Value Investing — Educational Series

Two neighbours build houses on the same street in the same summer. Both look solid. Both are freshly painted. Relatives visit both and say very nice things. For eight dry months, nothing separates the two houses. Then the first real monsoon downpour arrives. One roof holds. The other starts dripping into the bedroom. The paint never knew the difference. The rain knew it in one night.

Warren Buffett — the man many call the greatest investor of our age — has a one-line version of this story, and it has become one of the most repeated sentences in all of investing. In his 2007 letter to the shareholders of Berkshire Hathaway (his investment company), written just as a worldwide credit storm was gathering, he put it like this: “You only learn who has been swimming naked when the tide goes out.” He had been using versions of that line in his yearly letters since the early 1990s. It is short, it is funny, and it carries more protection for an ordinary saver than a hundred pages of finance.

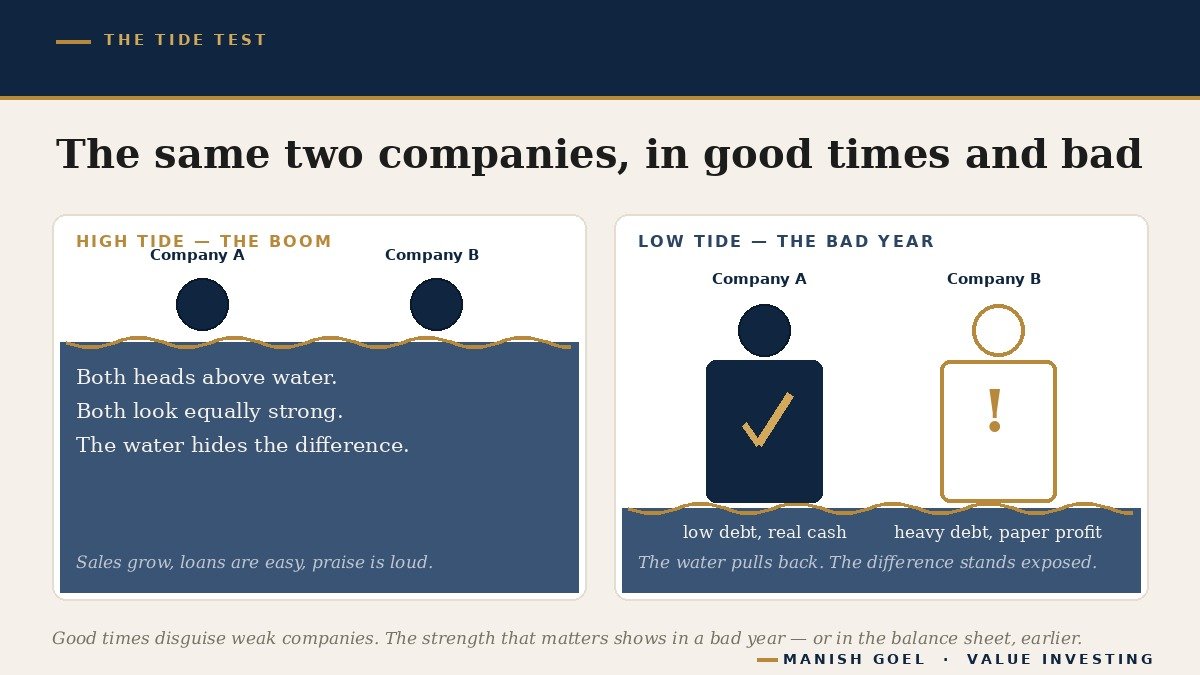

The picture is simple. When the tide is high, the water covers every swimmer. From the beach, the careful swimmer in proper swimwear and the careless one without it look exactly the same — two happy heads above the surface. Only when the water pulls back do you see who came prepared. Today’s lesson unpacks this idea in very plain words: what the tide is in the world of shares (small pieces of ownership in a company), what “swimming naked” means for a business, two real low tides that exposed the unprepared, and a short checklist you can use to spot a strong company — and to make your own family finances storm-proof too.

What the tide is, and what “naked” means

The tide is a good economy. It is the easy years: banks compete to hand out loans, customers are spending freely, order books are full, and the prices of most shares keep climbing. In years like that, almost every company looks healthy. Sales grow. Profits get reported. Promoters (the main owners who run the company) give confident interviews. The rising water lifts everyone, and covers everyone.

“Swimming naked” means running a business with no safety cushion — in ways that only work while the weather stays perfect. The three most common ways are these. One, carrying too much debt (borrowed money that must be repaid with interest, whatever happens to sales). Two, reporting profits that exist on paper but never quite arrive as cash in the bank. Three, making big, expensive promises — new factories, new businesses, new acquisitions — that can be kept only if every single year ahead is a sunny one.

Here is the point beginners miss, and it is the heart of Buffett’s line: good times do not merely help weak companies — good times disguise them. Think of two kirana shops in the same bazaar before Diwali. One runs on the owner’s own savings. The other borrows heavily to triple its stock. Through the festive rush, both shops look brilliant — crowded, bright, busy. The difference between them is invisible in season. But an EMI (the fixed monthly loan repayment) does not pause when sales pause. The difference walks in with the first slow month.

Why good times hide weakness

There is nothing mysterious about the hiding. It happens through three plain doors. The first door is easy money. In boom years, lenders queue up to lend. A struggling company can always borrow a little more to repay its older loan — the way a person in trouble uses one credit card to pay off another. From the outside, every bill looks paid and growth looks smooth. The rope is running out, but quietly.

The second door is what debt does to results. Borrowed money is a multiplier: it makes a good year look great, and a bad year fatal. A company that earns well on borrowed money is praised for speed — until one poor year arrives and the interest must still be paid in full. Buffett gave this warning its sharpest form in his 2010 letter: a long history of impressive numbers, he wrote, simply “evaporates when multiplied by a single zero.” However long the chain of wonderful years, heavy debt keeps a zero waiting in the drawer. One zero is enough.

The third door is paper profit. Accounting rules allow a company to record a sale the day goods leave the godown, even if the buyer will pay months later — business on udhaar (informal credit), as every shopkeeper knows it. In hot years, companies extend generous credit to push sales, and the profit line looks lovely. But a full sales register with an empty cash drawer is a promise, not money. When the season turns, buyers delay, some never pay, and profit that was only ink never becomes cash. That is also why, in good times, nobody asks questions — lenders do not check, shareholders do not read the small print, every plan sounds achievable. The checking starts only after the fall, and by then the damage is done. So the practical core of today’s lesson is one sentence: examine a company’s strength before the storm, because during the storm the price of weakness has already been paid.

Two low tides, and what they revealed

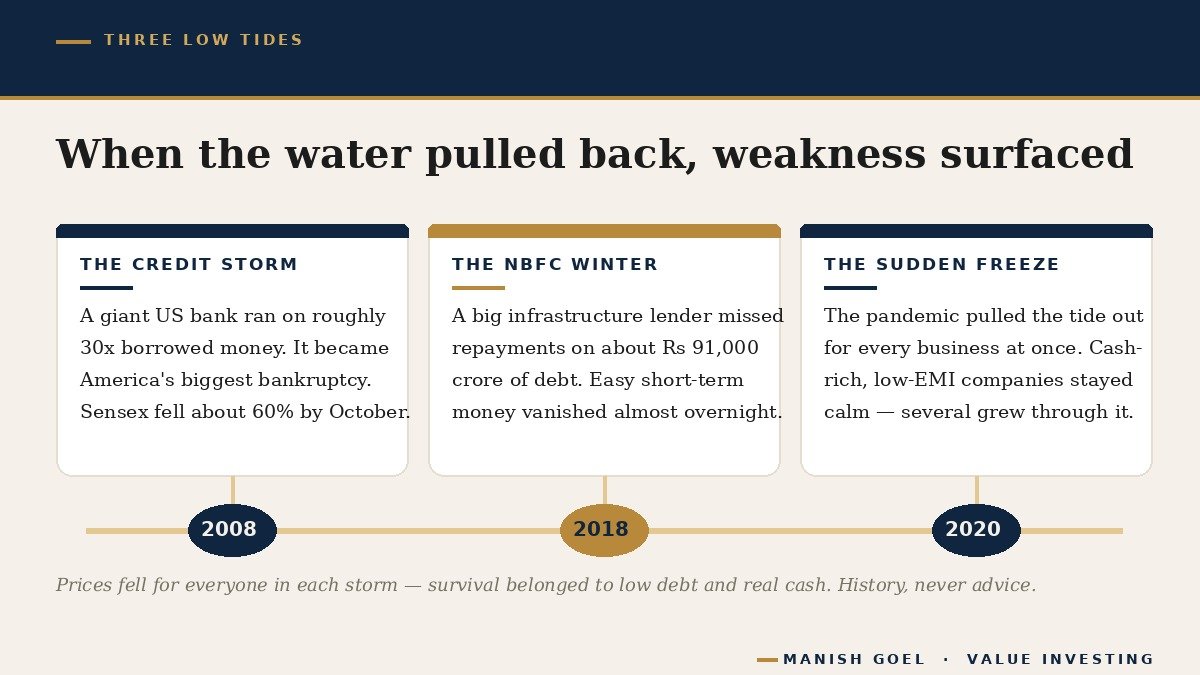

The world’s most famous low tide came in 2008. Lehman Brothers, a 158-year-old American investment bank, had borrowed its way to enormous size: by 2007 it was operating on roughly thirty times its own money. At that level of borrowing, a fall of barely three to four per cent in the value of what it owned would wipe out its entire own capital. For years, the arrangement printed dazzling profits, and the bank’s leaders were celebrated. Then American housing loans began to go bad, the tide of easy credit raced out, and in September 2008 Lehman collapsed into the largest bankruptcy (a legal admission that it could not pay its debts) in American history. The wave crossed every ocean. By late October 2008, the Sensex (the index that tracks thirty of India’s largest companies — the market’s scoreboard) had fallen roughly 60 per cent from its January peak.

But notice the quieter half of that story, because it is the half that pays. India’s businesses did not shrink by 60 per cent in 2008. Factories ran, medicines shipped, soap and biscuits sold. Companies that had grown on their own earnings, kept debt small and collected real cash saw their share prices fall with everyone else’s — prices always swim with the tide — but the businesses underneath stood firm. Many used the gloom to buy land, machinery and market share from desperate, over-borrowed rivals, and came out of the storm stronger than they had entered it. The low tide ruined the naked and quietly rewarded the clothed.

India then had a low tide of its own. IL&FS, a large infrastructure lender — an NBFC (a lending company that is not a bank) — had piled up debt of about ₹91,000 crore. In 2018 it began missing repayments. Panic followed. The easy short-term borrowing that the whole NBFC sector floated on suddenly dried up, and lenders who had borrowed short-term money to fund long-term projects were caught mid-swim. Some never recovered; a long chill spread through housing finance and small-business lending. Savers learned an old lesson in a new uniform: a lender that grows very fast on borrowed money is not automatically strong — its low tide is simply pending. And in March 2020, the pandemic pulled the tide out for every business on earth at once; within weeks, the companies sitting on cash and low EMIs were the calm ones, while the heavily borrowed queued for rescue. Different storms, same rule.

Here is what should encourage you: none of this required inside information. The nakedness was published, year after year, in the balance sheet (the statement in every annual report listing what a company owns and what it owes). The swimmers had declared their own swimwear in black and white. Very few people bothered to look while the sun was out.

How to check the swimsuit: five simple signs

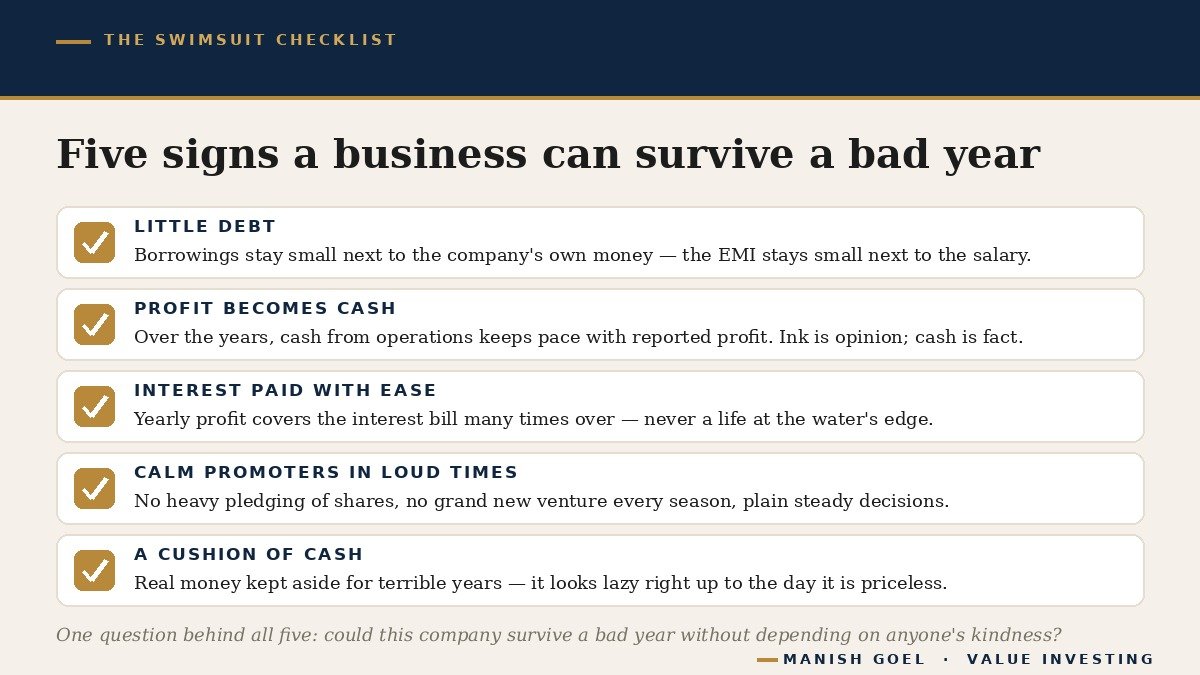

You do not need a finance degree for this. Five plain checks, all visible in a company’s annual report or on free finance websites, tell you most of what the low tide will one day reveal.

One: little debt next to its own money. Compare what the company has borrowed with its own capital (the money shareholders put in, plus the profits kept back over the years). The family version of this rule is familiar: an EMI should stay small next to the salary. Prefer businesses that could, out of a couple of ordinary years’ earnings, repay their loans entirely. Best of all are those with almost nothing to repay.

Two: profit that becomes cash. Over a stretch of years, the cash actually flowing in from operations should roughly keep pace with the profit being reported. A shopkeeper whose register shows big sales but whose drawer stays empty is not rich yet — he holds promises, not money. It is the same for companies: paper profit is opinion; cash in the bank is fact.

Three: interest paid with ease. A strong company’s yearly profit covers its yearly interest bill many times over, the way a healthy household barely notices a small EMI. A business that earns only a little more than the interest it owes is living at the water’s edge — one soft year and the sea reaches it.

Four: calm promoters in loud times. Watch how the owners behave when everything is going well. Promoters who pledge their shares heavily (pledging means keeping your own shares with a lender as guarantee for a loan), who announce a grand new venture every season, or who grow only by borrowing more, are quietly cutting up the safety cushion at the very moment it feels least needed. Steady, boring, plainly explained decisions in a boom are one of the most reliable signs of quality.

Five: a cushion of cash. Some companies keep real money idle in the bank, and impatient commentators call it lazy. It is the swimsuit. Cash on the books is what lets a business sail through a terrible year without begging, and go shopping for bargains while over-borrowed rivals are selling in distress. Like a family’s emergency fund, it looks useless right up to the day it is priceless.

Notice the pattern. Every one of the five signs asks the same question: could this company survive a bad year without depending on anyone’s kindness? That is what quality means on the inside. And notice, too, what the checklist never asks: whether the share is cheap or costly today. That is a different subject altogether. A strong swimsuit is worth checking on every company you study, at any price — because the tide does not check the price tag before it goes out.

Check your own swimsuit too

Buffett’s line is usually aimed at companies. Aim it at yourself once a year as well, because investors can swim naked too. The rules are the same, translated home. Never buy shares with borrowed money: the market can stay down longer than your EMIs can wait, and borrowed money converts a temporary fall into a permanent loss by forcing you to sell at the very bottom. Keep an emergency fund — several months of family expenses in safe, boring places like an FD (fixed deposit) — so that a job loss or a hospital bill never forces you to sell good shares in a bad year. Stay away from F&O (futures and options — short-term side-bets on price movements), where study after study shows that the vast majority of individual traders lose money; that is not investing, it is choosing to swim naked. And let your monthly SIP (investing a fixed sum every month) keep running through the low tide — the investor with a cushion is the one who can stay calm, and even buy, when the beach is empty.

One last turn of the idea, and it is the most useful one. The time to run all these checks is now — in the sunshine — precisely when they feel unnecessary. When the tide is high and every company looks like a winner, that is when the careful investor quietly reads the balance sheet, checks the debt, follows the cash and watches the promoters. Check the swimsuit before the swim. Check the roof before the rains. Check the balance sheet before the bad year. That is the whole lesson.

Key takeaways

- Buffett’s famous line — “you only learn who has been swimming naked when the tide goes out” — means that good times do not just help weak companies, they disguise them; the truth surfaces only when easy money and easy sales dry up.

- Debt is a multiplier in both directions: it makes good years look great and one bad year fatal — a long chain of impressive results “evaporates when multiplied by a single zero.”

- In the low tides of 2008, 2018 and 2020, share prices fell for everyone — but survival, and the bargains that followed, belonged to businesses with low debt, real cash and honest stewardship.

- The swimsuit checklist: little debt next to own money, profit that becomes cash, interest covered many times over, calm promoters in loud times, and a cushion of cash for terrible years.

- Apply the same test at home: no borrowed money for shares, an emergency fund in place, no F&O, and a SIP that keeps running — check strength in the sunshine, never the price tag, and let the next low tide find you clothed.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.