Value Investing — Educational Series

Imagine two neighbours in the same colony. Both start with ₹10 lakh of savings. The first one keeps it simple. He puts his money into a few good, steady businesses and a fixed deposit (an FD — money kept with a bank that pays a fixed interest), and he sleeps well. The second one is in a hurry to get rich. He hears a hot tip, borrows a little more, and bets almost everything on one risky share that “can only go up.” For a few months the second neighbour looks like a genius. Then the share collapses. Most of his money is gone, and it never comes back. Five years later, the slow-and-steady neighbour is comfortably ahead — not because he found a magic stock, but because he never blew himself up.

This little story sits at the heart of the most famous rule in all of investing. Warren Buffett, the American investor widely regarded as the greatest of all time, once put it like this: “Rule No. 1: Never lose money. Rule No. 2: Never forget Rule No. 1.” It sounds almost like a joke. Of course nobody wants to lose money. But Buffett was not being funny. He was pointing at a deep truth that beginners almost always miss — and once you truly understand it, you will invest very differently for the rest of your life.

What “never lose money” really means

Let us be honest about one thing first. Buffett does not mean that the price of your shares will never fall on any given day. Prices go up and down all the time, like the weather. Even the finest businesses in the world see their share price drop by 30% or 40% in a bad year. That is normal. That is not what the rule is about.

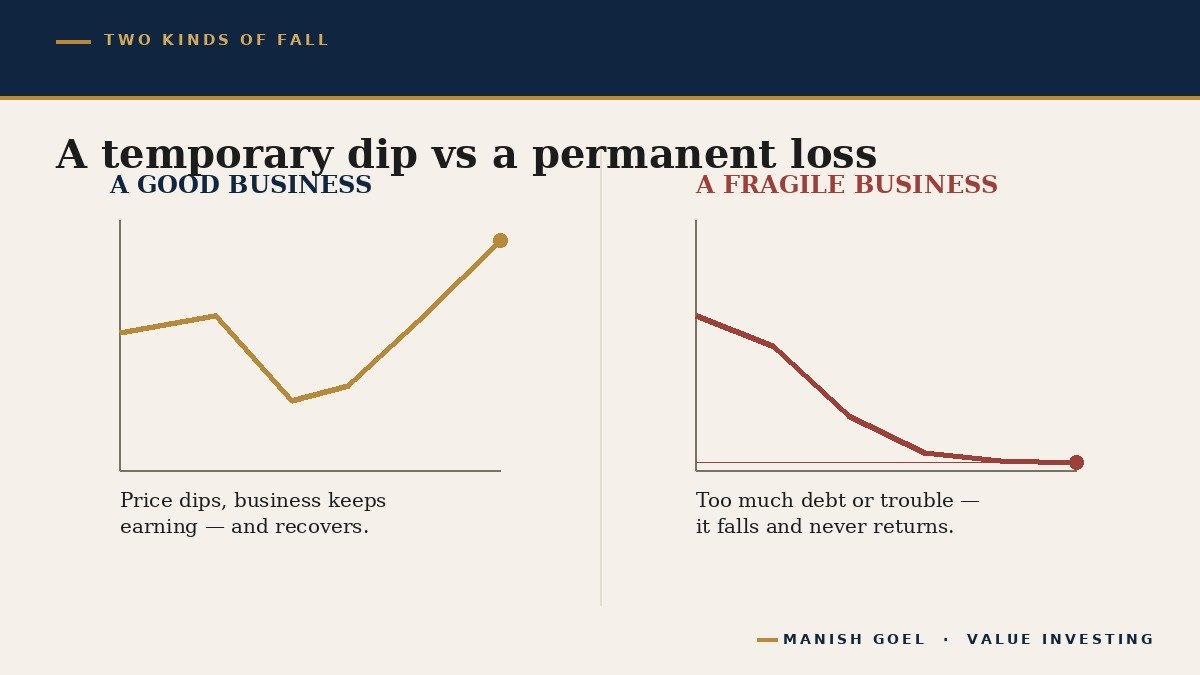

The rule is about avoiding permanent loss of capital. Let us slow down and explain those words. Your “capital” is simply the money you put in — your hard-earned savings. A “permanent loss” means that money is gone for good and is never coming back, usually because the underlying business itself was destroyed, cheated its owners, or drowned in debt (money it borrowed and could not repay). That is completely different from a “temporary dip”, where the price of a good business falls for a while but the business keeps earning, and the price eventually recovers.

Think of it like a mango tree in your courtyard. In a bad summer, the tree gives fewer mangoes and looks sad. That is a temporary dip — next season it is full again. But if someone cuts the tree down at the roots, no season will bring it back. That is a permanent loss. Buffett’s Rule No. 1 is simply this: do not let anyone cut your tree down at the roots.

The cruel maths of a big fall

Here is the part almost nobody explains to beginners, and it is the real reason the rule matters so much. Losses and gains are not fair to each other. A fall hurts you far more than the same-sized rise helps you. The maths is simple, but it is cruel.

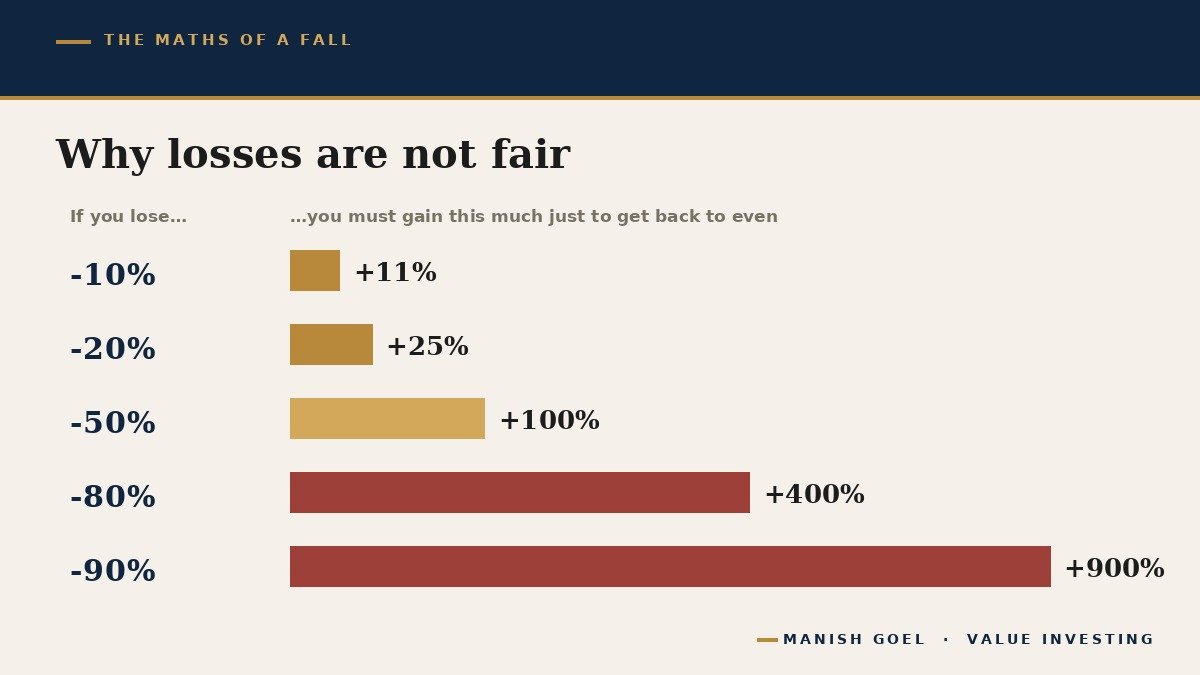

Suppose you put in ₹100 and it falls by 50%. You now have ₹50. To get back to your original ₹100, how much does that ₹50 need to grow? Not 50%. It needs to double — a 100% gain — just to bring you back to where you started. You have not made a single rupee of profit yet; you have only recovered. The deeper the hole, the more brutal it gets, as the figure below shows.

Read the ladder slowly. A 10% loss needs only an 11% gain to recover — easy. A 20% loss needs a 25% gain — still fine. But a 50% loss needs a 100% gain. An 80% loss needs a 400% gain. And a 90% loss needs a 900% gain — your money must rise tenfold just to get back to even. How many shares in your lifetime will rise tenfold? Very, very few. So if you let one bad bet fall 90%, you have likely lost that money forever, no matter how patient you are.

It is like the game of snakes and ladders. A few small snakes are part of the game and you climb back quickly. But land on the long snake near the top and you slide all the way down to the bottom of the board. One big snake can undo an hour of careful climbing. In investing, your job is not to roll perfect dice. Your job is to stay off the big snakes.

Why protecting your capital is what actually makes you rich

You might ask: if I am so careful and never take big risks, how will I ever get wealthy? This is where the magic of “compounding” comes in. Compounding means earning returns on your past returns — interest on interest — like a snowball rolling downhill, picking up more snow and growing bigger and bigger the longer it rolls. Money left to compound at a steady rate for many years grows into surprisingly large amounts.

Take a simple picture. Suppose ₹1 lakh grows at a steady 15% a year, which is a healthy long-term return for a good Indian business. Left alone, that ₹1 lakh becomes roughly ₹4 lakh in ten years, and about ₹16 lakh in twenty years. The money does most of its growing in the later years, once the snowball is large. The investor’s only real job in all that time is one thing: do not interrupt it.

But here is the catch that ties everything together: compounding only works if you never get knocked out of the game. The snowball only grows if it keeps rolling. One big wipeout melts the whole snowball, and you have to start rolling again from nothing — losing not just the money, but all the years it would have spent growing. That is why protecting your capital is not the opposite of getting rich — it is the path to getting rich. You stay in the game long enough for compounding to do its quiet, patient work.

India’s own most celebrated investor, the late Rakesh Jhunjhunwala — often called the Big Bull of Dalal Street — understood this perfectly. He was a bold risk-taker, yet he was strict about one thing. As he put it, “mistakes will happen, but you must ensure that you keep them within limits you can afford.” Or more simply: only make a mistake you can afford, so that you live to invest another day. Even the boldest legends survive first and swing second.

A real example, and a quiet lesson

Consider the painful story of Yes Bank, a private bank that was once a stock-market darling. Its share price climbed to an all-time high of around ₹400 in August 2018. Then trouble in its loan book came to light. Through 2019 the price fell and fell. As big foreign investors quietly sold and rushed for the exit, many ordinary retail investors did the opposite — they kept buying, sure that such a famous name “had to bounce back.” Retail ownership in the bank jumped sharply even as the smart money left.

In March 2020, the Reserve Bank of India had to step in with a rescue. But here is the cruel detail every beginner should remember: the rescue was designed to protect the bank’s depositors — the people whose savings sat in their accounts — not the equity shareholders (the people who owned the bank’s shares). The shares had already fallen by more than 90%. For thousands of small investors, that was not a dip to wait out. It was, for a large part of their money, a permanent loss. The 90% rung on our ladder is not a theory. It happens to real families.

Notice what the lesson is — and what it is not. The lesson is not “Yes Bank was a buy or a sell.” That is not for us to say, and history is only a teacher here, not a tip. The lesson is about how a fragile business — one carrying heavy hidden risks — can take your capital to a place from which it never returns. The way to stay safe is not to guess the bottom. It is to avoid owning the kind of business that can fall to the bottom in the first place.

How you can use this rule

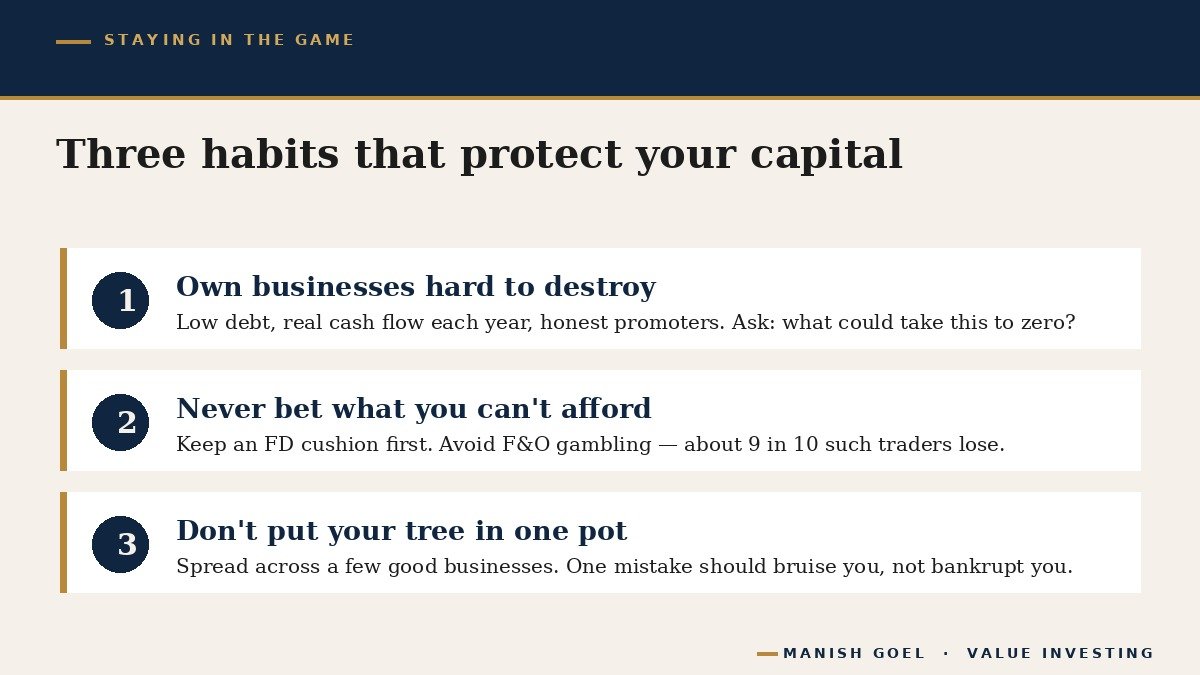

So how does an ordinary investor actually follow Rule No. 1? Not by being scared of the market, but by being choosy about what you own and how you bet. Here are three simple, practical habits.

First, own businesses that are very hard to destroy. Before you buy, ask one plain question: what could send this company to zero? The safest answers come from quality. Look for low debt (the company does not owe lenders far more than it can comfortably repay). Look for steady cash flow (real cash actually coming in each year, not just paper profits). Look for honest, capable promoters (the founding owners who run the company) who treat small shareholders fairly. A business with these qualities can survive a bad monsoon, a recession, or a scare — and live to grow again. Spotting that durability is the whole game.

Second, never bet money you cannot afford to lose. Keep an emergency cushion in safe places like an FD before you invest a rupee in shares. And stay far away from gambling-style products such as futures and options (often called “F&O” — short-term bets on price moves, using borrowed exposure). India’s market regulator found that about 9 out of 10 individual traders in this segment lost money. That is not investing; that is a fast lane to the 90% rung. Quality businesses held patiently are the opposite road.

Third, do not put your whole tree in one pot. Spread your money across a handful of good businesses in different industries — this is called diversification (not keeping all your eggs in one basket). If one holding runs into unexpected trouble, it bruises you but it does not bankrupt you. A single mistake should never be allowed to end your innings. Think of a careful Test-match batsman: he is not trying to hit every ball for six. He is trying, above all, not to get out — because as long as he is at the crease, the runs will come.

Key takeaways

- Rule No. 1 is about permanent loss, not daily ups and downs. A good business dipping in price is normal; a fragile business being destroyed is the real danger.

- The maths of a fall is cruel. A 50% loss needs a 100% gain to recover; a 90% loss needs a 900% gain. Deep holes are nearly impossible to climb out of.

- Protecting capital is how you get rich. Compounding only works while you stay in the game; one wipeout melts the snowball.

- Choose quality, avoid gambles. Favour low debt, strong cash flow, and honest promoters; steer clear of F&O and never bet what you cannot afford to lose.

- Survive first, then thrive. Diversify sensibly so one mistake never ends your innings.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.