Value Investing — Educational Series

The message arrives on a quiet Tuesday afternoon. “Pre-approved personal loan: ₹5 lakh in your account in ten minutes. One tap.” That same week, a colleague slides his phone across the canteen table. He has been trading options (contracts that let you bet on a share’s next move by putting down only a small deposit), and his screen this month is a happy green. The market is rising. The news is cheerful. And a thought — quiet, patient, reasonable-sounding — walks into your head and sits down: my plan is fine. I just need more money inside it.

On paper, the idea looks like innocent arithmetic. Borrow at twelve per cent, earn fifteen per cent in shares, keep the difference. Banks lend other people’s money all day. Businesses run on loans. Why should you not?

Because of one rule — possibly the simplest rule in all of investing, and the one Warren Buffett has repeated more insistently than almost any other: never invest with borrowed money. Today, in very plain words, we will see what borrowing to invest actually means, why arithmetic that looks so friendly on the way up turns violent on the way down, what happened when the cleverest team ever assembled in finance tried it, what India’s own market learnt about it the hard way — and a three-step ladder that keeps an ordinary investor permanently out of its reach.

What “investing on borrowed money” really means

Leverage (borrowed money used to make an investment bigger than your own savings allow) comes dressed in many uniforms. A personal loan taken “for the market”. A margin trading facility (an arrangement where your broker lends you money so you can buy more shares than your cash can pay for). Gold or a flat pledged to raise money for a “sure thing”. And the most popular uniform of all today: futures and options, or F&O (exchange contracts where a small deposit, called margin, controls a position many times larger). The clothing differs; the body inside is the same. Every one of these lets you buy more than your own money can buy.

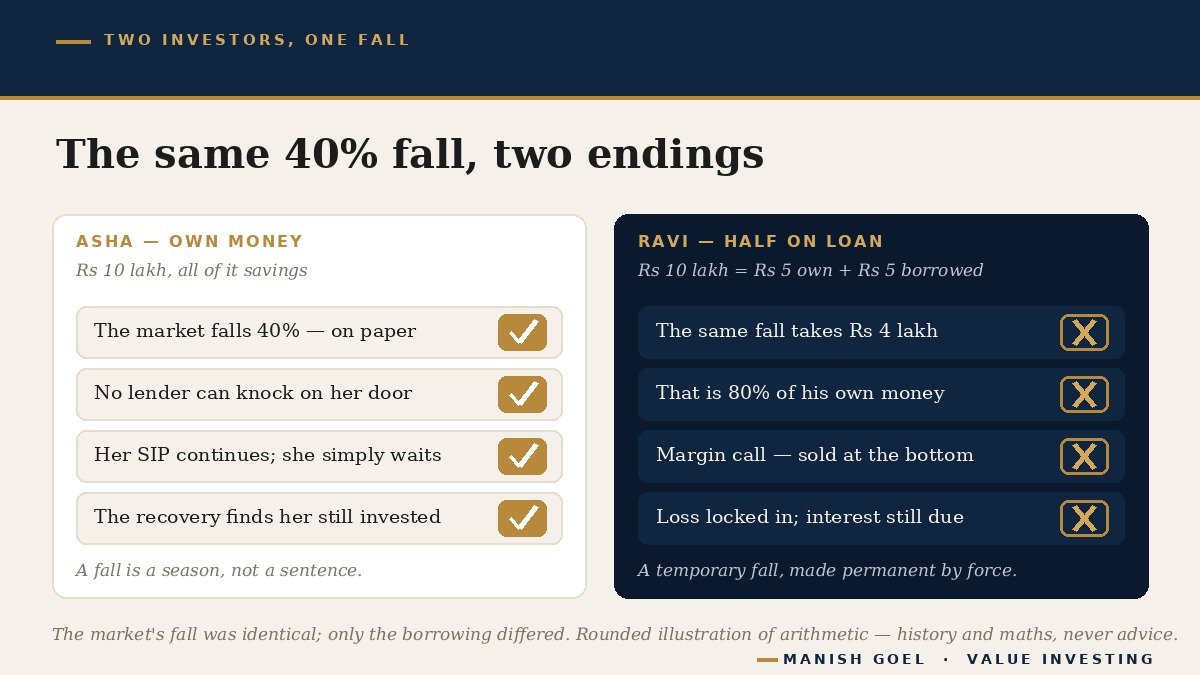

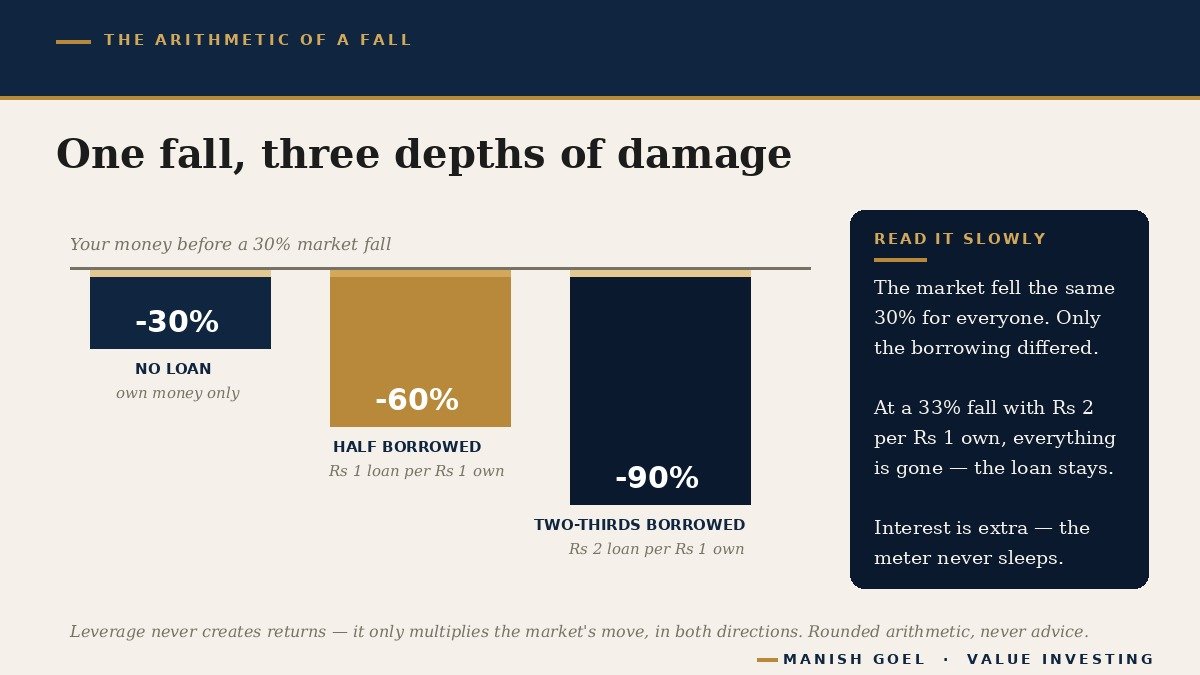

And that is exactly the attraction. Suppose you invest ₹10 lakh of your own and the market rises twenty per cent: you make ₹2 lakh. Add a borrowed ₹10 lakh, and the same rise hands you ₹4 lakh, minus interest. In a rising market, leverage feels like intelligence. Every borrower looks like a genius while prices climb, the way every swimmer looks graceful while the water is calm.

But a knife with two edges cuts on the way back too. The same twenty per cent move, downward, now takes ₹4 lakh out of a ₹10 lakh pocket — a forty per cent wound to your own money from a twenty per cent fall in the market. Notice what leverage actually did there. It did not create any return. It cannot. It only multiplies whatever the market does — in both directions — while the interest meter runs like an auto-rickshaw meter in a traffic jam. The market may stand still for a year. The meter never does.

Buffett’s late partner Charlie Munger compressed all of this into one line that Buffett loves to repeat. Quoting him in a television interview in 2018, Buffett said: “My partner Charlie says there is only three ways a smart person can go broke — liquor, ladies and leverage.” Then came the honest footnote: the first two, Buffett explained, were added mainly because they begin with L. The one that actually does the breaking is leverage.

Why borrowed money breaks the market’s one promise

Here is the deal the share market has always offered. Held patiently for many years, good businesses have rewarded their owners wonderfully. But the market signs no timetable. It promises nothing about the road in between — and the road in between includes falls that would frighten anyone. Falls are not a defect in the machine. They are the entry fee.

No company demonstrates this better than Buffett’s own. Berkshire Hathaway, one of the great wealth-creation stories in history, has seen its share price cut roughly in half four separate times: down about 59 per cent in the mid-1970s, about 37 per cent in the crash of 1987, about 49 per cent around 2000, and about 51 per cent in 2008–09. These are rounded numbers from history, never advice about any share. Buffett printed that painful table in his 2017 letter to shareholders himself, and wrote beneath it: “This table offers the strongest argument I can muster against ever using borrowed money to own stocks.”

Why is a table of falls an argument about borrowing? Because the same fall treats the two kinds of investors completely differently. The investor who used her own surplus money still owns the one thing that makes equity investing work: her own time. She can wait a year. She can wait five. Her shares in good businesses are like a field in a dry season — the farmer who owns his field outright can wait for the next monsoon, because nobody can ring his doorbell and demand the field back. For her, a fall is a season, not a sentence.

The borrowed investor has sold that right away, usually without noticing. His two new enemies work in shifts. Interest works the day shift: EMIs (fixed monthly loan repayments) fall due whether the market rises, falls or sleeps. And the margin call works the night shift. A margin call is the broker’s demand that you immediately deposit more money because your shares have fallen — and if you cannot, the broker sells your shares at the current low price to protect the loan. Imagine a housing loan where, any week your flat’s market price dipped, the bank could sell your flat within a day and post you a bill for the shortfall. Nobody would call that owning a home. That, precisely, is what owning shares on borrowed money is.

The forced sale is the heart of the tragedy, so look at it slowly. A fall in the market is temporary for the patient owner. The margin call converts that temporary fall into a permanent loss — at the bottom, by force, with the loan and its interest still standing. And Buffett points at a quieter injury too, in that same 2017 letter: “There is simply no telling how far stocks can fall in a short period. Even if your borrowings are small and your positions aren’t immediately threatened by the plunging market, your mind may well become rattled by scary headlines and breathless commentary. And an unsettled mind will not make good decisions.” Debt begins its damage long before any margin call arrives. It damages your sleep — and sleep is where patience lives. His conclusion from that letter deserves a place on the wall of every trading app: “it is insane to risk what you have and need in order to obtain what you don’t need.”

The cleverest people in the world already tried it

If intelligence could make borrowed money safe, a firm called Long-Term Capital Management would be running still. LTCM was an American fund launched in 1994 with what may be the finest team ever gathered in one trading room: sixteen partners, among them two men who would soon receive the Nobel Prize in economics, with perhaps three or four hundred years of combined experience between them. Their calculations were almost always right. But the profits on each calculation were small — so, to make small profits big, they borrowed enormously. At times the fund controlled more than twenty-five rupees of positions for every one rupee of its own.

In 1998, the world misbehaved. Russia suddenly stopped paying its government debt, frightened money stampeded across the globe, and prices moved in ways the models had called nearly impossible. The falls were violent; the lenders wanted their money back; positions had to be sold at the worst prices in living memory. Within a few months, four years of brilliant profits were gone, and the fund had to be rescued by a group of banks and quietly wound up. The men were not fools. They were the opposite of fools — and that was exactly Buffett’s point when he told the story to university students in Florida a few weeks later: “To make money they didn’t have and didn’t need, they risked what they did have and did need — and that’s foolish.” If you risk something that is important to you for something that is unimportant to you, he told the hall, it simply does not make sense.

India has taught the same lesson in its own languages. For decades, our market ran on an indigenous borrowed-money engine called badla — a system in which a buyer could carry his position forward without paying in full, effectively trading on borrowed funds at interest. Badla money fuelled the wild boom of 1992, and then deepened the historic crash that followed it, ruining lakhs of families who had never intended to be borrowers at all. After years of bans and reversals, India’s market regulator (the official body that supervises our stock markets) shut the system down for good in July 2001. The uniform changed; human nature did not.

Today the uniform is the F&O screen — leverage in its most concentrated form, where a small deposit controls a big bet and the clock works against you. In September 2024, India’s market regulator published a study of more than one crore ordinary Indians who traded equity F&O across three financial years. The findings deserve to be read slowly. Ninety-three out of every hundred lost money. The average loss was about ₹2 lakh per person. Added together, individual traders lost more than ₹1.8 lakh crore — enough to build entire highways — in three years. Against those hundred people stands Buffett’s remark to students at Notre Dame back in 1991: “You really don’t need leverage in this world much. If you’re smart, you’re going to make a lot of money without borrowing.”

How you can use this lesson

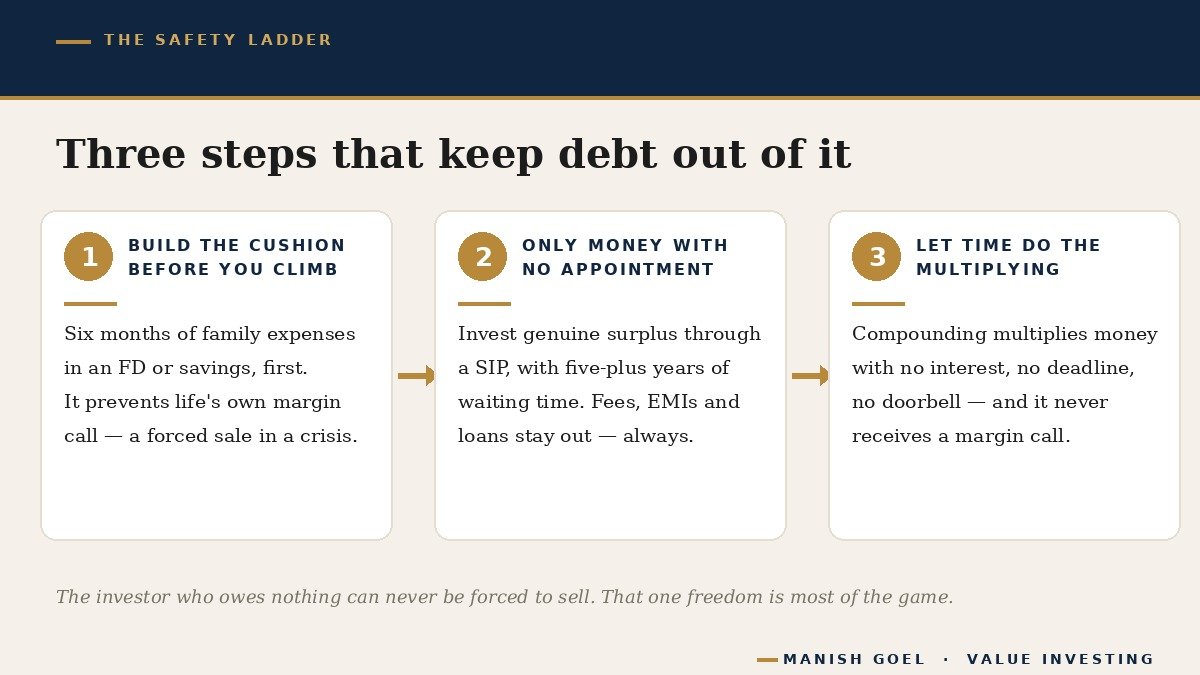

First, build the cushion before you climb. Keep six months of your family’s expenses in a fixed deposit or savings account before a single rupee goes into shares. This boring step quietly removes the most common forced sale of all — not the broker’s margin call, but life’s: the hospital bill or job loss that makes a family sell good shares at a bad time. A cushion buys you the right to be patient, and patience is the entire game.

Second, invest only money that has no other appointment. Money for school fees, EMIs, weddings or next year’s needs is not investment money — and borrowed money is the most appointed money of all: it belongs to someone else, on a schedule, with a meter running. Invest only your genuine surplus, ideally through a SIP (a Systematic Investment Plan, where a fixed sum goes into the market every month), with five years or more of waiting time. A simple test before you invest any amount: if this fell forty per cent on paper next year, would any EMI bounce, any fee go unpaid, any sleep be lost? If yes, it is not investment money yet.

Third, let time do the multiplying that you were tempted to let debt do. There is a legitimate multiplier available to every ordinary investor, and it charges no interest and issues no margin calls: compounding (your returns earning their own returns, the way interest earns interest on interest). Leverage tries to squeeze ten years of growth into one, and in exchange accepts a real chance of turning ten years into zero. Compounding does the opposite — it plays the long Test innings, scoring quietly, never getting out. The investor who chooses this multiplier needs no loan, hears no doorbell, and owes nothing to anybody while her money works.

Key takeaways

- Leverage (borrowed money used to invest) creates no returns of its own — it only multiplies whatever the market does, in both directions, while the interest meter runs even when the market sleeps.

- Deep falls visit even the greatest businesses — Berkshire Hathaway itself has halved four times in history. Own money can wait out a fall; borrowed money is often sold out at the bottom by a margin call, turning a temporary fall into a permanent loss.

- Intelligence is no protection: LTCM’s sixteen partners included two Nobel Prize winners, and borrowing still destroyed the fund within months in 1998.

- India’s own evidence is blunt — the badla system was banned in 2001 after fuelling boom and bust, and the market regulator’s 2024 study found 93 out of 100 individual F&O traders lost money, about ₹2 lakh each on average.

- The safe ladder: six months’ expenses in the bank first, then only genuine surplus into shares through a SIP for five-plus years, with compounding — never a loan — as your only multiplier.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.