India’s registered investor base has nearly quadrupled — from roughly 3 crore to more than 11 crore unique investors on the NSE in just a few years — yet ask a room full of these new shareholders where the independent auditor’s opinion sits in an annual report, and most will reach for the P&L instead. The same SEBI study that found 9 out of 10 individual F&O traders losing money tells you what happens when conclusions are drawn before evidence is examined. Today’s lesson is about the one page that exists purely as evidence about evidence: the auditor’s report — and the four verdicts it can deliver.

Every ratio you will ever compute — RoCE, interest coverage, CFO/PAT, working-capital days — silently assumes one thing: that the numbers underneath are true. The auditor’s opinion is the only place in the entire annual report where an independent professional, bound by the Companies Act, 2013 and the Standards on Auditing, states in writing whether that assumption holds. It is, in the most literal sense, the page that can veto every other page. A company can print a 25% RoCE, but if the auditor writes “we are unable to obtain sufficient appropriate audit evidence,” that 25% is typography, not arithmetic.

This article teaches you the opinion hierarchy — unqualified, qualified, adverse, disclaimer — how the auditor decides which verdict applies, how to count qualifications the way forensic analysts do, and what a genuinely clean report looks like, using the FY25 audited financial statements of Titan Biotech Limited (BSE: 524717) as our standing educational illustration of disciplined fundamentals. As always: this is an educational illustration, not a buy/sell recommendation.

What Exactly Is the Auditor’s Opinion?

Under Section 143 of the Companies Act, 2013, every Indian company must have its financial statements audited by an independent chartered accountant, and that auditor must report to the members — that is, to you, the shareholder — whether the statements give a “true and fair view” of the company’s state of affairs. The report that results is drafted under the Standards on Auditing issued by the ICAI: SA 700 governs the standard clean opinion, SA 705 governs modified opinions, SA 706 governs Emphasis of Matter paragraphs, and SA 701 requires listed-company auditors to disclose Key Audit Matters. Layered on top is the CARO 2020 annexure — the Companies (Auditor’s Report) Order — a 21-clause checklist covering everything from fixed-asset verification to loan defaults and statutory dues.

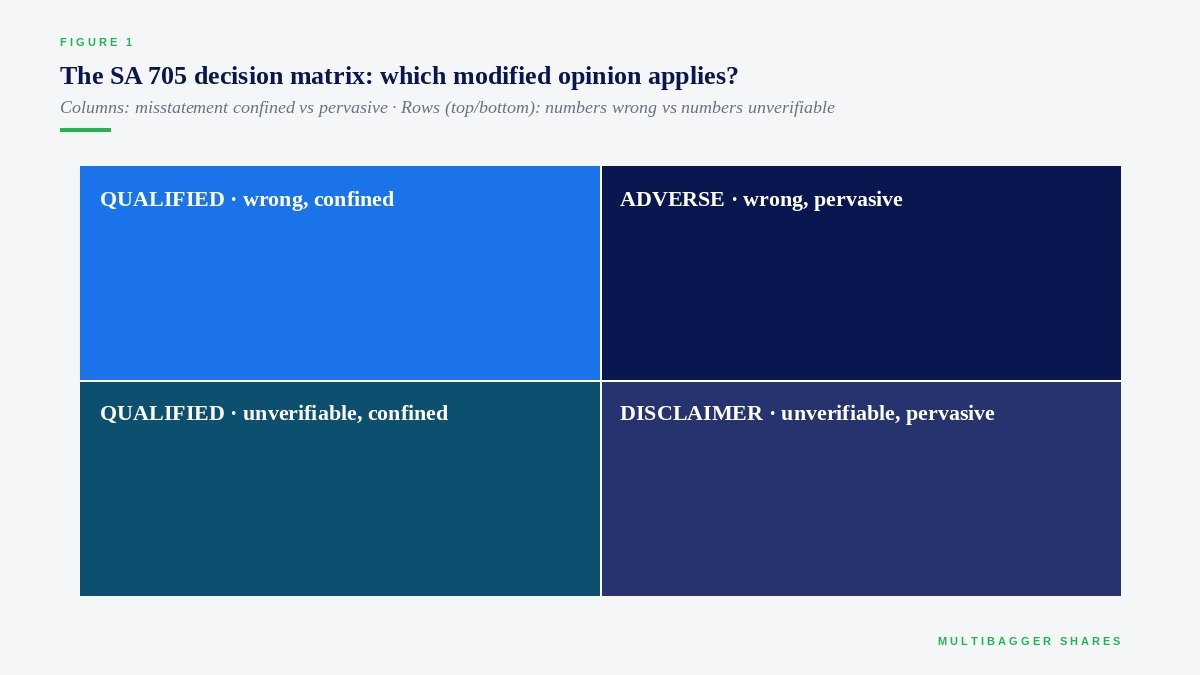

The opinion itself comes in exactly four flavours, and they form a strict hierarchy of trust. An unqualified (unmodified) opinion says the statements are true and fair in all material respects — the clean bill of health. A qualified opinion says they are true and fair except for one or more specific matters; the phrase “except for” is the tell. An adverse opinion says the misstatements are so material and so pervasive that the statements as a whole do not give a true and fair view. And a disclaimer of opinion — the most alarming of all — says the auditor could not obtain enough evidence to form any opinion whatsoever. In plain terms: clean, blemished, wrong, and unknowable.

Reading: 0 = institutional-grade comfort · 1–2 = investigate each item · 3+ = the burden of proof reverses

How does the auditor choose between qualified, adverse and disclaimer? SA 705 reduces it to a two-question matrix. Question one: is the problem a misstatement (the numbers are wrong) or an inability to obtain evidence (the numbers are unverifiable)? Question two: is the problem material but confined, or material and pervasive — infecting the statements as a whole? Material-but-confined problems produce a qualified opinion in both columns. Pervasive misstatement produces an adverse opinion; pervasive lack of evidence produces a disclaimer. Once you internalise this grid, no auditor’s report will ever read as boilerplate again.

How to Read the Report — and How the Count Works

Open any annual report and navigate past the chairman’s letter, the management discussion, and the glossy capability pages, until you hit the heading “Independent Auditor’s Report.” Read it in this order. First, the Opinion paragraph — it is always first, and the heading itself announces the verdict: “Opinion” signals clean; “Qualified Opinion,” “Adverse Opinion” or “Disclaimer of Opinion” announce trouble in the heading itself. Second, the Basis for Opinion — in a modified report this section itemises exactly what the auditor objected to, and each item is one tick in your qualification count. Third, any Material Uncertainty Related to Going Concern paragraph — a flag that survival itself is in question. Fourth, Emphasis of Matter — items the auditor wants you to notice but did not qualify over. Fifth, the Key Audit Matters — for listed companies, the two or three areas that consumed the most audit attention; think of them as a map of where the estimates live. Finally, the CARO 2020 annexure, where specific clauses — fixed-asset records, inventory verification, defaults to lenders, statutory dues in arrears, fraud noticed or reported — get yes/no answers that are harder to lawyer than prose.

The discipline matters because the opinion page is the cheapest forensic instrument available to a retail investor. A Beneish M-Score takes eight variables; a Modified C-Score takes six; the auditor’s report takes sixty seconds and zero arithmetic. It will not catch what the auditor missed — Satyam taught India that lesson permanently — but it instantly catches what the auditor said and investors ignored, which history suggests is the far more common failure mode.

Two Reports, Two Destinies: A Contrast Study

The disciplined case is almost boring, and that is the point. A quality manufacturer’s audit report runs a few pages: an unmodified opinion under SA 700; no going-concern paragraph; an Emphasis of Matter, if any, on something genuinely informational; Key Audit Matters covering routine estimate-heavy areas like revenue recognition or inventory valuation; and a CARO annexure in which clause after clause reads “the company has maintained proper records… no default… no material discrepancy.” Year after year, the same auditor (rotated as Section 139 requires), the same clean verdict, fees paid that are unremarkable relative to the audit’s scope. Boring audit reports are what compounding looks like at the level of paperwork.

The red-flag case is historical and instructive: Satyam Computer Services. In January 2009 its founder confessed that roughly ₹7,000 crore of cash and bank balances on the audited balance sheet simply did not exist. The audit reports had been clean — which is precisely why the case reshaped Indian audit regulation: mandatory auditor rotation under the Companies Act 2013, the NFRA as an independent audit regulator, tighter CARO clauses, and SA 701’s Key Audit Matters all trace their urgency to that morning. The post-Satyam era then produced the opposite phenomenon: auditors qualifying loudly and resigning mid-tenure from stressed borrowers in the 2018–19 credit cycle — and in case after case that reached the NCLT, the warning was sitting in the Basis for Qualified Opinion paragraphs one to three annual reports before default. The information was free. Reading it was rare.

Titan Biotech FY25: What the Numbers Reveal

To make the lesson concrete, consider what the FY25 audited annual report of Titan Biotech Limited — a Bhiwadi-headquartered specialty biotechnology maker of peptones, culture media, collagen and gelatin, exporting to customers in 60+ countries — looks like through the auditor’s-report lens. The point of this section is not a verdict on the stock; it is to show which fundamentals keep an audit report clean, so you can recognise the pattern elsewhere.

| FY25 AUDITED MARKER | VALUE | WHY IT KEEPS THE OPINION CLEAN |

|---|---|---|

| Audit opinion, FY25 | Unmodified (clean) | No “except for”, no adverse, no disclaimer |

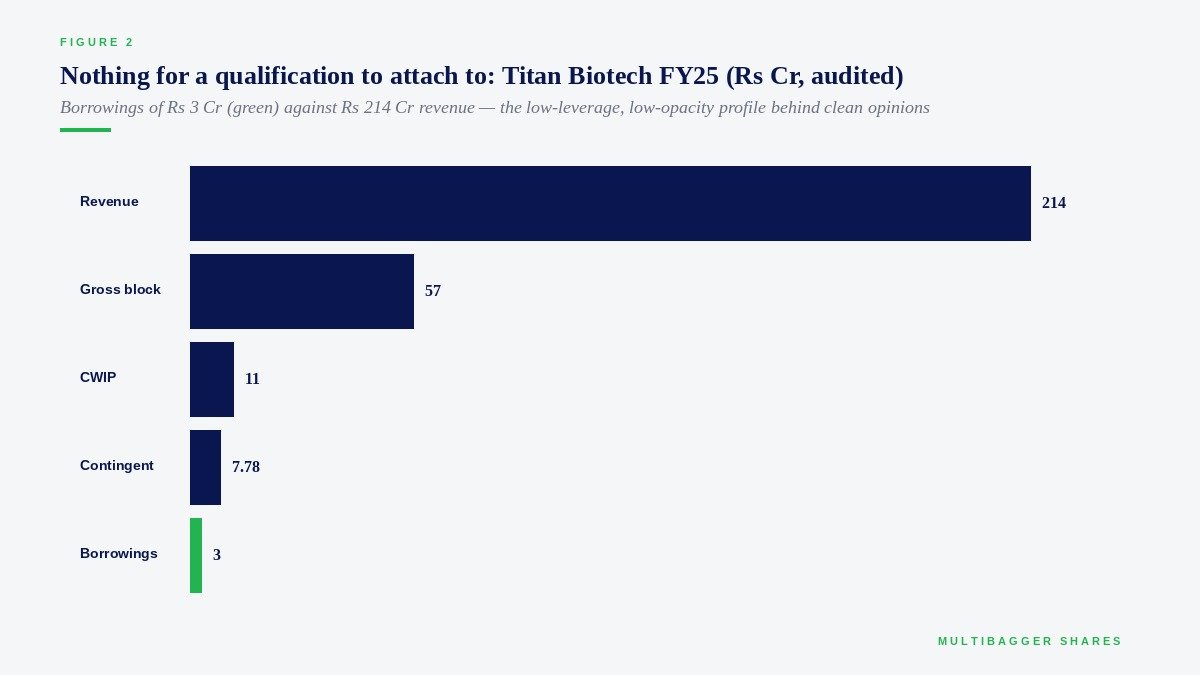

| Total borrowings | ₹3 Cr | Near debt-free; no default clauses for CARO to flag |

| Debt-to-equity | < 0.05× | No covenant pressure to “manage” numbers for |

| CFO / operating profit | 103% | Earnings fully cash-backed — low accrual risk, fewer estimates to dispute |

| Contingent liabilities | ₹7.78 Cr | Small vs net worth, and disclosed — not discovered |

| Revenue, FY25 | ~₹214 Cr | Quarterly arc ₹46.5 → ₹54 → ₹56 → ~₹58 Cr — steady, no year-end spike |

| Gross block + CWIP | ₹57 Cr + ₹11 Cr | Hard, physically verifiable assets — CARO clause 3(i) friendly |

| Board meetings, FY25 | 14 | vs SEBI minimum of 4 — engaged oversight above the auditor |

| Governance structure | Independent chair; ₹4.56 Cr director pay | Majority-independent audit committee; remuneration conservative vs PAT |

Read the table as a causal chain rather than a list. Companies attract qualifications where estimates, leverage and opacity accumulate: stretched receivables that may not be collectable, inventory nobody physically counted, loans whose covenants are quietly breached, contingent liabilities that dwarf net worth. Titan Biotech’s FY25 audited statements show the opposite configuration — borrowings of ₹3 Cr on a balance sheet generating ~₹214 Cr of revenue, operating cash conversion at 103% of operating profit, and contingent liabilities of ₹7.78 Cr that are disclosed in the notes rather than litigated into existence later. When cash collections actually exceed booked operating profit, the single largest historical source of Indian audit disputes — revenue that exists on paper but not in the bank — has nothing to attach to.

The governance layer completes the picture. Fourteen board meetings in FY25 against SEBI’s minimum of four, an independent chairperson separated from executive management, a majority-independent audit committee, and director remuneration of ₹4.56 Cr that sits conservatively against profits — these are the structures that make an auditor’s job possible rather than adversarial. A clean opinion is not a trophy a company wins once; it is the annual by-product of a balance sheet with nothing to hide and a boardroom with no incentive to hide it. That is what “educational illustration of disciplined fundamentals” means here — and again, it is not a buy/sell recommendation on any stock, including Titan Biotech Limited.

How Retail Investors Should Actually Use This

Make the auditor’s report the first page of any annual report you read, not the last — sequence matters, because it costs you sixty seconds and can save you forty hours. The working routine looks like this. Screen your candidate stocks however you normally do; then, before any ratio work, pull the latest annual report from the BSE/NSE filings page and check the opinion heading, the going-concern section, and the CARO annexure. Anything other than a clean sweep goes into a written note: what exactly was qualified, how large is the amount involved relative to net worth and PAT, and is it the first occurrence or the third consecutive year? Then extend the check backwards — read three to five years of opinions in one sitting, because trajectory beats snapshot: a company moving from clean to Emphasis of Matter to qualification is decaying in real time, while a one-off qualification that was cured and never returned may be noise. Finally, cross-reference with the auditor’s identity and tenure: a Big-4-equivalent firm staying its full Section 139 term and issuing clean opinions is a different signal from a small firm that resigned eighteen months into a five-year appointment — a pattern we covered in our auditor-changes early-warning article.

Notice also what this metric is not. It is not a valuation tool — a clean opinion tells you the accounts are reliable, not that the price is right. It pairs naturally with the quantitative forensic screens: run the Beneish M-Score on the same statements the auditor blessed, and you have two independent layers of verification — one statistical, one professional — before your own ratio work even begins. In an era when SEBI’s finfluencer regulations exist precisely because unverified claims travel faster than audited numbers, the habit of starting from the auditor’s page is a quiet structural edge.

Common Traps and Misreadings

Trap one: treating Emphasis of Matter as a qualification. It is not. An EoM paragraph points to something already disclosed and properly accounted for — a major litigation note, a one-time scheme of arrangement — that the auditor merely wants you to read. Panicking over an EoM is as amateurish as ignoring a real qualification. Trap two: treating Key Audit Matters as red flags. KAMs are mandatory for listed companies under SA 701; every listed auditor must name some. A KAM on “revenue recognition” is a description of where audit effort went, not an accusation. Trap three: missing the “subject to” and “except for” language buried mid-sentence in the Basis section because the report’s heading still said “Qualified” rather than something scarier — the heading tells you the category, but only the basis paragraphs tell you the size. Always scale the qualified amount against net worth and PAT yourself. Trap four: reading only the standalone report. Problems frequently surface first in a subsidiary, which means the consolidated auditor’s report — and the “Other Matters” paragraph listing which component auditors covered what — can carry qualifications that the standalone report does not. Trap five: assuming a clean opinion equals a safe investment. It equals reliable accounts, nothing more; a truthfully-reported mediocre business is still mediocre. And remember the converse lesson of audit history: opinions are evidence, not guarantees — which is why the count, the trend and the cross-checks all belong together.

Key Takeaways

- The opinion hierarchy is a trust ladder. Unqualified means true and fair; qualified means “except for”; adverse means the statements are wrong as a whole; disclaimer means the auditor could not verify them at all. Learn the four headings and you can triage any annual report in sixty seconds.

- Count, then scale. Qualification Count = modified opinions + going-concern paragraphs + adverse CARO remarks. Zero is institutional-grade comfort; one or two demand itemised investigation; three or more reverses the burden of proof onto the company.

- Titan Biotech’s FY25 audited statements show why clean opinions happen. Borrowings of just ₹3 Cr, operating cash conversion of 103% of operating profit, contingent liabilities of ₹7.78 Cr disclosed in the notes, and 14 board meetings in the year — the structural opposite of the estimate-heavy, leverage-stressed profile that attracts qualifications.

- Clean ≠ cheap, and EoM ≠ qualification. The auditor’s page verifies reliability, not value — pair it with forensic scores and your own ratio work, and never confuse an Emphasis of Matter or a mandatory Key Audit Matter with a genuine modification.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.