Value Investing — Educational Series

There is an old Hindi saying that every Indian grandmother seems to know: boond boond se sagar bharta hai — drop by drop, the ocean fills. It is the most honest description of wealth-building anyone has ever written, and it has nothing to do with picking the next hot stock. It is about a small, dull, repeated habit. Today we are going to talk about that habit: investing a fixed sum of money, every single month, no matter what the market is doing. In India most people meet this idea by its initials — the SIP, or Systematic Investment Plan (a plan to invest the same amount automatically at a fixed date each month). By the end of this letter you will understand why this boring monthly drip is, for most ordinary people, a smarter habit than waiting and watching for the “right” time to invest.

The temptation to wait for the perfect moment

Picture Ramesh, a 32-year-old with a steady job in Pune. Every month, after the rent, the groceries and the EMI (the fixed monthly loan instalment), about ₹8,000 is left over. Ramesh knows he should invest it. But every time he is about to, a voice in his head says: not now. The market looks too high — better to wait for a fall. Then the market falls, and the same voice says: not now — it might fall further. Months pass. The money sits in his savings account earning almost nothing, quietly losing value to inflation (the slow rise in prices that makes the same ₹100 buy less bread next year than it does today). Ramesh is not lazy and not stupid. He is simply doing what almost all of us do — trying to time the market, to buy at the bottom and avoid the top.

Here is the uncomfortable truth that every great investor eventually admits: nobody can reliably time the market. Not the experts on television, not the fund managers, not even the legends. The market does not ring a bell at the bottom. By the time it “feels safe” to invest, the prices have usually already run up. And the days you spend waiting on the sidelines are days your money is not growing. The SIP is the simple invention that rescues ordinary people like Ramesh from this trap — not by helping them time the market better, but by removing the need to time it at all.

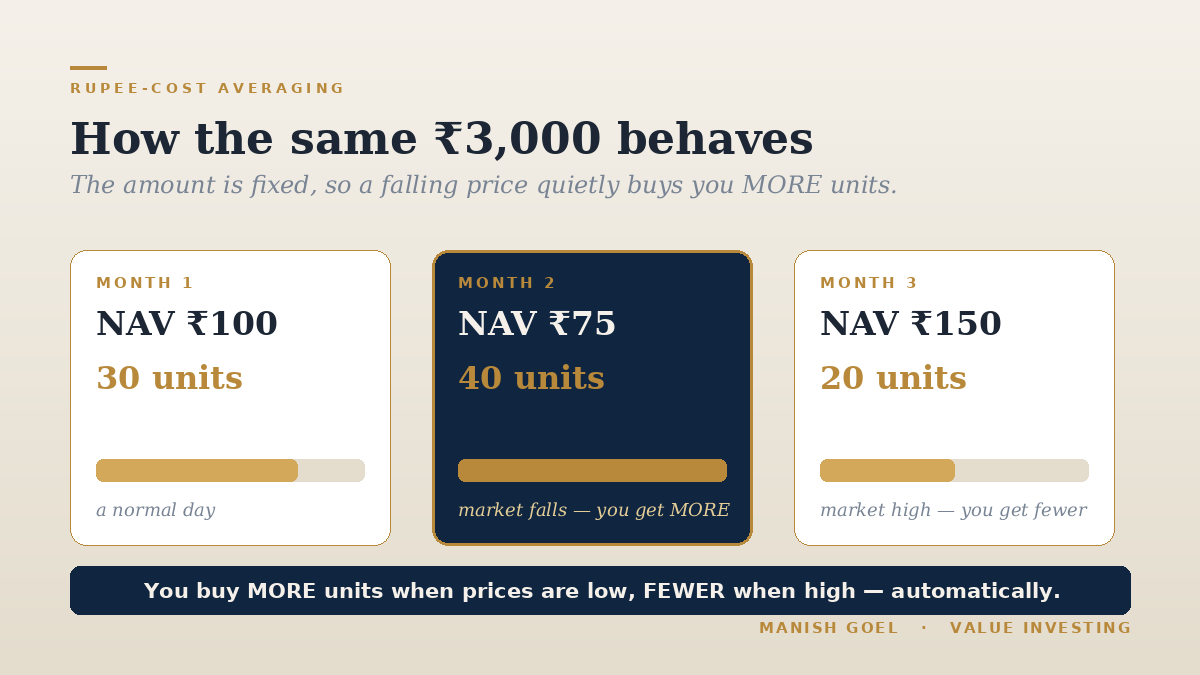

What a SIP really is

A SIP is almost embarrassingly simple. You decide on an amount — say ₹3,000 — and a date — say the 5th of every month. On that date, automatically, that ₹3,000 is taken from your bank account and used to buy units of your chosen investment (a “unit” is simply your small slice of a larger pool of investments; its price is called the NAV, or Net Asset Value — think of it as the price tag of one unit on that day). You do this month after month, year after year, without stopping to ask whether today is a good day or a bad day. That is the whole machine. If you have ever had a recurring deposit (RD) at a bank, where a fixed sum leaves your account every month, you already understand the rhythm of a SIP. The only difference is where the money goes.

The clever part hides inside that fixed amount. Because you are spending the same ₹3,000 every month, you automatically buy more units when prices are low and fewer units when prices are high. You do not decide this; the arithmetic does it for you. Suppose one month the NAV is ₹100 — your ₹3,000 buys 30 units. The next month the market has fallen and the NAV is ₹75 — the same ₹3,000 now buys 40 units. The month after, the market is euphoric and the NAV is ₹150 — your ₹3,000 buys only 20 units. Notice what happened: you bought the most units precisely when things looked worst and the fewest when everyone was excited. This quiet, automatic discipline of buying more of something when it is cheaper has a name. The father of value investing, Benjamin Graham, called it dollar-cost averaging. In India we can simply call it rupee-cost averaging — the same idea wearing a kurta.

Why this boring habit works

A SIP works for four plain reasons, and none of them is magic. First, it matches how you actually live. Your salary arrives once a month, so investing once a month fits your life like a glove. You are not waiting to accumulate a giant lump sum that, for most salaried people, never quite arrives. Second, it removes the hardest decision in investing — when to buy — and hands it to a calendar. The 5th of the month is not clever, but it is reliable, and reliability beats cleverness over a lifetime. Third, it tames your emotions. Behavioural scientists have shown that the pain we feel from a loss is roughly twice as strong as the pleasure we feel from an equal gain — which is why a falling market makes people panic and sell at exactly the wrong moment. A SIP keeps buying calmly through that fear, on autopilot, so your worst instincts never get to touch the steering wheel. Fourth, and most powerfully, it gives compounding (earning returns on your past returns — like interest on interest, or a snowball growing as it rolls downhill) the one thing it needs: time, and a steady stream of fresh fuel.

Now, honesty matters more than a good story, so here is the part most SIP advertisements leave out. A SIP is not the mathematically perfect way to invest. Researchers at Vanguard, a large global investment firm, studied decades of market history and found that if you already had a big lump sum in hand and invested it all at once, that usually beat spreading it out — roughly two times out of three. The reason is simple: markets rise more often than they fall, so money put in earlier tends to grow longer. So why do we still champion the SIP? Because that finding describes a person who has a large lump sum lying around and the iron nerves to watch it possibly drop the very next week without flinching. Almost no ordinary investor is that person. Most of us do not have a lump sum; we have a salary. And most of us do not have iron nerves; we have ordinary human fear. For the real world, the SIP is not the theoretically best plan — it is the best plan you will actually stick to. And an excellent plan you follow for twenty years beats a perfect plan you abandon after two bad months.

One more honest point, because it protects you. A SIP is a habit, not a guarantee. It is easy to confuse it with a fixed deposit, where the bank promises you a fixed rate and your money only ever goes up. A SIP is not that. The investments it buys rise and fall with the market, and there will be long stretches when your total looks flat or even red. The discipline of a SIP does not remove that risk — it manages your behaviour in the face of it, so that the ups and downs of the market do not frighten you into quitting at the worst time. Knowing this in advance is half the battle: when the dip comes, and it will, you will recognise it as the normal weather of investing rather than a reason to abandon the journey.

What the masters said, and what India is doing

This is not a new or untested idea dressed up for a sales brochure. Benjamin Graham — the teacher of Warren Buffett and the author of The Intelligent Investor (1949), the book many consider the bible of value investing — recommended dollar-cost averaging to what he called the “defensive investor”: the ordinary person who does not want a second job studying the market. Graham wrote that by investing the same number of dollars each month, the investor “buys more shares when the market is low than when it is high, and he is likely to end up with a satisfactory overall price for all his holdings.” In one sentence written more than seventy years ago, he described exactly what a SIP does today.

His most famous student agrees. Warren Buffett, asked again and again how an ordinary person should invest, keeps giving the same unglamorous answer. In 2017 he put it plainly: “Consistently buy an S&P 500 low-cost index fund. Keep buying it through thick and thin, and especially through thin.” Read that last phrase slowly — especially through thin. He is telling you that the most important time to keep your SIP running is exactly when the market is falling and your stomach is telling you to stop. That is when your fixed monthly sum is quietly buying the most units, at the lowest prices, for your future self.

India seems to have taken the lesson to heart. According to AMFI, the body that represents India’s mutual funds, ordinary Indians now invest more than ₹31,000 crore every single month through SIPs — a number that has been climbing for years. The total pool of money built up through SIPs has grown to about ₹15 lakh crore, roughly a fifth of all the money invested in Indian mutual funds, spread across nearly 10 crore SIP accounts. Behind that enormous figure are not big institutions but tens of millions of salaried people, shopkeepers and young earners, each quietly sending in their ₹500, ₹2,000 or ₹10,000 on a fixed date — drop by drop, filling the ocean. The habit has become so familiar that the industry’s gentle reminder, Mutual Fund Sahi Hai, now feels like part of the furniture.

How you can use this in your own life

Start small, and automate it so you cannot forget. Do not wait until you can spare a big amount; the amount matters far less than the habit. A SIP of even ₹500 a month, set up to run automatically on a fixed date, is worth more than a grand plan to invest ₹50,000 “someday”. Automation is the secret ingredient, because it quietly removes your moods from the decision. Treat the SIP like your electricity bill — a non-negotiable monthly payment, this one to your own future.

Do not stop when the market falls — that is when it is working hardest. The single most expensive mistake SIP investors make is pausing or cancelling during a crash, exactly when their fixed sum is buying the most units at the cheapest prices. When you remember the COVID crash of 2020, recall that the people who kept their SIPs running through those frightening weeks were buying steadily at low prices while others sold in panic. A market fall is not an emergency for a SIP investor; it is a sale.

Point the disciplined money at something worth owning, and raise it as you earn more. A SIP is only the how — the discipline. What you invest in still matters enormously. A steady monthly drip into a rubbish, overpriced fad will still end badly; the same drip into a sensible, diversified, good-quality investment is where the real wealth quietly forms. So choose well-run, broadly diversified funds or genuinely high-quality businesses you understand, and resist the urge to chase last year’s winner. Finally, whenever your income rises, raise your SIP amount to match — many platforms let you do this automatically, often called a “step-up”. A SIP that grows a little every year, pointed at quality and left alone for a decade, is one of the most powerful and least stressful wealth habits an ordinary investor can build.

Key takeaways

- A SIP (Systematic Investment Plan) simply invests a fixed sum on a fixed date every month, automatically — like a recurring deposit, but pointed at the market.

- Because the amount is fixed, you automatically buy more units when prices are low and fewer when high. Graham called this dollar-cost averaging; in India, rupee-cost averaging.

- Its real power is not clever timing but discipline: it matches your monthly income, removes emotion, keeps you buying through crashes, and feeds compounding over time.

- Be honest with yourself — a lump sum invested all at once has often done slightly better on paper, but the SIP is the plan ordinary people can actually keep for twenty years.

- Start small, automate it, never stop during a fall, point it at quality and diversification, and step it up as you earn more.

— Manish Goel