Value Investing — Educational Series

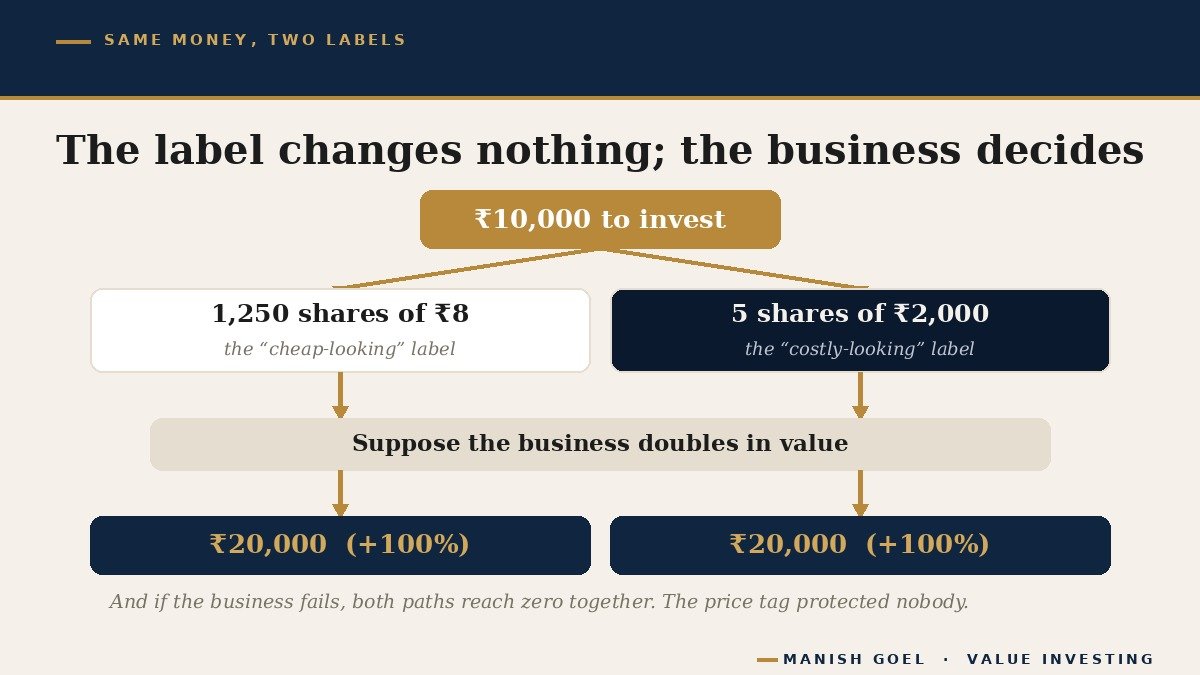

Two friends met for evening tea. Ramesh could not stop smiling. “I have found a very cheap share,” he said. “It costs only ₹8. With my ₹10,000 I will get more than twelve hundred shares. Look at the share you keep talking about — it costs ₹2,000. With the same money you get only five. Mine is cheaper, and it has more room to grow.”

Suresh stirred his tea and asked one quiet question. “Cheaper than what?”

Almost every new investor in India has stood where Ramesh is standing. We compare prices all day long — tomatoes at ₹40 a kilo against tomatoes at ₹60 a kilo, petrol at one pump against petrol at another — and it works, because a kilo is a kilo and a litre is a litre. So when we see one share priced at ₹8 and another at ₹2,000, the same habit switches on. The small number feels like a bargain. The big number feels out of reach.

In the share market, that feeling is an illusion. The price tag on one share — by itself — tells you nothing. Not whether the company is big or small. Not whether the business is strong or weak. Not how much “room to grow” it has. Nothing. Today’s lesson explains what that number on the screen actually is, why our mind misreads it, and what an ordinary investor should look at instead. One thing this essay will never do is tell you whether any share is worth buying — it only clears up a confusion about a label.

What the price of one share really is

Start with what a share is. A share is one slice of a company — a small piece of its ownership (this is why shareholders are called part-owners of the business). And here is the detail most beginners are never told: every company decides for itself how many slices to cut its ownership into.

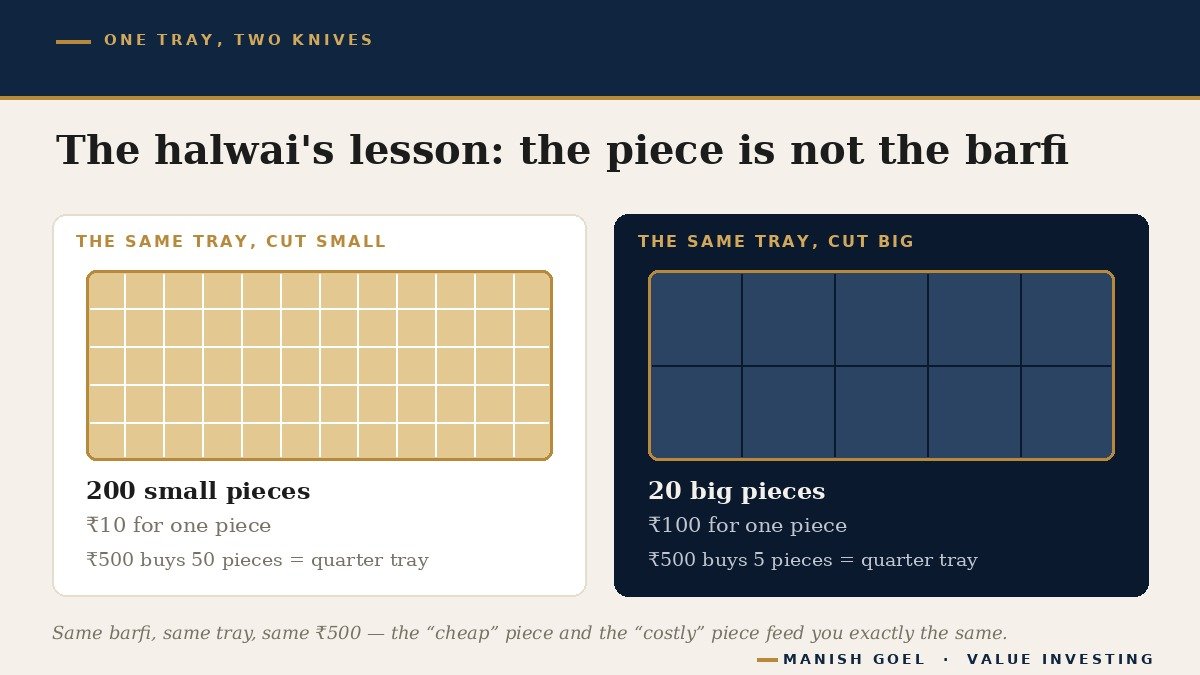

Think of a halwai who has made a large tray of barfi. He can cut the tray into 20 big pieces and sell each one at ₹100, or he can cut the very same tray into 200 small pieces and sell each one at ₹10. Is the ₹10 piece “cheaper” than the ₹100 piece? No. It is simply a smaller piece of the same tray. Whether you spend ₹500 on five big pieces or on fifty small ones, you carry home exactly the same amount of barfi.

Shares work the same way. Imagine two companies, each with a total market value of ₹100 crore (market value, also called market capitalisation, is simply the price of one slice multiplied by the number of slices — the price tag on the whole tray). Company A has cut itself into 10 crore shares, so one share trades near ₹10. Company B has cut itself into just 5 lakh shares, so one share trades near ₹2,000. Same size of tray. Different knife. A person who says the ₹10 share is “cheaper” is only saying that one company cut smaller pieces.

This is also why two everyday market events change nothing real. In a share split, a company cuts its existing pieces into smaller ones (one ₹10 piece becomes two ₹5 pieces). In a bonus issue, it hands existing owners extra pieces free of cost. In both cases the tray — the business, its sales, its profits — stays exactly the same size; there are simply more pieces, each one smaller. Your ₹10,000, invested either way, buys the same portion of the same business.

One more label worth decoding, because it confuses many people: face value. Face value is the original printed value of a share — usually ₹1, ₹2, ₹5 or ₹10 in India — fixed when the company first divided itself on paper. It is a bookkeeping label, like the year printed on a coin. It is not what the share is worth, and it is yet another reason why the number on the screen differs so wildly from company to company.

Why the small number fools our mind

If the arithmetic is this simple, why do so many of us fall for the ₹8-versus-₹2,000 comparison? Because three very human feelings get in the way.

First, we are trained unit-price shoppers. In the sabzi mandi, comparing the price per kilo is exactly the right thing to do, because every kilo of tomatoes is the same. But one share of Company A and one share of Company B are not the same unit. They are pieces of different sizes, cut from different trays, by different knives. Comparing their price tags is like comparing one piece from the halwai’s counter with one piece from the shop next door without asking how big either piece is, or how good either barfi is.

Second, a bigger count feels like more wealth. Twelve hundred shares simply sound richer than five shares, the way ten notes of ₹100 can feel like more money than one note of ₹1,000. But your wealth is decided by the value of what you hold, not by how many pieces of paper it is divided into. ₹10,000 is ₹10,000 — in twelve hundred slices or in five.

Third — and this is the costliest one — the small number seems to have “more room to grow.” Going from ₹8 to ₹16 feels like a small, easy hop. Going from ₹2,000 to ₹4,000 feels like climbing a mountain. Yet both are exactly the same journey: a doubling. And a share’s price doubles for one reason only — because the market comes to believe the business behind it is worth twice as much. The tray has to grow for every piece to grow. An ₹8 price tag does not make that one bit easier. Prices move in percentages, not in “small numbers” and “big numbers.”

There is a harder truth hiding behind this illusion, and it is better heard from a friend than learnt from a loss. People who sell tips know this psychology very well. That is why the messages that reach your phone so often read “only ₹5 per share — buy before it becomes ₹50.” The small number is the bait: it makes the punt feel affordable and the dream feel near. The market regulator (the government-appointed body that supervises our stock market) has cautioned investors again and again about share tips pushed through SMS, WhatsApp and social media. Very low-priced shares of small, weak companies are a favourite playground for such operators, because a thin, little-traded share is easier to push up and dump on latecomers.

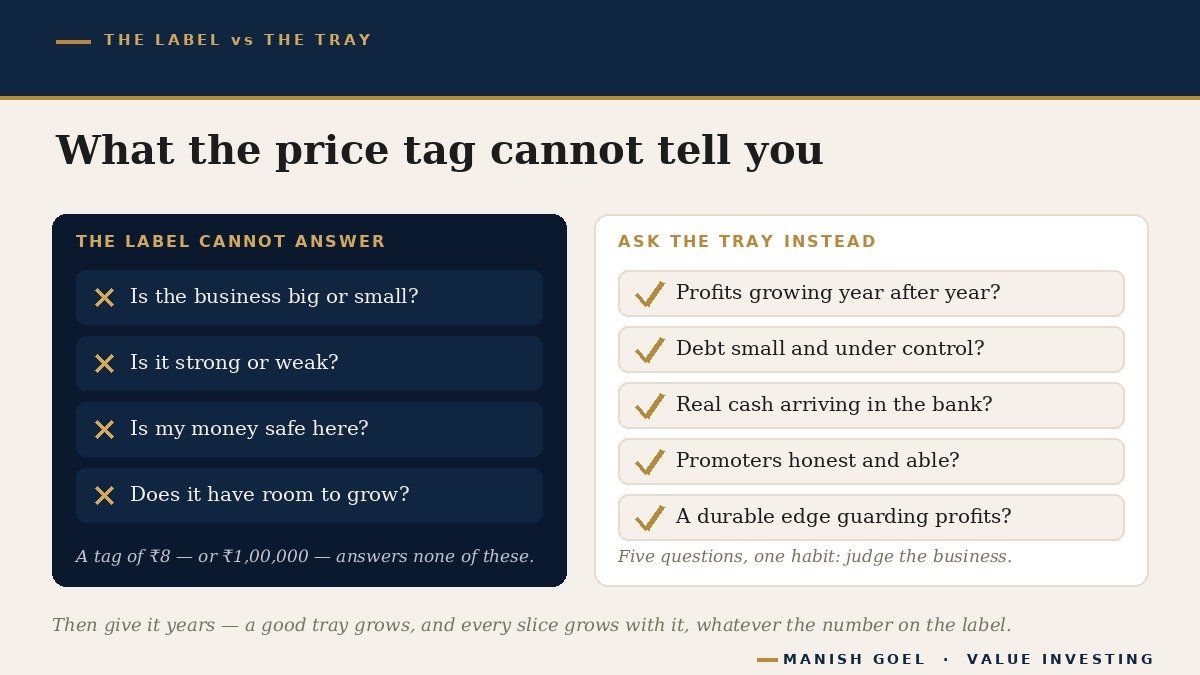

Be careful with the opposite conclusion too. A low price tag does not automatically mean a bad business, just as a tag of one lakh rupees does not mean a good one. That is the whole point of today’s lesson: the label, by itself, proves nothing in either direction. It is simply the size of one slice.

Two true stories, from two ends of the price scale

Peter Lynch, who ran America’s famous Magellan Fund and wrote the beloved beginner’s book One Up on Wall Street in 1989, kept a list of the silliest things he heard ordinary investors say. One entry on that list was exactly Ramesh’s sentence: “It’s only $3 a share — what can I lose?” Lynch’s answer was blunt. Whether you pay $50 a share or $3 a share, if the business behind it fails and the price goes to zero, you lose everything you put in. A person who put $25,000 into a “cheap” $3 share loses every rupee of it just as surely as his neighbour who paid $50. The small price tag protected nobody. A weak business at a low price is not safety; it is a weak business.

Now the other end of the scale. Warren Buffett’s company, Berkshire Hathaway, has never split its original shares in all the decades since he took charge of it in 1965 — the tray was never recut. Piece by piece, as the businesses inside it earned and grew, the price of that one uncut slice climbed. By July 2026, one single share of Berkshire Hathaway traded around 7.4 lakh US dollars — more than six crore rupees for one share. In his 1983 letter to shareholders, Buffett explained why he refuses to cut the pieces smaller to make the price tag look friendlier: “Were we to split the stock or take other actions focusing on stock price rather than business value, we would attract an entering class of buyers inferior to the exiting class of sellers.” In plain words: he wants owners who read the tray, not the tag. (Years later the company did create a separate, smaller class of shares so that people with modest savings could also invest — but the original slice was never recut.)

India has its own famous uncut slice. MRF, the Chennai tyre maker, has not split its share in decades — its last bonus issue was back in the 1970s — and in June 2023 it became the first share in India to cross a price of ₹1,00,000. In July 2026 it trades near ₹1.3 lakh per share. Newspapers love to call it “India’s costliest share.” But read the label correctly: that price tells you only that the company is divided into very few pieces — about 42 lakh shares, where many companies of similar size have crores of them. It does not tell you the business is wonderful, and it does not tell you the business is poor. Meanwhile, dozens of shares with tags below ₹10 have quietly gone to zero over the years when the businesses behind them crumbled — their “cheapness” saved no one.

These stories are history, never advice. Nothing here says Berkshire or MRF is a share to buy, avoid or hold — the lesson is only this: at ₹8 and at ₹1,00,000 alike, the people who went by the label learnt nothing, and the people who studied the business learnt everything that mattered.

How you can use this lesson

One: think in rupees invested, not in number of shares. Decide the amount you want to invest in a business — say ₹10,000 — and let the share count be whatever the division throws up. Five shares or twelve hundred, your money grows and falls by the same percentage either way. When you review your holdings, look at the amount invested and the percentage change, and let the share count sit quietly in a corner of the statement where it belongs.

Two: strike “it’s only ₹5” from your list of reasons. A share’s price tag — small or big — should never appear among your reasons for buying it. And when a message, a video or a well-meaning cousin presents the low price itself as the main attraction, treat that as a warning bell, because the honest attractions of a business sound completely different: its profits, its products, its customers, its promoters.

Three: judge the tray, not the piece. Before your money goes anywhere, ask the questions that the price tag cannot answer. Do sales and profits grow steadily, year after year? Is debt (borrowed money) small enough that the business is not working for its lenders? Does real cash actually arrive in the bank from operations, and not just profit on paper? Are the promoters (the founding owners who run the company) honest and able? Does the business hold some durable edge — a trusted brand, a locked-in customer, a cost nobody can match — that protects its profits? Each of these has been a full lesson of its own in this series. Together they describe the quality of the barfi. That is what you are buying — never the size of the piece.

Key takeaways

- A share is one slice of a business, and every company chooses how many slices to cut. The price of one share tells you the size of the slice — never the size or quality of the business.

- A ₹10 share is not cheap and a ₹1,00,000 share is not costly. The price tag alone can never tell you whether a share is a bargain or a mistake — in either direction.

- Think in rupees invested, not share counts. The same ₹10,000 grows by the same percentage whether it is divided into five pieces or twelve hundred.

- “More room to grow” is the costliest myth of all: ₹8 to ₹16 and ₹2,000 to ₹4,000 are the same journey, and both need the business itself to double.

- Tip messages shout small numbers because small numbers feel safe. Judge the tray instead: growing profits, low debt, real cash, honest promoters, a durable edge — and then give it years.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.