In nature, lasting success is mostly about not dying — not about being the fastest. One India-focused fund manager built a remarkable record by applying that single idea to the stock market. His lessons are simple, and they are about the quality of a business, never about guessing its price.

A lesson from the jungle

In the wild, the animal that survives the longest is rarely the strongest or the fastest. It is usually the one that makes the fewest fatal mistakes — the deer that never wanders too far from cover, the one that does not take silly risks. Over thousands of years, nature does not reward the boldest gambler. It rewards the careful survivor.

Pulak Prasad, an India-focused investor, took this idea from biology and built an entire investment philosophy around it. Prasad runs Nalanda Capital, a fund that has invested in Indian companies since 2007 and earned an outstanding long-term record. In 2023 he wrote a book called What I Learned About Investing from Darwin, where he explains how Charles Darwin’s ideas about survival and evolution shaped the way he picks and holds shares. His message can be boiled down to three simple rules, and all three are about owning high-quality businesses — not about timing prices.

Why borrow ideas from biology at all? Because nature is the ultimate long-term test. Over millions of years it has quietly worked out what survives and what does not, and the answer is almost never “the reckless gambler”. Prasad’s simple bet is that the same forces that reward careful survival in nature also reward it in the stock market — where most investors are far too busy chasing excitement to notice. And he is worth listening to because he has lived his philosophy: Nalanda has compounded money in Indian shares for well over a decade by owning a small number of high-quality companies and barely touching them. The ideas are not complicated, and that is the point. You do not need to be a genius to invest well; you need to avoid being a fool, own good businesses, and be patient.

Rule 1: Avoid big mistakes — be a great “rejector”

Prasad’s first and most important rule is simple: do not lose a lot of money. He writes that a great investor is, above all, a great rejector — someone who says “no” to the vast majority of companies. Most of his work is not finding things to buy; it is throwing out almost everything. Over a long life of investing, he argues, you do well not by hitting more winners, but by avoiding the few disasters that can wipe you out.

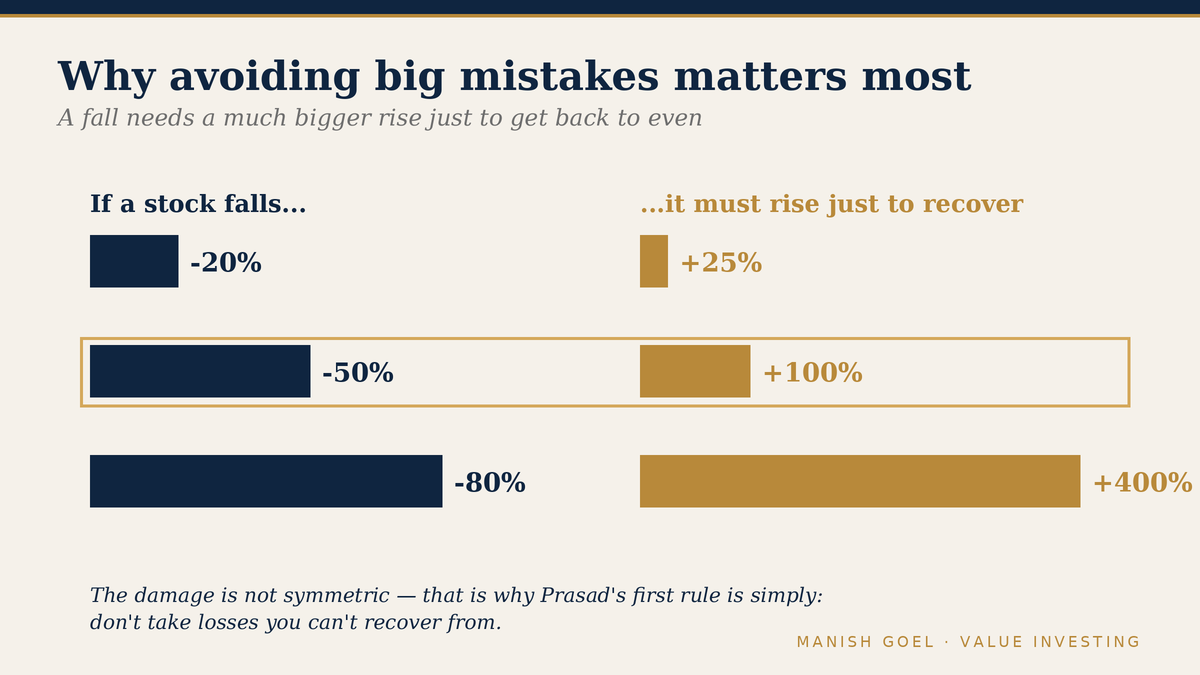

The maths shows why this matters so much. If a stock falls by 50%, it does not need a 50% rise to recover — it needs a 100% rise just to get you back to where you started. A single big loss can undo years of good, steady gains. So before he ever gets excited about how good a business could be, Prasad first asks: what could go badly wrong here, and could it seriously hurt me? If the honest answer is that a permanent, serious loss is possible, he simply walks away — no matter how exciting the story sounds. Think of it like crossing a busy Indian road: getting across quickly matters far less than not getting hit. Avoiding the accident is the whole game.

What does a “big mistake” usually look like? Rarely a small price wobble; it is something that can cause permanent damage. A company carrying far too much debt, so that one bad year can sink it. A promoter (the controlling owner) who is dishonest or treats the company as a personal piggy bank. A business that a single new technology or rule change could wipe out. Or, on your own side, putting too large a part of your savings into one risky bet. Spotting and refusing these is most of the job. As Prasad sees it, the first task is simply to make sure you are still standing to invest another day.

Rule 2: Own only high-quality businesses

Prasad’s second rule is to buy only excellent businesses and to become, in his words, a “permanent owner” of them. But how do you spot an excellent business simply, without drowning in numbers? Here he uses a wonderful story from biology.

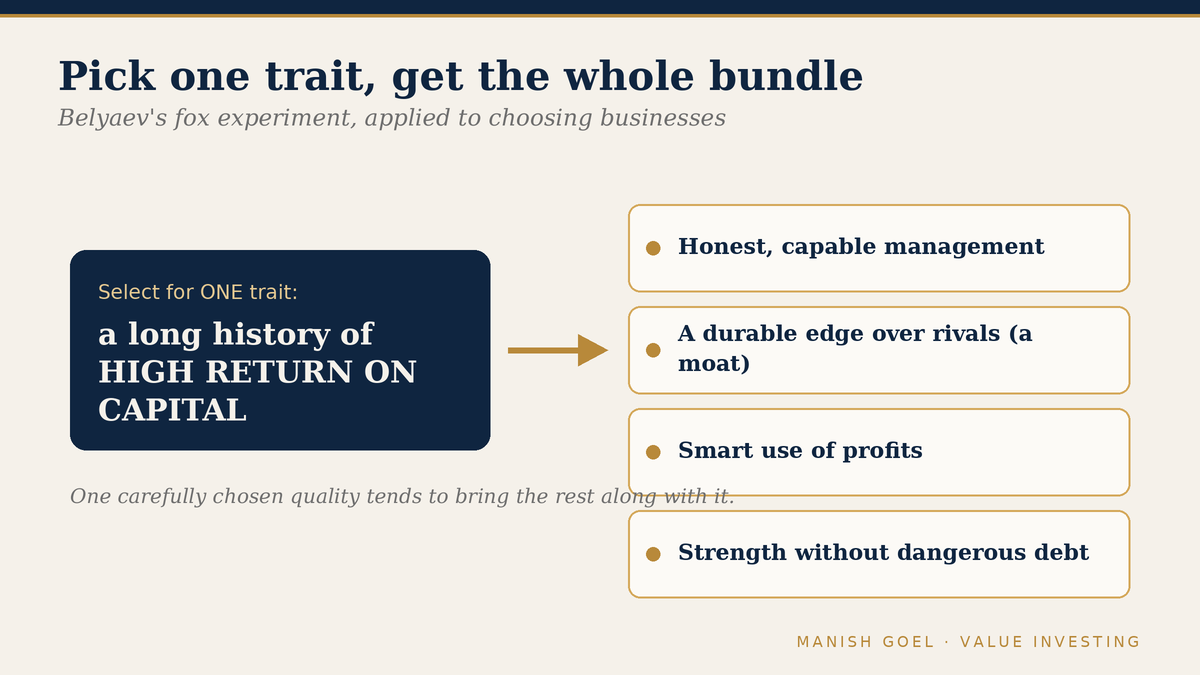

In Russia, a scientist named Dmitry Belyaev ran a famous experiment with wild silver foxes. He selected them for just one trait — friendliness towards humans — and bred only the calmest ones, generation after generation. Something surprising happened. By selecting for that single trait, he ended up with foxes that were not only tame but also developed floppy ears, curly tails and softer, dog-like looks. Choosing one good quality quietly brought a whole bundle of other good qualities along with it.

Prasad applies the same trick to companies. He focuses on a single, powerful trait: a long history of high return on capital (in simple terms, a business that has earned a lot of profit for years on the money put into it). His insight is that when you find a company with a genuinely high historic return on capital — sustained over many years — you usually get the whole bundle of quality for free: honest and capable management, a strong and durable edge over rivals, sensible use of profits, and the strength to take business risks without taking on dangerous debt. One good trait, chosen carefully, reveals all the others. (A note worth remembering: he relies on a long track record, not on a single good year or a rosy forecast.)

Why lean so heavily on the past record rather than a forecast? Because a forecast is just a hopeful guess about a future nobody can see, while a long history of high returns on capital is hard evidence that a business actually works. Think of choosing a player for an important cricket match: you would trust someone who has scored consistently for ten seasons over a newcomer with a great-sounding story. A company that has earned strong returns on its money for a decade or more — through good years and bad — has already proved it owns something special. Evidence beats imagination.

Rule 3: Don’t be lazy — be very lazy

The third rule sounds like a joke, but Prasad means it seriously: once you own a truly great business, do almost nothing. Sit still. Nalanda buys rarely and sells even more rarely; it aims to hold its companies more or less forever. Most investors do the opposite — they fiddle constantly, booking small profits, jumping in and out, reacting to every headline. All that activity usually does is generate costs and taxes while interrupting the magic of compounding (your returns earning further returns, year after year).

Think of planting a mango tree. If you dig it up every few weeks to check the roots, it will never grow. A great business is the same: its real rewards come from being left alone for ten or twenty years so it can grow and compound quietly. Darwin’s nature works over very long stretches of time, and so, Prasad argues, does serious wealth creation. The hardest part is not buying or selling — it is having the patience to do nothing while a good business does its work.

Over-activity is expensive in ways that are easy to miss. Every trade carries brokerage and taxes, and each time you sell a winner you hand a slice to tax and give up the years of compounding it still had ahead of it. Worse, constant buying and selling gives you many more chances to make a bad decision. Studies of ordinary investors around the world keep finding the same thing: those who trade the most tend to earn the least. Stillness here is not laziness — it is a deliberate strategy that lets a great business reward you fully.

How you can use these rules

1. Ask “what can go badly wrong?” first. Before you fall in love with a company’s growth story, look for the things that could cause a permanent loss — heavy debt, a dishonest promoter, a business that could be wiped out by one change. If a serious, lasting loss is realistically possible, reject it. Be a proud rejector; saying “no” often is a strength, not a weakness.

2. Use a long quality track record as your filter. Instead of chasing tips, look for businesses that have earned high returns on their capital for many years in a row, run by honest, capable people. Like the fox experiment, this one filter tends to surface companies that are strong in many other ways too. Demand history, not promises.

3. Once you own quality, leave it alone. If you have done the hard work and own a genuinely great business, your main job becomes patience. Resist the urge to keep trading. Let time and compounding do the heavy lifting, and check your roots far less often than you feel like doing.

Notice what is missing from all three rules: there is nothing here about predicting prices, calling the market cheap or expensive, or timing your entry to the rupee. Prasad’s whole approach is about the quality and survival of the business you own. Get those right, be patient, and the rest tends to follow.

A word of honesty: these rules are simple, but they are not easy. Rejecting most ideas can feel like missing out. Owning a wonderful business through a year when its share price falls — and still doing nothing — takes real nerve. And even great companies have rough patches. The point is not that this approach removes all discomfort; it is that, like careful survival in nature, it keeps you in the game long enough for quality and patience to do their work. That, in the end, is Prasad’s quiet challenge to every Indian investor: stop trying to be clever, and start trying to be wise — reject the dangerous, own the excellent, and then have the patience to leave it alone for years.

Key takeaways

- Avoid big mistakes first. A great investor is a great rejector. One large, permanent loss can undo years of gains — a 50% fall needs a 100% rise just to recover.

- Own only high-quality businesses. Like Belyaev’s foxes, picking one strong trait — a long history of high return on capital — tends to bring the whole bundle of quality (good management, a durable edge, sensible capital use).

- Be very lazy. Once you own a great business, do almost nothing. Constant trading kills compounding; patience protects it.

- It’s about quality, not price-guessing. Prasad’s rules say nothing about timing the market — they are about owning survivors and letting them compound.

- Darwin’s lesson: in markets as in nature, the long-term winners are the careful survivors, not the bold gamblers.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.