Value Investing — Educational Series

In almost every Indian town there is a family like this one. Upstairs, in a steel cupboard, sits a small pouch of gold — bangles from a wedding, a chain bought when the harvest was good, a few coins added over thirty years. Downstairs is the family’s kirana shop. For those same thirty years, the gold slept quietly in the dark. The shop, meanwhile, opened every morning at seven. It fed the family, paid school fees, survived two bad droughts, and slowly became two shops. Both the pouch and the shop were called “wealth”. But only one of them ever did any work.

Warren Buffett — widely regarded as the most successful investor of our age, and the man who built Berkshire Hathaway, a giant American company that owns dozens of businesses — once turned this everyday observation into one of the most famous thought experiments in the history of investing. He asked, in effect: if you could own all the gold in the world, or a collection of working farms and businesses worth the same amount, which would you choose? His answer, and the simple reasoning behind it, is today’s lesson.

A cube of gold you could touch but never grow

Every year Buffett writes a letter to the shareholders (the part-owners) of his company. These letters are read all over the world because he explains big ideas in small words. In his letter for the year 2011, he did some simple arithmetic on gold.

At that time, all the gold ever mined in human history came to about 170,000 tonnes. Buffett asked readers to imagine melting every last gram of it into a single solid cube. That cube would measure about 68 feet on each side — roughly as wide as a cricket pitch is long, and about as tall as a six-storey building. Every wedding bangle in India, every coin in every locker, every bar in every central bank vault on earth — all of it would fit into that one cube standing quietly in a field.

At the gold price of that day, the cube was worth about 9.6 trillion dollars — a number so large it was more than five times the size of India’s entire economy in that year. Buffett called this cube “pile A”. Then he built an imaginary “pile B” costing exactly the same amount. With 9.6 trillion dollars, he wrote, you could buy all the farmland in the United States — 400 million acres producing about 200 billion dollars of crops every single year — plus sixteen companies the size of ExxonMobil, then the most profitable company in the world, each one earning more than 40 billion dollars a year. And after buying all of that, you would still have about 1 trillion dollars left in your pocket as, in his words, walking-around money.

Then came the famous question: “Can you imagine an investor with $9.6 trillion selecting pile A over pile B?”

To make the point unforgettable, he looked a hundred years ahead. A century from now, he wrote, the farmland will have produced staggering amounts of corn, wheat and cotton, and will still be producing more, whatever money looks like by then. The sixteen Exxons will have paid out trillions of dollars in dividends (a dividend is the share of profit a company hands to its owners in cash). And the gold? In his exact words: “The 170,000 tons of gold will be unchanged in size and still incapable of producing anything. You can fondle the cube, but it will not respond.”

Read that line twice. You can polish gold, lock it up, take it out and admire it. But it will never hand you a single rupee, grow a single grain of wheat, or become one gram heavier. A hundred years of waiting leaves you exactly where you started: with the same shiny cube.

What the lesson really means

An asset is simply anything you own that has value — gold, land, a fixed deposit, a share. Buffett’s letter sorted all assets into three simple baskets, and this sorting is the heart of the lesson.

The first basket holds money-like assets — savings accounts, fixed deposits (FDs), and bonds (a bond is a loan you give to a company or government, which pays you interest). These feel the safest. Their danger is quiet: inflation, the slow yearly rise in the price of everything, keeps nibbling at what your money can buy. The amount in the passbook grows, but what it can purchase often grows much less.

The second basket holds assets that just sit. Gold is the king of this basket. Buffett described its two weaknesses in one line: gold is “neither of much use nor procreative”. Procreative is just a formal word for “able to produce offspring”. A buffalo gives you milk every day and a calf every year or two. A mango tree gives you mangoes every summer. Gold gives you neither milk nor mangoes nor interest nor rent. One tola kept for a hundred years is still exactly one tola. So the price of a sitting asset can rise for only one reason: the hope that the next buyer will pay more for it than you did. Nothing inside it is growing; only the queue of buyers outside is changing.

The third basket holds assets that work: a farm, a shop, a flat that earns rent, and — this is the key one for us — a share. A share is not a lottery ticket or a blinking price on a screen. It is a small ownership slice of a real, working business. If the business behind your share sells soap or medicines or software at a profit, then a tiny part of every sale, in every corner of the country, belongs to you. Working assets do something for you every single year you hold them.

Why working assets win over long years

A working asset pays you twice. First, it produces something every year — crops from the farm, rent from the flat, profit from the business. Second, that yearly produce can be planted back to make the asset itself bigger — the shop’s profit opens the second shop, the company’s profit builds the next factory. This is compounding: your money earns, and then those earnings start earning too, like interest on interest, or a snowball growing as it rolls downhill. A sitting asset has no second engine. It cannot plant its gains back into itself, because it produces no gains to plant. Its only hope is a higher price from the next buyer.

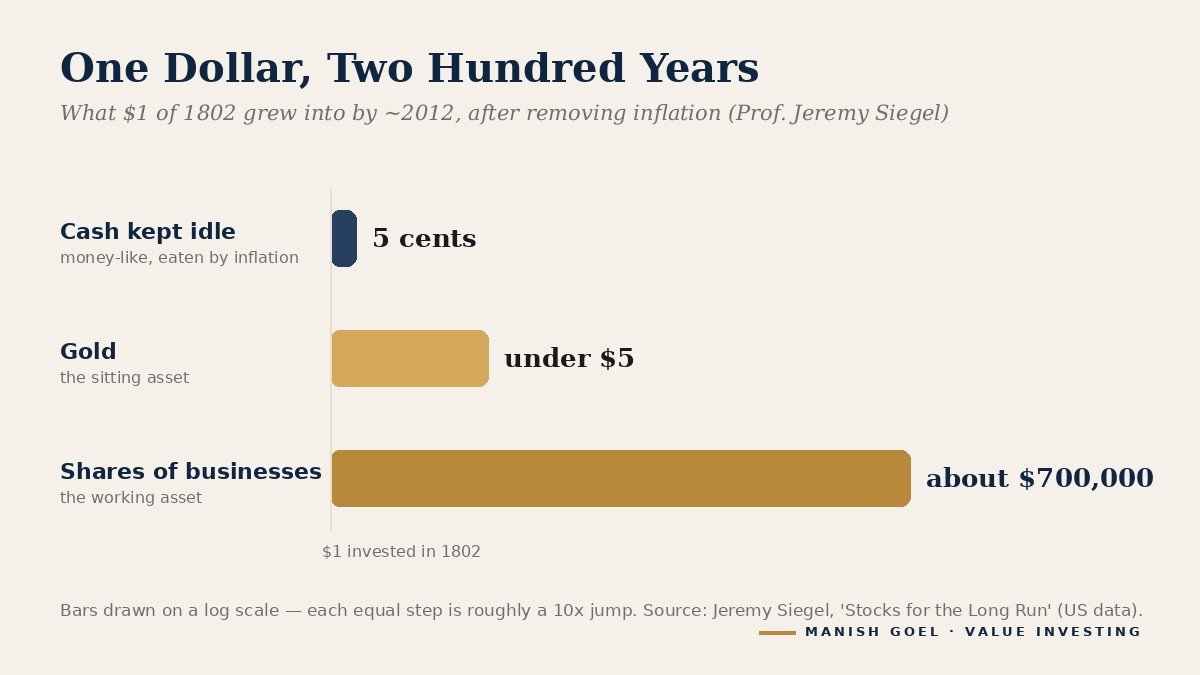

Over short periods, this difference hides. Over long periods, it becomes the whole story. Jeremy Siegel, a professor at Wharton, one of America’s most famous business schools, measured this across more than two hundred years of American records in his well-known book “Stocks for the Long Run”. After removing inflation, one dollar invested in shares in 1802 grew to roughly 700,000 dollars of buying power over those two centuries. The same one dollar in gold grew to less than five dollars. And one dollar simply kept as cash shrank to about five cents. The working asset did not win by a small margin. It won by a margin so large the chart can hardly hold both lines.

Now, let us be completely fair to gold, because fairness is part of honest investing. Over the last twenty-five years, gold’s price has climbed a great deal, and Indian families who held it have done well, especially measured in rupees. Buffett’s lesson is not that gold’s price can never rise — it can, and it has. The lesson is about what an asset does while you hold it. Gold sits in the locker and waits for the mood of buyers. A good business works every day of every year — through festivals and slowdowns, monsoons and elections — like a set batsman who keeps taking singles even when no boundaries come. Gold also has real and honourable roles in an Indian home: it carries tradition, it adorns weddings, and it is a trusted cushion for the darkest emergency. The mistake is not owning gold. The mistake is expecting the sleeping asset to do the working asset’s job.

India’s own cube: the 25,000 tonnes in our lockers

Here is a number worth sitting with. The World Gold Council, the global body that studies the gold market, estimates that Indian households and temples together hold roughly 25,000 tonnes of gold — the largest private holding of gold anywhere on earth, recently valued at around 2.4 trillion dollars. That is more gold than the official reserves of the world’s ten biggest central banks put together (a central bank is a country’s main bank, like our Reserve Bank of India). If Buffett’s imaginary world cube is 68 feet on a side, then India’s homes hold a very large slice of it — bangle by bangle, coin by coin.

This is not something to scold anyone about. It shows how deeply Indian families believe in saving, and saving is the raw material of all wealth. The question the lesson asks is gentler: what if even a modest part of the money we add to the locker each year were also put to work as ownership in good businesses? Raamdeo Agrawal, one of India’s most respected investors and the co-founder of the broking house Motilal Oswal, has published a detailed “Wealth Creation Study” nearly every year since the 1990s. Study after study circles the same message: India’s lasting investment fortunes have been built by people who owned good businesses and stayed with them for many years — owners of the shop downstairs, not only keepers of the pouch upstairs.

How you can use this lesson

You do not need a single complicated tool to apply today’s idea. Three simple habits are enough.

First, before buying any asset, ask one question: what will this earn while I hold it? A flat earns rent. An FD earns interest. A share earns you a slice of a business’s yearly profit. If your honest answer is “nothing — I am only hoping the price goes up”, then know clearly that you are not holding a working asset; you are only betting on the next buyer’s mood. Sometimes that bet pays. But it is a bet, not a business.

Second, when you buy shares, remember you are buying the shop, not the price tag. A share is only as good as the business behind it. So look for the marks of a high-quality business, the kind the great investors have always hunted: it earns a strong profit on the money it uses, it carries little debt (borrowed money, which can sink a business in bad times), it produces real cash year after year and not just profits on paper, and it is run by honest, capable people. Judge the shop the way you would judge a shop you were buying in your own bazaar. The daily share price is just noise from the crowd outside it.

Third, give gold its right seat — just not the driver’s seat. Keep gold for what it does beautifully: tradition, ornament, and a cushion for true emergencies, exactly as your family has always done. But let patient, regular investing in working assets — good businesses held for long years — carry the main load of building your future wealth. The cube can decorate the journey. Only the working farm can power it.

Key takeaways

- Assets come in three baskets: money-like (FDs, bonds), sitting (gold), and working (farms, shops, rental flats, shares). Know which basket you are buying.

- Buffett’s famous cube: all the world’s gold, melted together, produces nothing in a hundred years — “you can fondle the cube, but it will not respond.”

- A working asset pays you twice — yearly produce plus growth — and that second engine is compounding, the greatest force in investing.

- Gold has honourable roles in an Indian home — tradition and emergency cushion — but a sitting asset should not be asked to do a working asset’s job.

- A share is a slice of a real business: judge its quality — strong profits on capital, low debt, real cash, honest promoters — the way you would judge a shop you were buying.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.