Value Investing — Educational Series

Have you ever noticed how, on one busy market lane, the moment a single sweet shop starts doing well, three more sweet shops open within a month? Or how, in a boom year, one builder announces a shopping mall and suddenly every builder in the city wants a mall too? The people running these businesses are not foolish. Many are hard-working and clever. Yet again and again, good companies — and their capable bosses — make the same expensive mistakes at the same time, as if pulled by an invisible string.

Warren Buffett, the world’s most famous long-term investor, gave this invisible string a name. He called it the institutional imperative (the quiet pressure inside a company that pushes even smart managers into doing what everyone else is doing, whether or not it makes sense). Once you learn to see it, you start to understand why so many businesses waste money — and, more usefully for us, how to spot the rare, high-quality management that refuses to be pushed around by it. This is a lesson about judging the people running a business, not about whether any share is cheap or dear.

A strange thing you may have noticed

Think back to your school days. The class topper writes an answer. Slowly, other students start copying it — even the ones who suspect it might be wrong. Why? Because if everyone gets the same answer wrong, no single student stands out and gets scolded. But if you write a different answer and you are the one who is wrong, everyone remembers. Being wrong along with the crowd feels safe. Being wrong alone feels dangerous.

Grown-up businesses behave in exactly the same way. Picture a chaiwala (tea seller) whose little stall is doing beautifully. He has spare cash for the first time in his life. A voice inside says, “Don’t just sell tea — the shop next door added a photocopy machine, so add one too. And a mobile-recharge counter. And maybe a tiffin service.” Six months later he is running four half-baked businesses, his famous tea has become average because his attention is scattered, and his savings are gone. He did not fail because he was lazy. He failed because he could not sit still while holding spare cash and watching his neighbours expand.

Now scale that chaiwala up to a company worth thousands of crores (tens of billions of rupees), with a boardroom, consultants and a proud chairman. The same pull is at work — only now it is dressed up in fancy presentations. That pull is the institutional imperative, and it is one of the biggest destroyers of shareholder wealth that almost nobody talks about.

What Buffett really meant

In his famous 1989 letter to Berkshire Hathaway shareholders (Berkshire is the company Buffett built into one of the largest in the world), he wrote: “My most surprising discovery: the overwhelming importance in business of an unseen force that we might call ‘the institutional imperative.'” He admitted that business school never warned him about it. He had assumed that “decent, intelligent, and experienced managers would automatically make rational business decisions.” Then he learned the hard truth: “rationality frequently wilts when the institutional imperative comes into play.” In plain words — even good, honest, clever bosses often stop thinking clearly once this pressure takes over.

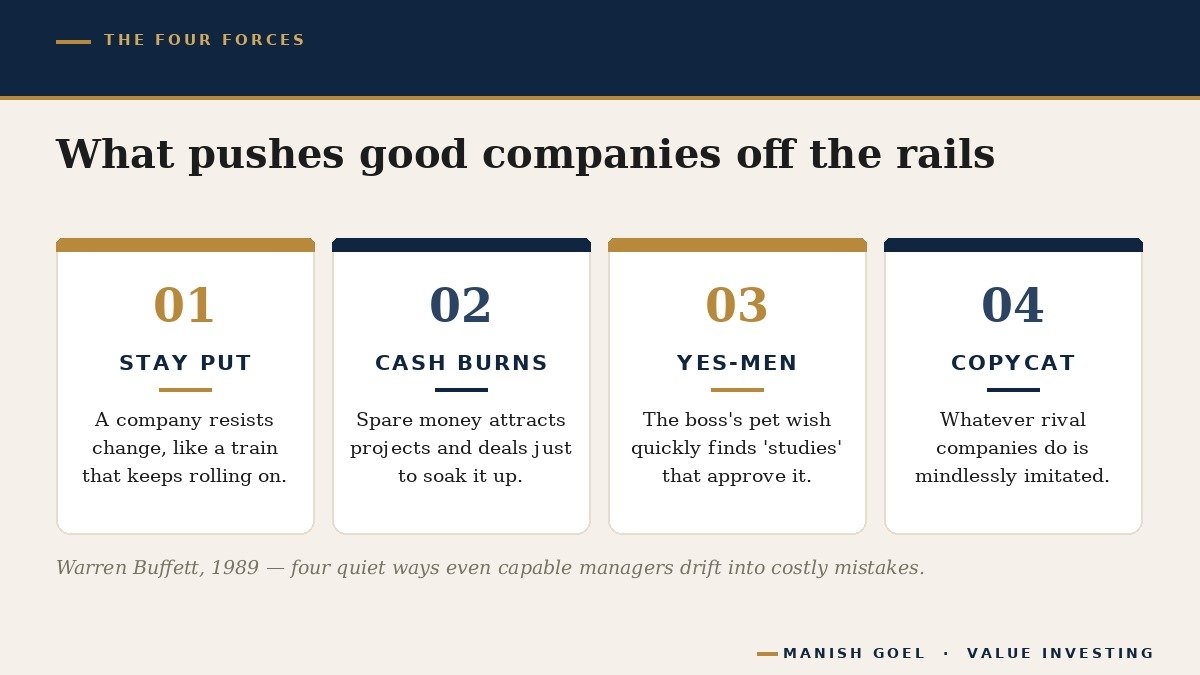

Buffett listed four forces that push companies off the rails. Let us translate each one into everyday language.

One: businesses resist change, like a train that keeps rolling. Buffett compared this to a law of physics — an object in motion stays in motion. If a company has always done things a certain way, it keeps going that way long after it should have stopped, simply because turning is hard and nobody wants to be the one to pull the brake.

Two: spare money finds a way to get spent. Buffett borrowed a famous idea called Parkinson’s Law — “work expands to fill the time available.” Money behaves the same way, he said: “corporate projects or acquisitions will materialize to soak up available funds.” An acquisition is simply one company buying another. When a firm is sitting on a big pile of cash, projects and takeover deals magically appear to use it up — not because the company needs them, but because the cash is just lying there, tempting everyone.

Three: the boss’s pet wish always finds “proof.” Buffett put it sharply: “Any business craving of the leader, however foolish, will be quickly supported by detailed rate-of-return and strategic studies prepared by his troops.” In other words, once a powerful chairman decides he wants to build that factory or buy that company, his own team will rush to prepare thick reports full of charts that conveniently prove the boss is right. Nobody wants to be the person who tells the king his idea is bad.

Four: companies copy their rivals without thinking. “The behavior of peer companies,” Buffett wrote, “whether they are expanding, acquiring, setting executive compensation or whatever, will be mindlessly imitated.” If a competitor launches a new business line or hikes the boss’s pay, the others follow — like our sweet shops on the market lane. Buffett joked that managers would rather fail in a crowd than risk standing out: as a group, lemmings may have a rotten image, he said, but no single lemming ever gets the blame.

Notice something kind in Buffett’s explanation. He said these mistakes come from “institutional dynamics, not venality or stupidity” — meaning the managers are usually neither crooked nor dumb. They are ordinary people caught in a strong current. That is exactly why the imperative is so dangerous: you cannot spot it by looking for bad people. You have to look for bad behaviour, even in good people.

Why this pull is so strong

If the institutional imperative leads to such costly mistakes, why does it win so often? Because the pressures behind it are deeply human.

The first reason is career safety. A manager who quietly does nothing while rivals expand looks lazy, even if doing nothing was the wise choice. A manager who makes a big, bold acquisition looks like a hero on the day it is announced — and if it later fails, well, “everyone was doing deals back then.” Looking active is rewarded; sitting still is punished, at least in the short run.

The second reason is ego. Running a bigger empire feels grander than running a smaller, better one. A chairman who controls fifteen businesses can feel more important than one who controls two — even if the two make more money and the fifteen are a headache. Size flatters the ego in a way that quiet quality never does.

The third reason is the comfort of company. When everyone in your industry is doing the same thing, it feels normal and responsible. Going against the crowd feels reckless and lonely. Remember the wedding-season pressure to spend as much as the neighbours spent, simply because “log kya kahenge” (what will people say)? Boardrooms feel that same pressure, only with far bigger sums of money.

A real example or two

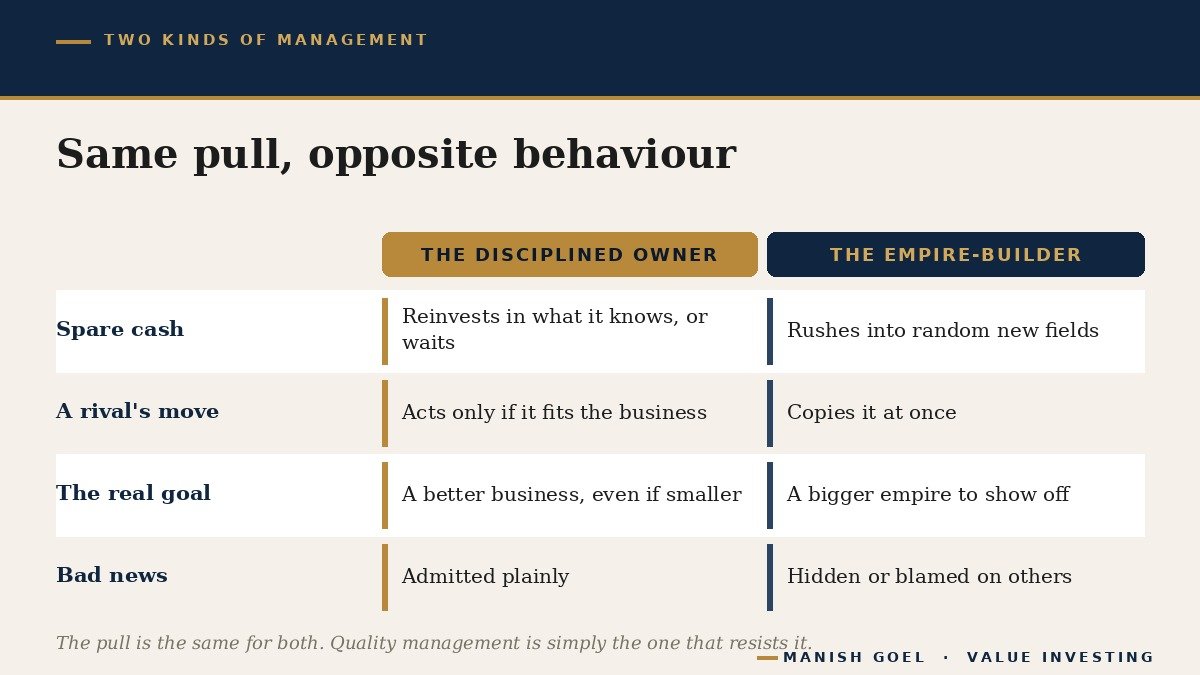

The good news is that a few managers do resist — and they are exactly the kind of people a quality-focused investor wants to find. A wonderful Indian example is Eicher Motors, the company that owns the old motorcycle brand Royal Enfield. In the early 2000s the group was a scattered mess: it was spread across roughly fifteen different businesses — tractors, trucks, motorcycles, engines, components, even maps — and most were only average. A young leader named Siddhartha Lal took charge in his early thirties and did something most bosses find almost impossible. Instead of adding more, he subtracted. Around 2005 he sold or shut about thirteen of those fifteen businesses, keeping only the two where he believed the company could become a true leader: motorcycles and trucks.

That decision went completely against the institutional imperative. It meant a smaller empire, fewer things to boast about at parties, and the discomfort of walking away from businesses the family had built over decades. Lal later summed up the whole lesson in one honest sentence: “The most difficult thing in business and in life is the ability to say, ‘no, this doesn’t work’.” By focusing fiercely instead of spreading thin, that once-ordinary motorcycle unit went on to become one of India’s most admired businesses. (This is simply a piece of history to learn from — it is not advice about the company or anything to do with its share price.)

Now the other side. Buffett is honest that even he was not immune. He admitted he made “some expensive mistakes because I ignored the power of the imperative” before he learned to fight it. And you can watch the imperative at work in every boom. A company suddenly flush with cash announces it is entering a hot, unrelated field — because a rival just did. A profitable firm pays a huge price for a “trophy” acquisition that its own consultants happily bless. A whole industry copies one competitor’s discount war until nobody makes any money. No names are needed; once you know the pattern, you will see it in the newspaper almost every week.

Buffett’s own response was telling. He wrote that he and his partner Charlie Munger try to “concentrate our investments in companies that appear alert to the problem” — that is, they deliberately look for management teams that resist the herd. That single habit is something an ordinary investor can copy.

How you can use this as an investor

You do not need a finance degree to put this lesson to work. You just need to watch how a company’s management behaves, especially when it has spare cash. Here are three simple habits.

First, watch what they do with extra money. When a company earns more cash than it needs, does the management pour it back into the business it truly understands, return some to shareholders, and stay patient — or does it rush into random, unrelated fields just because the money is there? A boss who calmly says, “we will wait for the right opportunity,” is often showing you the discipline Buffett prized. How a management uses spare cash is called capital allocation (deciding where the company’s money goes), and it is one of the clearest windows into management quality.

Second, prefer bosses who can say “no.” Read a few years of a company’s annual report (the yearly booklet every listed company sends its owners) or listen to what the promoters say. A promoter is the founding family or main owner who controls most Indian companies. Do they stick to what they do best, admit mistakes plainly, and avoid chasing every shiny new trend? Or do they announce a grand new plan every year and quietly bury the old ones? Focus and honesty are quality signals; restless empire-building is a warning sign.

Third, be extra careful when you hear “everyone is doing it.” When a company’s main reason for a big move is that rivals are doing the same, treat it as a yellow light, not a green one. Mindless imitation is the fourth force on Buffett’s list for a reason. The best managements act because a move makes sense for their business, not because the neighbour did it first.

None of this is about guessing whether a share is cheap or expensive. It is about recognising real quality in the people steering the ship. A wonderful business run by a disciplined, imperative-resisting management can keep compounding (growing on top of its own past growth, like interest earning interest, or a snowball rolling downhill) for many years. A business run by an empire-builder can waste even the finest opportunities.

Key takeaways

- The institutional imperative is the quiet pressure that pushes even smart, honest managers to copy the crowd and waste money.

- Buffett named four forces: companies resist change, spare cash gets spent, the boss’s pet wish always finds “proof,” and rivals are copied without thinking.

- These mistakes usually come from human pressure — career safety, ego and the comfort of the crowd — not from bad or stupid people.

- High-quality management resists the pull: it focuses, says “no” to shiny distractions, and spends spare cash wisely — as Eicher’s leader did by choosing focus over a scattered empire.

- As an investor, judge how management behaves with spare money and peer pressure. This is about spotting quality in people, never about a share’s price.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.