Value Investing — Educational Series

Think back to your school days. Every year, the class chose a monitor. The winner was usually the most popular child — the one with the best jokes, the new cricket bat, the biggest group of friends. And every year, a few months later, the board exam arrived. The exam did not care who was popular. It quietly weighed what each student had actually learnt.

The stock market runs both of these systems at the same time, on the same shares. Every single day, it holds an election. And slowly, year after year, it conducts an exam.

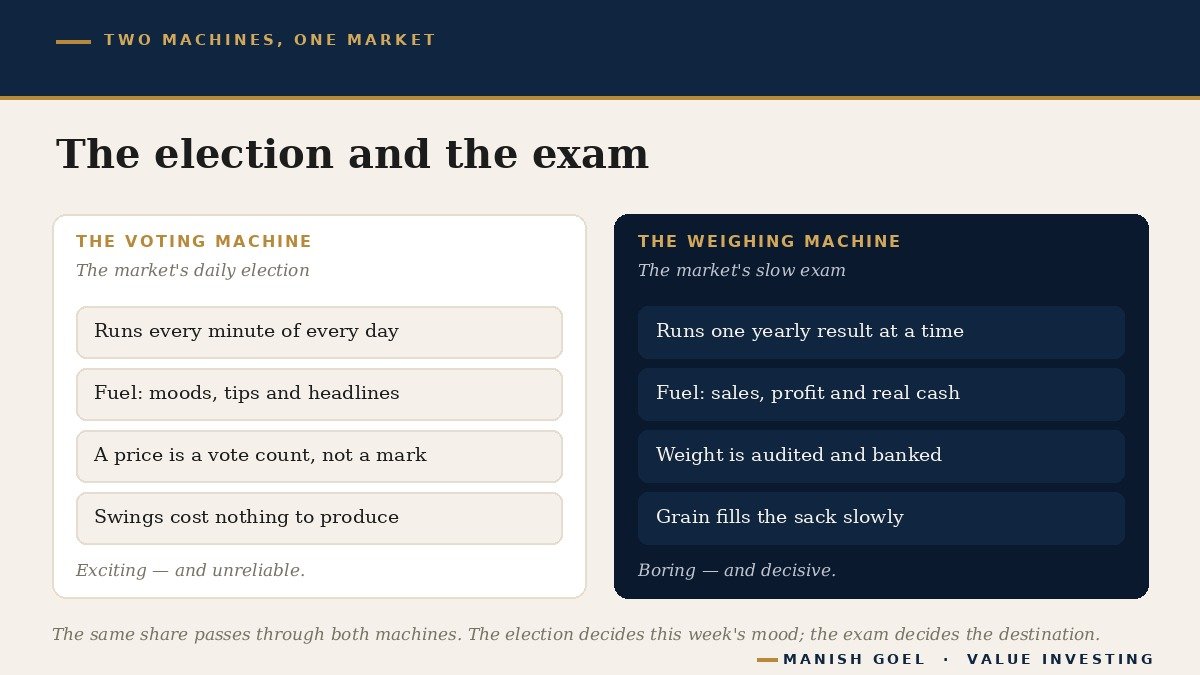

Benjamin Graham — the teacher of Warren Buffett, and widely called the father of value investing (the approach of buying pieces of good businesses and holding them patiently) — explained this double life of the market with a picture so simple that investors still repeat it every day, nearly a century later. He said the market is two machines in one: a voting machine and a weighing machine. Understand the difference between the two, and a large part of the market’s madness stops confusing you.

What Graham really said

In his 1934 book Security Analysis, written with David Dodd soon after the great American market crash of 1929, Graham warned readers not to treat the daily market price as a careful judgement of a company’s worth. The market, he wrote, is not a weighing machine, where the value of each share is recorded by an exact and impartial process. Instead, he said, the market is a voting machine — a counter where countless people register choices that are, in his exact words, “the product partly of reason and partly of emotion.”

In plain words: on any given day, a share’s price is a vote count, not an exam mark. It tells you how popular the share is this morning — how many people are excited, fearful, bored or hopeful about it. It does not tell you what the business behind the share actually earned.

Warren Buffett, who studied under Graham and later worked for him, remembered the full teaching in a shorter form. In his 1987 letter to shareholders, he quoted his teacher like this: “In the short run, the market is a voting machine but in the long run it is a weighing machine.” The short run means days, weeks, months, even a year or two. The long run means five years, ten years, a working lifetime.

It helps to remember when this lesson was written. Graham had just lived through the crash of 1929, in which share prices in America fell for nearly three years and wiped out families who had believed that a rising price was itself the proof of a good company. He watched people treat every day’s quotation as a verdict — celebrating when the number rose, despairing when it fell — without ever asking what the businesses behind those numbers were earning. His two machines were built to cure exactly that confusion, and the cure has not aged at all.

Every Indian who has visited a sabzi mandi (vegetable market) knows both machines already. A vendor’s loud shouting can gather a crowd around his stall today. But when your bag is placed on the tarazu — the weighing scale — the shouting stops mattering. The pan reads only what is actually in it. Votes are the shouting. Weight is what lands in the pan. Graham’s lesson is that share prices behave like the shouting in the short run, and like the tarazu in the long run.

Why the scale wins in the end

Why should a beginner trust the weighing machine more than the voting machine? The logic is plain once you see what each machine runs on.

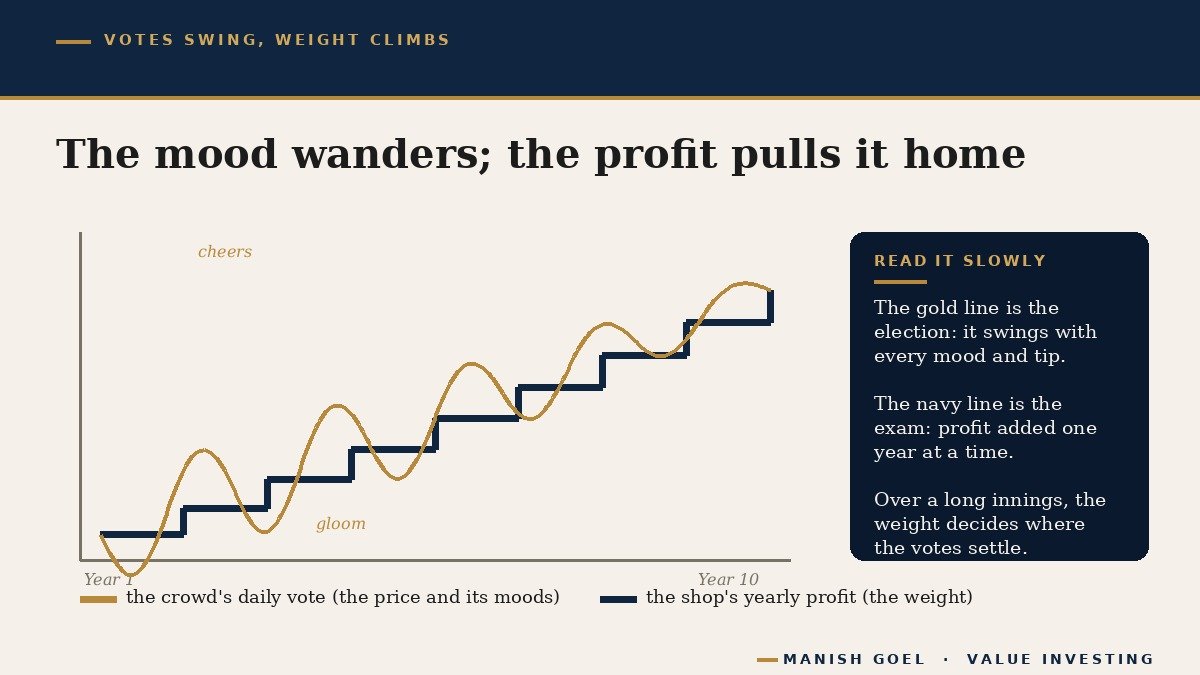

Votes are free, and votes are fickle. A forwarded tip on WhatsApp, a loud headline, a neighbour’s boast at a wedding — any of these can add or subtract thousands of votes today. But notice: none of them adds a single rupee to what the business actually earns. The shop’s daily sales do not change because the whole bazaar is shouting about its name.

Weight is different. Weight is profit that truly arrives — money left in the company’s bank after paying staff, suppliers, tax and interest on loans. Weight collects the way grain fills a sack: slowly, one season at a time. A company that earns more this year than last year, and more again the year after, is quietly adding weight to its pan whether anyone is watching or not.

And here is the simple mechanism that finally connects the two machines. As a business earns more, it can do more for its owners. It can pay a growing dividend (the part of profit a company hands to its shareholders in cash). It can repay its loans. It can open new plants and shops and earn even more. Sooner or later, even the most distracted voter notices a shop whose profits have doubled, and then doubled again. The votes eventually move towards the weight — not because voters suddenly become wise, but because real weight becomes impossible to ignore.

Buffett described exactly this habit in that same 1987 letter: “Following Ben’s teachings, Charlie and I let our marketable equities tell us by their operating results — not by their daily, or even yearly, price quotations — whether our investments are successful. The market may ignore business success for a while, but eventually will confirm it.” Read that middle line twice. The market may ignore business success for a while. That “while” is where most investors lose patience — and where the calm ones quietly win.

Cricket lovers can say the same thing in one line: a single over of sixes wins the crowd’s cheers, but a ten-year batting average is weighed, not cheered.

There is one more reason to distrust the vote count on its own: votes can sometimes be rented. In small, thinly traded shares, a handful of determined players can push a price up sharply for a while, simply by trading among themselves and drawing a crowd. The jump looks like public excitement; much of it is manufactured shouting. Our market’s history has seen such episodes again and again, and the regulator keeps warning ordinary investors about them. The weighing machine cannot be rented in this way. Sales must be billed, profits must be audited (checked by an independent accountant), cash must reach the bank, dividends must actually be paid. It is easy to print noise; it is very hard to fake grain in a sack, year after year.

One honest caution before we go further. The weighing machine rewards only real weight. A weak business that nobody votes for is not a hidden treasure; it is simply a weak business. Graham’s lesson is not “unpopular shares are good.” The lesson is about where to look: at the khata (the account book), not at the crowd.

Two true stories from our own market

Our own market has run both machines in full public view, and two famous elections show the whole lesson.

First, an election that failed. In February 1993, a software company from Bengaluru offered its shares to the public for the first time — an IPO (initial public offering, a company’s first sale of its shares to ordinary investors) — at 95 rupees per share. The company was called Infosys. So few people voted for it that the issue was undersubscribed — fewer applications arrived than there were shares on offer — and the bankers managing the issue had to step in, with the American firm Morgan Stanley picking up a large block of shares to complete the sale. When the share listed a few months later, it opened around 145 rupees. The crowd had shrugged. But year after year, the weight kept arriving: more clients, more engineers, more profit, decade after decade. A hundred shares bought for 9,500 rupees in that ignored issue, held patiently through every bonus issue (free extra shares given to existing owners) and share split (one share divided into several smaller ones), grew into a holding worth crores of rupees over the following three decades. The election of 1993 said “not interested.” The weighing machine said otherwise — one annual report at a time.

Now, an election that roared. In January 2008, at the very top of a booming market, a new power company offered its shares to the public at 450 rupees each. It had grand plans, but at that time, hardly any operating power plants earning money. The company was Reliance Power. The election was thunderous: about five million applications poured in, and the issue was oversubscribed roughly 73 times — for every share on offer, applications arrived for about seventy-three. On 11 February 2008, the share listed, rose briefly, and then fell the same morning, closing about a sixth below its issue price on its very first day. The years that followed conducted the exam. The profits the crowd had imagined did not arrive in time, and the price stayed far below 450 rupees for years upon years. Five million votes could not put weight into the pan.

Same market. Same rules. Opposite elections — and in both cases, it was the scale, not the shouting, that wrote the final result. Please read these as history, not as any comment, good or bad, on any share today. That is exactly how we tell every story in this series: to learn from the machine, never to point at a name.

How you can use it

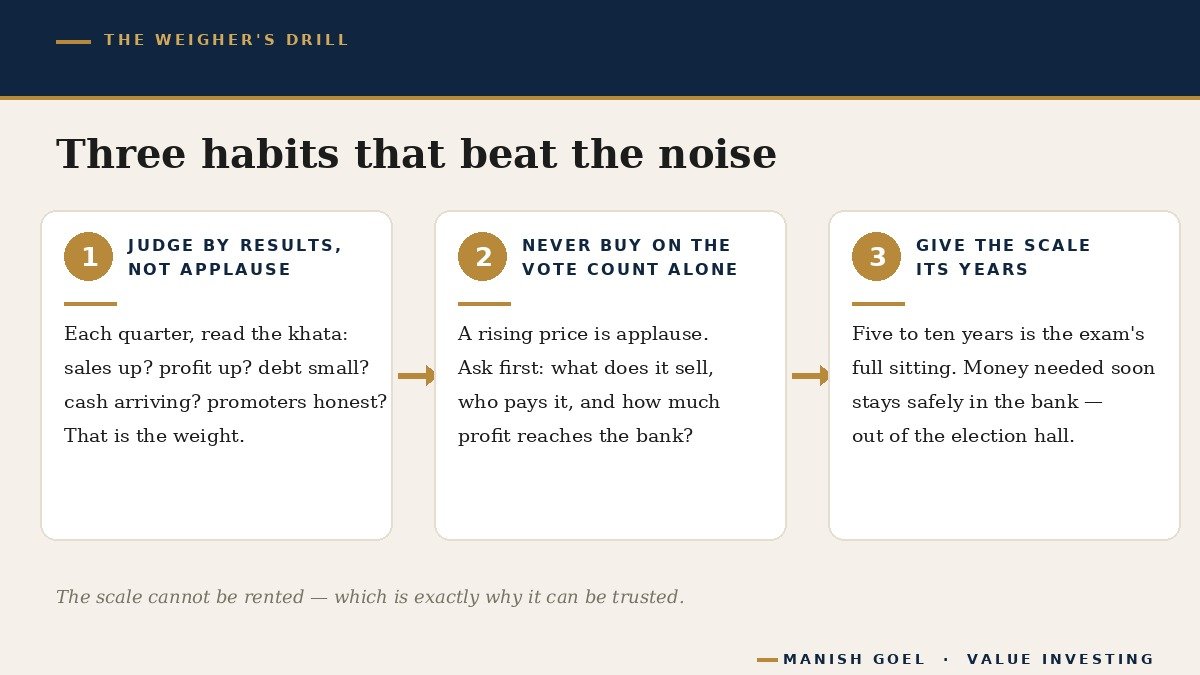

You do not need high mathematics to put Graham’s two machines to work. You need three habits.

One: judge your shares by results, not by applause. Once every three months, each listed company publishes its results; once a year, a full annual report. Read the few lines that carry weight: are sales growing, is profit growing, is the debt small, is cash truly arriving in the bank, and do the promoters (the founding family or group that controls and runs the company) deal with shareholders honestly? That is the weight. If the weight is healthy and only the vote count has fallen, you have learnt something calming: it is the election that changed, not your business.

Two: never buy only because the price is rising, or because everyone around you is applying. A rising price is a vote count, and votes tell you about the crowd’s mood, not the shop’s earnings. Before joining any queue, ask the exam question instead: what does this business sell, who pays it, and how much profit reaches its bank? If you cannot answer in two plain sentences, the queue can move on without you. Nothing is lost by missing an election; a great deal is lost by failing an exam you never checked.

Three: give the scale time. Weighing is slow by design. Five years is a fair sitting for the exam; ten is better. A fixed deposit pays on a fixed date, but a business pays on the scale’s schedule, not the calendar’s. Money you will need next year — for a fee, a wedding, a house payment — does not belong in the election hall at all. Keep it safe in the bank, and send only long-term savings to sit for the long exam.

Key takeaways

- Every day the market votes; over the years it weighs. Prices follow popularity first, and profits in the end.

- A rising price is applause, not proof. Ask what the business earns before you join any queue.

- Weight means growing sales, growing profit, low debt, cash that actually arrives, and honest promoters — nothing more mysterious than that.

- The scale is slow. Give a good business five to ten years for the weighing, and keep short-term money out of the election hall.

- When a strong company’s price falls while its results stay strong, it is usually the votes that changed, not the business. Check the weight before you change your mind.

Graham left us many gifts, but this picture may be the kindest one for a beginner: two machines, one market. The voting machine measures noise. The weighing machine measures nourishment. The crowd will always run to watch the vote count — it changes every minute, and it is exciting. Your money, though, is fed by the tarazu. Watch the pan, not the shouting, and let the years do the weighing.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.