Value Investing — Educational Series

A question you should never ask a barber

Imagine you walk up to your neighbourhood barber and ask him a simple question. “Do I need a haircut?” What will he say? You already know. He will look at your head, nod seriously, and say yes. He is not a bad man. He may be the friendliest person on your street. But his income depends on your answer being yes. Every haircut he recommends puts money in his pocket. His advice and his interest are mixed together, like sugar dissolved in tea. You cannot separate one from the other.

Old-timers on Wall Street (America’s stock market street) turned this into a famous warning: never ask a barber whether you need a haircut. Warren Buffett, the world’s most famous investor, has repeated it for decades. At his company Berkshire Hathaway’s annual meeting in 1994, he used it to explain why big companies receive poor advice on buying other companies. The bankers giving that advice earn their fee only when a deal actually happens. So, somehow, the advice is almost always “do the deal”.

India has its own versions of the barber question. Ask a sweet-shop owner whether you should eat more mithai. Ask a jeweller whether this is a good time to buy gold. Ask a property dealer whether prices in his colony will go up. You can guess every answer before you ask. None of these people are lying to you on purpose. Each one is simply standing where his earnings point him.

Charlie Munger, Buffett’s business partner for almost sixty years, spent his whole life studying this one force. He called it the power of incentives. He believed most people, even very clever people, badly underestimate it. Understanding this single idea can protect your savings better than many fancy formulas in finance. That is today’s lesson.

What it really means

An incentive is simply the reward a person gets for behaving in a certain way. A salary is an incentive to come to work. A commission (a cut of the sale money, paid to the seller) is an incentive to sell more. Marks are an incentive to study. A tip is an incentive to serve customers well. Incentives are everywhere, quietly steering human behaviour, the way the slope of a road quietly steers rainwater.

In 1995, Munger gave a now-legendary talk at Harvard University called “The Psychology of Human Misjudgment”. In it, he listed the standard ways our minds fool us. At the very top of his list, as cause number one, he placed the power of incentives. His most quoted line says it all: “Show me the incentive and I will show you the outcome.” In plain words: tell me how people are paid, and I will tell you how they will behave, before they behave.

Here is the part most people miss. An incentive does not just change what a person does. It slowly changes what the person believes. Munger called this incentive-caused bias (a bias is a lean in our thinking, like a cycle wheel that is slightly bent and always pulls to one side). The insurance agent who earns a fat commission on a particular policy does not feel like a salesman tricking you. Over time, he honestly starts believing that policy is the best thing for you. His mind bends towards his income, without his permission, and he does not even feel the bend.

Think of a kirana shop. Suppose one soap company quietly gives the shopkeeper a bigger margin (margin means his profit on each packet) than the others. Watch what happens. When you ask “bhaiya, which soap is good?”, he points to that brand. He is not cheating you. Ask him privately and he will swear it really is the better soap. The extra two rupees per packet have, over months, written his honest opinion for him. An old proverb says it perfectly: whose bread I eat, his song I sing.

This is why the polite English phrase “conflict of interest” matters so much to investors. A conflict of interest simply means the adviser’s benefit and your benefit are pulling in different directions. The barber rule is just a homely way of spotting it.

Why it works: the plain logic

The logic is simple enough for a child. People repeat what gets rewarded. People stop what gets punished. Reward a batsman only for sixes, and do not be surprised when he stops playing careful defensive shots; you built a T20 player, not a Test player. Reward a salesman only for sales, and do not be surprised when he sells to people who should not buy. The behaviour follows the reward, the way a plant grows towards sunlight.

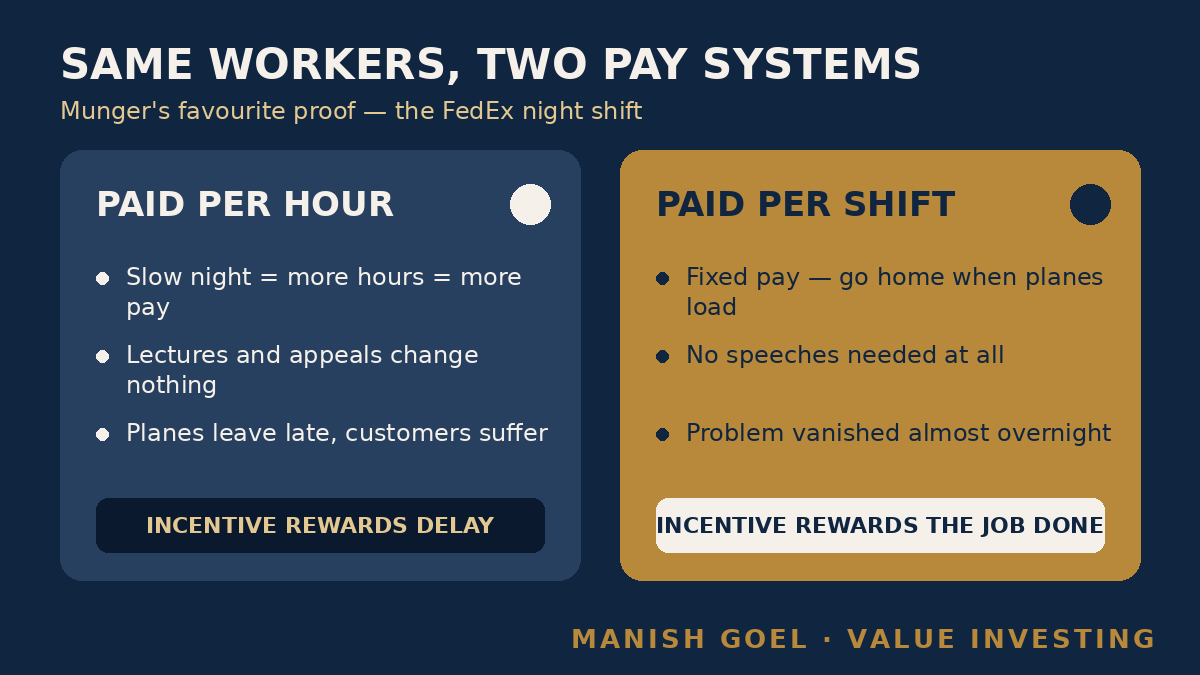

Munger’s favourite proof was the FedEx story. FedEx, the American courier company, moves parcels through one central airport every night. Parcels must shift quickly from plane to plane in the dark hours, or the whole system fails and customers get their packets late. For years, the night workers simply could not finish on time. Managers gave lectures. They made appeals. They tried everything. Nothing worked. Then someone noticed the real culprit: the workers were paid per hour. The slower the night went, the more hours they earned. Going slow was, quite literally, the well-paying choice. So FedEx changed one thing. Workers would now be paid per shift, a fixed amount, and everyone could go home the moment all planes were loaded. The problem that years of lecturing could not solve vanished almost overnight.

Notice the deep lesson inside that story. The workers were never lazy or wicked. The pay system was faulty. When the behaviour around money looks strange, do not rush to blame character. First check the incentive. Fix the incentive and you usually fix the behaviour.

Munger added a confession that should make all of us humble. He said he had been in the top five percent of his age group, all his life, in understanding the power of incentives — and yet, every single year, some new example still surprised him, and he realised he had underestimated it again. If one of the sharpest minds in investing kept underestimating this force, an ordinary saver should treat it with double respect.

One more thing before the stories. Incentives are not evil. They are a tool, like fire. The interest on a fixed deposit (FD) is an incentive to save instead of spend. A SIP (systematic investment plan — a fixed amount auto-invested every month) is really a clever incentive trick you play on yourself, so that saving happens before spending can. The same force that mis-sells policies can also build your wealth, if you point it in the right direction.

When incentives go wrong: one American story, one Indian story

First, the American story. Wells Fargo was one of America’s largest and most respected banks. Its managers pushed a target called cross-selling: selling many extra products — more accounts, more cards — to each existing customer. Branch staff had strict sales targets, and bonuses hung on those targets. Under that pressure, thousands of employees began quietly opening accounts that customers had never asked for. By 2017, investigators estimated that roughly 35 lakh unauthorised accounts had been created. In September 2016, regulators fined the bank 185 million dollars, and in 2020 Wells Fargo agreed to pay 3 billion dollars (over twenty thousand crore rupees) to settle the matter. Here is the thought worth keeping: Wells Fargo never hired five thousand cheats. It hired ordinary people and handed them a dangerous incentive. The incentive did the rest.

Now the Indian story, which many families experienced personally. In the 2000s, a product called the ULIP (unit linked insurance plan — a policy that mixes insurance cover with stock market investment) became the hottest thing agents sold. Why were agents so much in love with ULIPs? The commission. In those years, a very large slice of your first-year premium — often 30 to 40 paise of every rupee, and in some early plans even more — went to the seller as commission. So ULIPs were sold to everyone: retired uncles, young parents, people who needed simple insurance, people who needed none. Many buyers were told it was a “three-year plan”, when three years was only the lock-in (the period when your money cannot be taken out), not the time needed to actually benefit. Complaints flooded in. In September 2010, IRDA (the insurance regulator, the referee of the insurance industry) changed the rules: charges were capped, commissions on these plans dropped to roughly 7 to 10 percent, and the lock-in was raised from three years to five. And then came the most educational part. Almost overnight, many agents lost their enthusiasm for ULIPs and drifted towards other products that still paid higher commissions. The product had not changed. The customer had not changed. Only the incentive had changed — and the “expert advice” changed with it.

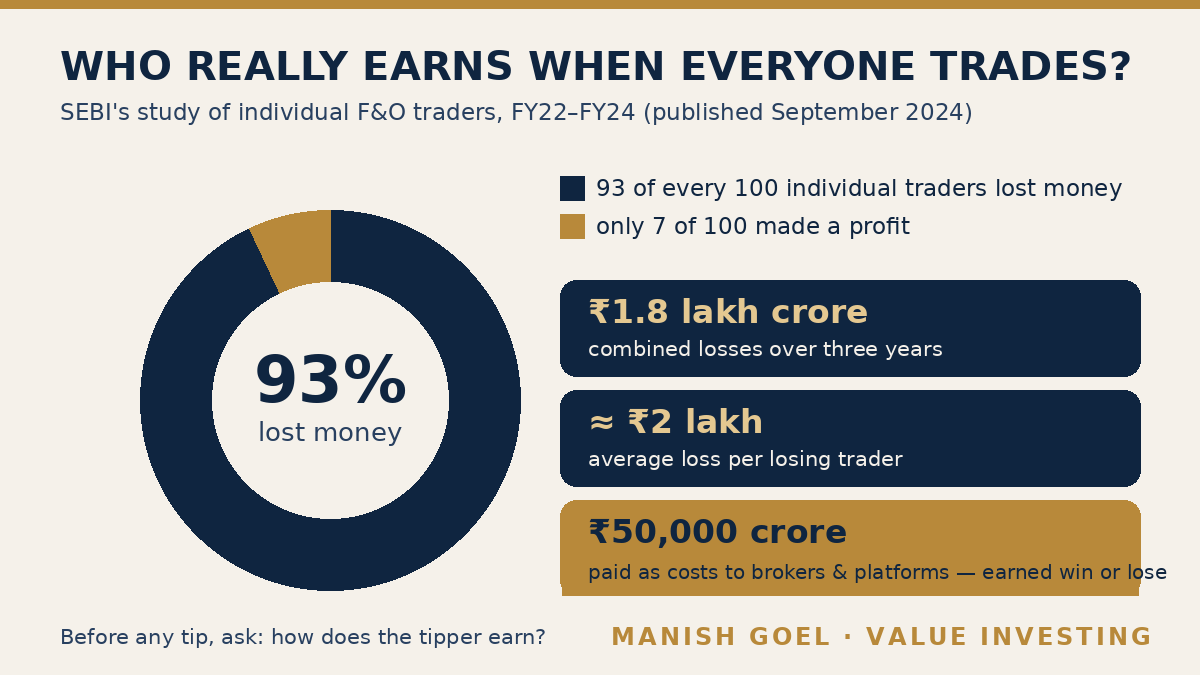

There is a third story running live on your phone right now. Free tip groups on WhatsApp and Telegram. Influencers shouting about quick profits in F&O (futures and options — side-bets on where a price will go next, rather than ownership of a business). Trading apps that celebrate every trade with confetti. Before trusting any of them, look at the incentives. A broker (the middleman who executes your trades) earns brokerage — a fee on every single trade — whether you win or lose. A tip-group operator often earns by quietly selling his own shares to the crowd he has excited. SEBI, the stock market regulator, studied individual F&O traders and published the results in September 2024: between FY22 and FY24, 93 out of every 100 individual traders lost money. Their combined losses crossed ₹1.8 lakh crore, with the average loser down about ₹2 lakh. And while traders bled, roughly ₹50,000 crore went out as transaction costs — earned by the ecosystem that kept urging everyone to trade more. The barber rule, playing out at national scale.

How you can use it

You do not need a finance degree to use Munger’s lesson. You need one habit and two preferences.

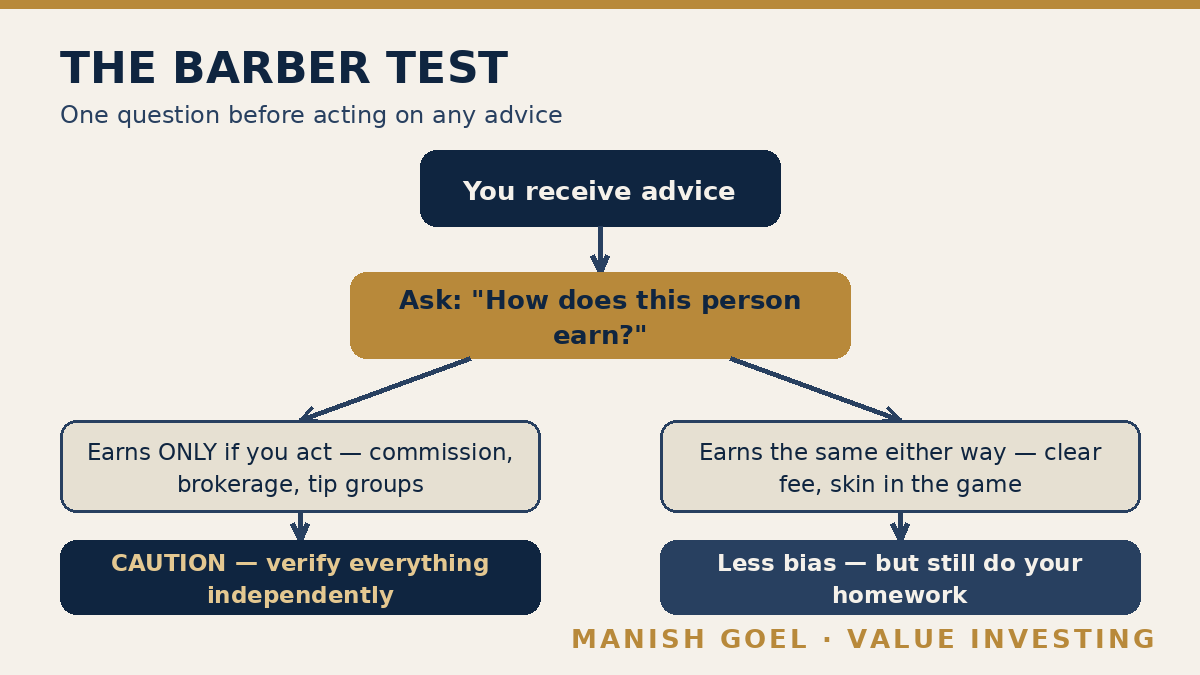

First, before acting on any financial advice, ask one question: “How does this person earn?” Ask it about the relative recommending a policy, the influencer recommending a trade, the free Telegram group recommending a hot stock, and yes, even a publication like this one. If the honest answer is “he earns only if I act”, slow down and verify everything independently. Remember that free tips are usually the most expensive advice in the world, because when the advice is free, you are not the customer — you are the product.

Second, prefer businesses where the people in charge eat their own cooking. When you study a company, look at its promoters (the founding family or controlling owners who run the company). Do they hold a large stake in the company’s shares? Is that stake free of pledging (pledged shares are shares handed to a lender as security for a loan — a quiet warning sign)? Are their salaries sensible, so that they get rich mainly the same way you do — through the long-term rise of the same shares you hold? When the owner’s reward can only grow if your reward grows, his incentive becomes your bodyguard, working silently for you every day. All of this is public: the shareholding pattern, pledge details and managers’ pay sit in every annual report and on the stock exchange websites. Checking them takes minutes, and it is one of the simplest quality checks an ordinary investor can do.

Third, set your own incentives wisely, because the rule applies to you too. Automate the good behaviour: a SIP auto-debit on salary day makes saving the default, so your patience never has to fight your temptation. Avoid apps and products that reward activity — trading again and again — instead of outcomes. And if you take professional advice, prefer an adviser paid through a clear, visible fee rather than hidden commissions, so that his earnings do not depend on making you act. You cannot remove incentives from the world. But you can stand on the right side of them.

Key takeaways

- Never ask a barber whether you need a haircut: a person paid to sell will rarely advise you not to buy.

- Incentives change beliefs, not just behaviour — most mis-sellers honestly believe their own pitch, which is exactly what makes them convincing.

- Munger’s rule: “Show me the incentive and I will show you the outcome.” Check how people are paid before you trust what they recommend.

- Free tips are the costliest advice: when advice is free, you are the product. Always ask, “How does this person earn?”

- Favour companies whose promoters hold large, unpledged stakes and modest salaries — owners who eat their own cooking are a genuine quality signal.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.