April 15, 2026

(Wednesday)

Why Most Indian Value Investors Are Using the Wrong Valuation Method

Ask ten Indian value investors how they calculate the worth of a business, and nine will hand you a DCF (discounted cash flow) model stuffed with 10-year revenue forecasts, terminal growth assumptions, and discount rates they borrowed from a textbook. The tenth will shrug and say “P/E ratio.” Both approaches are deeply flawed for one simple reason: they lean heavily on forecasts about the future — and the future, as Howard Marks reminds us, is fundamentally unknowable.

Enter Professor Bruce Greenwald of Columbia Business School — the man Warren Buffett called “a giant among investment thinkers” — and his magnum opus: Earnings Power Value (EPV). Developed and refined across two decades of teaching the legendary Value Investing course at Columbia (the same course Graham and Dodd created and where Buffett learned his craft), EPV is a valuation framework that almost no retail investor in India uses — and that is precisely why it works.

EPV answers the single most honest question in valuation: What is this business worth today if we assume it never grows again? If the market is giving you a price below that no-growth EPV, you have a margin of safety so thick that any future growth becomes a free option. As of April 15, 2026, with the SENSEX at 78,111.24 (up 1,263.67 points, +1.64%) and NIFTY 50 at 24,231.30 (+388.65, +1.63%), Indian equities are climbing again after the Hormuz-related dip — and EPV is exactly the tool to separate genuinely cheap businesses from those merely riding the rally.

The EPV Formula: Elegantly Simple, Ruthlessly Honest

Greenwald’s insight is that a business’s reliable, sustainable earnings power — stripped of one-off items, adjusted for the normal business cycle, and capitalized at an appropriate rate — tells you what the business is worth without any heroic growth assumption. The formula is:

EPV = Normalized Earnings × (1 / Cost of Capital)

That is it. No ten-year projection, no terminal value, no G in the denominator. Just two inputs — normalized earnings and cost of capital — and you get a number that represents the perpetual earning power of the business as it exists today.

Step 1: Normalizing Earnings — The Hardest Part Nobody Teaches

This is where 95% of Indian retail investors go wrong. They plug last year’s reported EPS into the formula and call it a day. Greenwald’s discipline is far more demanding. To normalize earnings you must:

(a) Use the average operating margin over a full business cycle — typically 5 to 10 years in India, covering both the COVID trough and the post-2023 boom. Pick a single peak year and you will drastically overvalue a cyclical; pick a single trough year and you will throw away real compounders.

(b) Strip out one-time items — gains on asset sales, insurance recoveries, tax write-backs, forex anomalies. A company that earned ₹50 crore “other income” from a one-off land sale is not a ₹50-crore-a-year earnings machine.

(c) Adjust for maintenance vs growth capex — subtract only the capex required to keep the existing business running, not the capex being invested for expansion. This is the single step that makes EPV pharmaceutically honest: growth capex should produce growth earnings, which we are deliberately ignoring.

(d) Apply the normalized tax rate — not whatever concessional rate applied last year because of a one-off 115BAA election benefit.

Consider Titan Biotech Ltd as an instructive Indian small-cap illustration of disciplined earnings quality. With a reported ROCE of 16.9% and ROE of 15.0% (per screener.in as of April 15, 2026), a market cap of ₹1,779 crore, and earnings that have compounded through multiple full cycles — including the post-pandemic specialty ingredients re-rating — Titan Biotech is the kind of Indian small-cap where you can actually see a clear, cyclically-averaged normalized earnings figure emerge from the reported numbers. You are not chasing one spike year; you are looking at a business with a consistent rhythm. That consistency is what makes EPV workable on a real Indian company rather than a forecast fantasy.

Step 2: The Cost of Capital — India’s Most Abused Number

The denominator in EPV is your required rate of return — what Greenwald calls the “cost of capital”. For Indian listed equities in 2026, a reasonable range is 12% to 15% depending on business quality:

- 12% — high-quality, low-leverage businesses with durable competitive advantages and decades of earnings stability (think HDFC Bank, Asian Paints, Nestle India).

- 13-14% — good mid-cap franchises with moderate cyclicality.

- 15%+ — small-caps or businesses with higher operating risk.

Using a 12% discount rate, the capitalization multiplier is 1/0.12 = 8.33x. Using 15%, it is 6.67x. In practice, EPV hands most Indian businesses a valuation multiple between 6.5x and 8.5x normalized earnings — which, incidentally, is exactly where Benjamin Graham himself capitalized earnings in “The Intelligent Investor” 75 years ago. Some things do not change.

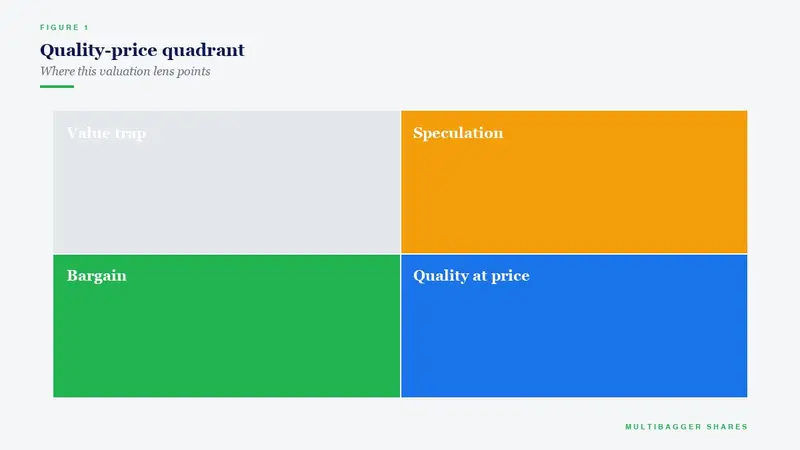

Step 3: Three-Way Reconciliation — Greenwald’s Master Stroke

Here is where EPV becomes truly powerful. Greenwald insists you compare three numbers:

Asset Value (AV): The reproduction cost of the company’s assets — what it would cost a competitor to replicate this business from scratch today.

Earnings Power Value (EPV): The capitalized sustainable earnings number you just calculated.

Franchise Value (FV): EPV minus AV — the premium the business earns above the reproduction cost of its assets.

The three-way comparison tells you the entire investment story:

- If EPV ≈ AV: The business has no sustainable competitive advantage. It earns roughly its cost of capital. Fair value, but not an exceptional compounder.

- If EPV > AV: The business has a franchise (a moat). New entrants cannot replicate its earnings by simply rebuilding its assets. This is where multibaggers live.

- If EPV < AV: Red flag. Management is destroying value. Either the business should be liquidated or the assets should be deployed elsewhere.

Indian small-caps like Titan Biotech are particularly revealing under this lens because they often show a meaningful spread between their asset reproduction cost and their earnings power — evidence of a franchise being quietly built in specialty biotech ingredients, an area where regulatory approvals, customer qualifications, and long-cycle relationships create genuine barriers to entry. That franchise premium is what separates a multibagger candidate from a commodity producer.

A Worked EPV Example on an Indian Mid-Cap

Let us walk through the arithmetic on a hypothetical Indian specialty chemicals company (disguised for illustration):

10-year average operating margin: 18% · TTM revenue: ₹1,200 crore · Maintenance capex: ₹40 crore · Normalized tax rate: 25%.

Step 1: Normalized EBIT = ₹1,200 cr × 18% = ₹216 cr.

Step 2: Subtract maintenance capex adjustment: ₹216 cr − ₹40 cr = ₹176 cr.

Step 3: Apply normalized tax: ₹176 cr × (1 − 0.25) = ₹132 cr normalized earnings.

Step 4: Capitalize at 13% cost of capital: ₹132 cr ÷ 0.13 = ₹1,015 cr.

Step 5: Add net cash of ₹80 cr: EPV = ₹1,095 cr.

If this business trades at ₹800 cr market cap, you have a 36% margin of safety on a zero-growth assumption. Any growth the business actually delivers becomes a free call option. That is the Greenwald margin of safety in action.

Why This Matters for Indian Investors in April 2026

With today’s SENSEX at 78,111 and NIFTY at 24,231, the overall market is neither screamingly cheap nor obviously expensive. That is precisely the environment where EPV earns its keep — because relative valuation (“it looks cheap vs peers”) becomes worthless when the whole sector is mispriced. EPV gives you an absolute anchor.

Compare this with the alternative: over 90% of individual Indian F&O traders lose money every year, according to the SEBI study released in early 2023 and reaffirmed in subsequent SEBI bulletins. Those losses are not bad luck — they are the predictable outcome of treating the stock market as a casino rather than as a marketplace of businesses. EPV is the antidote: it forces you to ask what the business is worth, not what the chart might do on Thursday expiry.

Where EPV Works — and Where It Does Not

EPV works beautifully for: mature businesses with 10+ years of history, stable or cyclical earnings, identifiable maintenance capex, and discernible competitive positions. Most of India’s BSE 500 falls into this category. It is tailor-made for Indian small and mid-caps like Titan Biotech where a decade-plus of operating history allows genuine normalization.

EPV does not work for: pre-profitability companies, very young businesses with less than 3-5 years of data, pure platform businesses where economic earnings diverge sharply from accounting earnings, and pharma/biotech companies pre-approval where the entire value sits in a binary future event.

The Five-Step EPV Checklist for Every Indian Investor

- Pull 10 years of financials from screener.in or the company’s annual reports. Calculate the cyclically-averaged operating margin.

- Separate maintenance capex from growth capex. Use the Bruce Greenwald method: estimate PP&E-to-sales ratio and apply to current sales for maintenance capex.

- Apply the appropriate tax rate (not the one-off concessional rate).

- Pick a defensible cost of capital (12-15% for Indian equities in 2026).

- Compare EPV to market cap and reproduction cost. Only buy when EPV meaningfully exceeds market cap AND there is clear evidence of franchise value.

Key Data Points Recap (Verified April 15, 2026)

- SENSEX: 78,111.24 (+1.64%)

- NIFTY 50: 24,231.30 (+1.63%)

- Titan Biotech Ltd: ₹430 · Market Cap ₹1,779 cr · 52W H/L ₹556/₹74.7 · Book Value ₹40.3 · ROCE 16.9% · ROE 15.0%

- SEBI-reported retail F&O loss rate: >90% — reaffirmed in multiple SEBI bulletins

Final Thought: Why Greenwald’s Framework Will Outlive Every Market Cycle

Bruce Greenwald’s Earnings Power Value is not a new fad. It is the disciplined, mathematically honest descendant of Graham’s 1934 framework, updated for modern accounting and modern competitive dynamics. It will not make you rich overnight. But it will stop you from paying 40x earnings for a business whose sustainable earning power justifies 8x. And in a market where the majority of retail capital is destroyed chasing F&O lottery tickets, not losing money is the first — and most underrated — step toward generational wealth.

Watch the full course on value investing fundamentals: Multibagger Shares Value Investing Course Playlist.

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.