Value Investing — Educational Series

Think of two family weddings, a few years apart. At the first one, you mention that you have started investing in shares (small pieces of ownership in a company). Your uncle quickly changes the subject to gold. Your cousin says the share market is a casino. Within a minute, you are standing alone near the paneer counter.

At the second wedding, you do not even have to raise the topic. The photographer has a tip (the name of a share passed around like a secret, with no homework behind it). The caterer is checking prices between servings. Three uncles surround you with the names of companies you have never heard of. Nobody asks what these companies actually do. Everybody is sure.

Same family. Same city. Often the very same people. What changed in between? Not the quality of India’s businesses — real businesses change slowly. What changed is the market’s mood (how hopeful or fearful investors feel as a group). And one of the greatest investors of the last century built a famous little tool for reading that mood. He built it by standing quietly at parties, listening.

Peter Lynch ran America’s Fidelity Magellan Fund (a giant mutual fund — a pool where a professional invests money collected from lakhs of ordinary savers) from 1977 to 1990, and earned his investors roughly 29 per cent a year — one of the finest long records in history. In his 1989 book One Up on Wall Street, he described what he playfully called the cocktail party theory. It is simple, funny, and full of quiet wisdom. Today’s lesson walks through it in plain words — and shows what an ordinary Indian investor should, and should not, do with it.

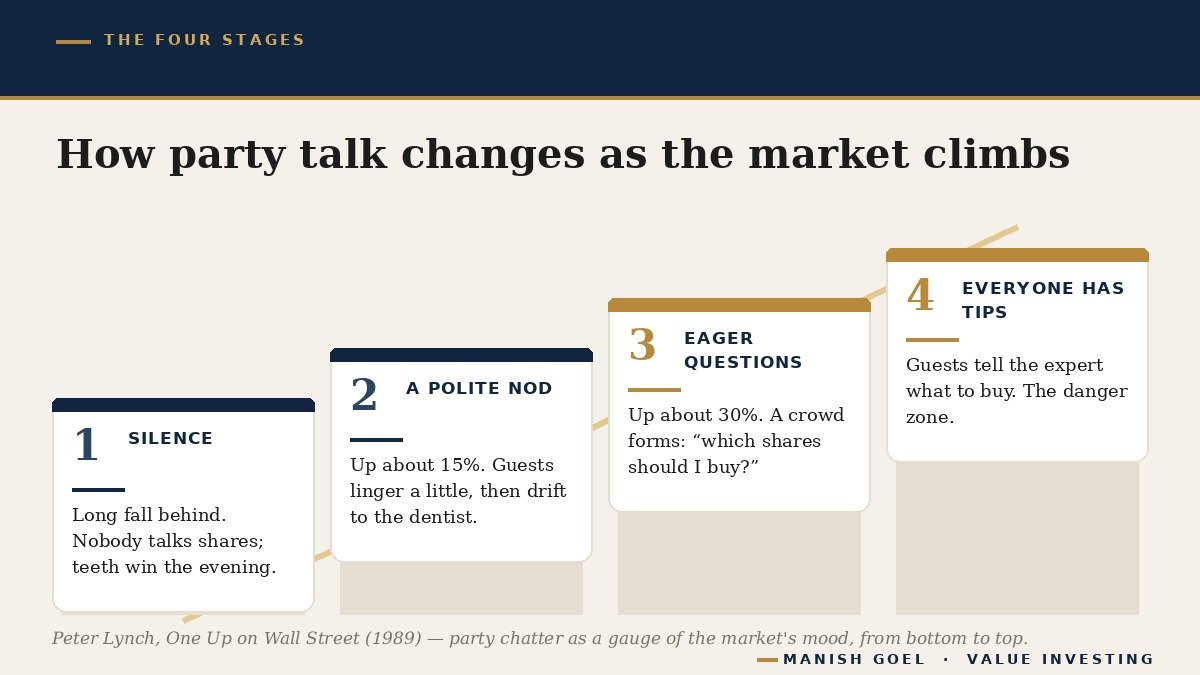

The four stages Lynch heard at parties

Lynch wrote that for years, when the market was about to do something important, he could sense it at social gatherings. He would stand near the snacks and simply watch how the ten people nearest to him reacted when they learned that he managed money for a living.

Stage one: silence. The market has been falling for a while, and nobody expects it to rise again. When Lynch told people what he did, they would nod politely, mumble that shares are risky, and drift away to chat with the dentist standing nearby — about tooth plaque. Lynch’s joke was sharp: when people at a party would rather discuss teeth than shares, the market’s mood has hit rock bottom. And that, he noticed, is usually when the market is quietly getting ready to climb.

Stage two: a polite nod. The market has risen about 15 per cent from its low. Now people linger with Lynch a little longer. They still say the market looks risky, and they still end up with the dentist — but the fear has softened.

Stage three: eager questions. The market is up around 30 per cent. Suddenly the dentist stands alone. A circle of excited guests surrounds Lynch all evening, asking one question again and again: which shares should I buy? Even the dentist asks.

Stage four: everyone has tips. This stage is the funniest, and the most dangerous. The guests crowd around Lynch once more — but this time nobody is asking. They are telling. The photographer, the caterer and, yes, the dentist all have three tips each, and the tips have been going up. When the neighbours start telling the expert what to buy, Lynch wrote, and when he catches himself wishing he had taken their advice, the market has very likely climbed near a top.

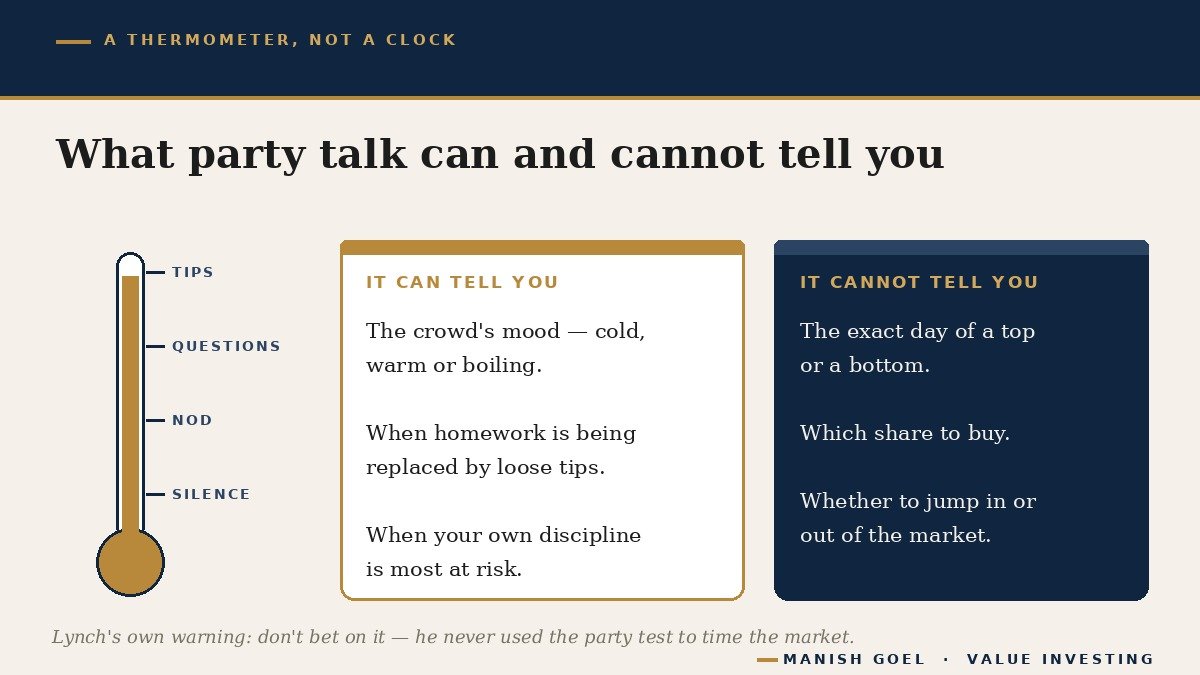

What it really means: a thermometer, not a clock

Strip away the humour, and the theory says something simple. The amount of share-talk around you measures the market’s temperature. When the talk is freezing cold — silence, embarrassment, warnings — most people who wanted to sell have already sold, or have sworn off shares completely. When the talk is boiling hot — tips flying at wedding buffets, in office lifts, in family WhatsApp groups — most people who could buy have already bought. An FD (fixed deposit) pays the same interest whether the neighbourhood is excited or bored. Shares are different in the short run: their prices swing with the crowd’s feelings, even when the business underneath has not changed at all.

Think of a cricket World Cup. In the group stage, only true fans discuss the team. By the final, the whole country has become a selector — people who cannot name the twelfth man are angrily explaining the batting order. All that noise tells you nothing new about the team. But it tells you everything about the excitement around it. Party talk about shares works the same way. It measures the crowd’s excitement, not the strength of the businesses.

That is why the honest way to use the theory is as a thermometer, not a clock. A thermometer tells you the fever is high; it does not tell you the hour it will break. Lynch himself gave a clear warning in the very same book: do not bet on this. He wrote that he does not believe in predicting markets — he believes in buying great companies. The party test never told him when to jump in or out of the market. It simply told him what the crowd was feeling, so that he could make sure he was not blindly feeling it too.

Why it works: the logic of the last buyer

Why should the chatter at a wedding carry any information about the share market at all? The logic is plain, and it is worth keeping for life. In the short run, share prices rise when new buyers keep arriving with fresh money. Prices fall when sellers outnumber buyers. That is all there is to it.

Now walk through the stages again with that in mind. In stage one, everyone who panicked has already sold. The people still holding shares are the patient ones who refuse to sell at any mood. Selling pressure is nearly exhausted — which is why, at the bottom, even bad news stops pushing prices much lower. In stage four, it is the opposite. When the caterer, the photographer and all three uncles already own shares — and are busy recruiting new buyers at a wedding — ask the child’s question: who is left to buy? When almost everyone who wanted to join the party has joined, the fresh money dries up. Like in musical chairs, the music is loudest exactly when the chairs are about to run out.

There is a second, deeper reason the boiling stage is dangerous. In a hot market, people stop doing homework. Shares get bought because a neighbour mentioned them — not because anyone checked what the company sells, whether it earns real profits, or how much debt (borrowed money that must be repaid whatever happens) sits on its books. Buying without homework is not investing; it is borrowing someone else’s conviction. And borrowed conviction runs away at the first fall. Warren Buffett compressed all of this into one famous line: be fearful when others are greedy, and greedy only when others are fearful.

Old stories, and a Dalal Street repeat

The oldest version of this lesson is nearly a hundred years old. The story goes that in 1929, Joseph Kennedy — a wealthy American businessman, and father of a future president — sat down to have his shoes polished. The shoeshine boy, while working, offered him tips on which shares to buy. Kennedy stood up with a cold feeling: if even the shoeshine boy is handing out tips, then everyone who could enter the market is already in. He quietly got out. Soon after came the great crash of 1929, the worst in market history. Historians admit the tale may be part legend — but it has survived a century because it is true to life.

India has its own versions. Old-timers remember the boom of 1992, when share-talk conquered every street corner and the Sensex (the index that tracks thirty of India’s largest companies — the market’s scoreboard) raced up to about 4,500 by April. Then a big market scandal came to light, the mood snapped, and by August the Sensex had fallen by more than 40 per cent. The party went silent almost overnight.

It happened again in 2008. In January of that year, after a five-year climb, the Sensex crossed 21,000 for the first time, and shares had become the favourite subject at every gathering. By October, as a global financial crisis unfolded, the index had fallen roughly 60 per cent. Here is the part worth remembering: the real businesses of India did not shrink by 60 per cent that year. Factories still ran, biscuits still sold, medicines still shipped. The mood shrank, and prices followed the mood.

And in our own time, the party has grown larger than ever. India had about four crore demat accounts (the electronic accounts in which shares are kept) in 2020. Today there are more than twenty-one crore. That is a wonderful thing for the country — many more families now own a piece of Indian business. But it also means the WhatsApp groups are louder, and Lynch’s four stages now play out on your phone screen instead of at the punch bowl. None of this is a prediction about where the market goes next. It is a reminder that the pattern is old, human, and always dressed in new clothes.

How you can use it

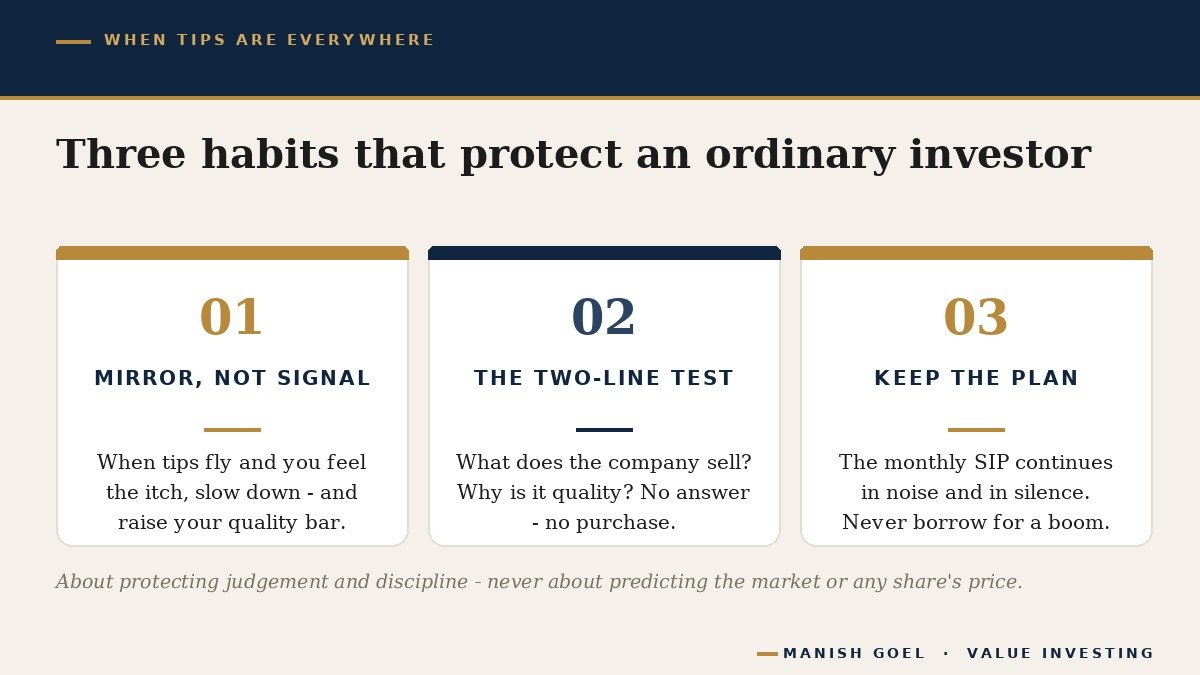

So what should an ordinary investor actually do with the cocktail party theory? Three simple habits cover it.

First, use it as a mirror, not as a signal. The theory is most useful when you point it at yourself. When tips are flying around you and you feel the itch to act quickly, treat that itch as a warning light on your own dashboard. Ask honestly: am I buying this because I understand the business, or because everyone around me is excited? The moment of maximum party noise is exactly the moment to slow down and raise your quality bar — look for businesses with steady profits, little debt, and honest, capable promoters (the main owners who run the company).

Second, apply the two-line test to every tip. Before acting on any name you hear, see if you can explain, in two plain lines, what the company sells and why it is a high-quality business. If you cannot, the tip is not an investment — it is a lottery ticket with a company’s name printed on it. This one habit quietly filters out most of the damage a hot market can do to a family’s savings.

Third, keep your simple plan running in noise and in silence. If you invest a fixed sum every month (a SIP), let it continue through the boring stage one, when nobody at the party wants to discuss shares — that quiet stretch is when patient investors slowly accumulate good businesses. Let it continue through stage four too, instead of borrowing money to “catch the wave”. Never borrow to invest in a boom, and never stop investing merely because the room has gone quiet. The party’s volume should change your alertness — never your discipline.

Notice what is missing from this list: jumping in and out of the market. Lynch, who invented the theory, did not use it for market timing (guessing tops and bottoms so as to trade in and out). He stayed invested through booms and crashes and let great businesses do the compounding (earning returns on your past returns — like a snowball growing as it rolls downhill). The party test exists to protect your judgement, not to replace it. And none of it is about guessing whether any share is cheap or expensive — it is about protecting the discipline with which you judge the quality of a business.

Key takeaways

- Peter Lynch’s cocktail party theory: the way people at a gathering react to shares moves through four stages — silence, a polite nod, eager questions, and finally everyone handing out tips.

- Party talk is a thermometer, not a clock. It measures the crowd’s excitement; it cannot tell you the day the market turns — and Lynch himself warned against using it to predict.

- The logic is the last buyer: when everyone already owns shares and is recruiting others, fresh money is running out; when nobody wants to talk, the sellers are mostly done.

- Hot markets make people buy on borrowed conviction. The louder the tips, the higher your quality bar should rise: steady profits, low debt, honest promoters, and a business you can explain in two lines.

- Let the party’s volume change your alertness, never your discipline: keep the monthly plan going in silence and in noise, never borrow to join a boom, and always judge the business, not the buzz.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.