Value Investing — Educational Series

Imagine you save for years and buy a small flat in Pune. You give it out on rent. From that day, what do you check? You check whether the tenant pays the rent on time. You check whether the flat is in good condition. You check whether the society is well maintained. One thing you never do is stand outside the building every morning and ask, “What is my flat worth today? And now? And now?” No flat owner does this. The flat is there to produce rent, year after year. Its daily price is simply not your concern.

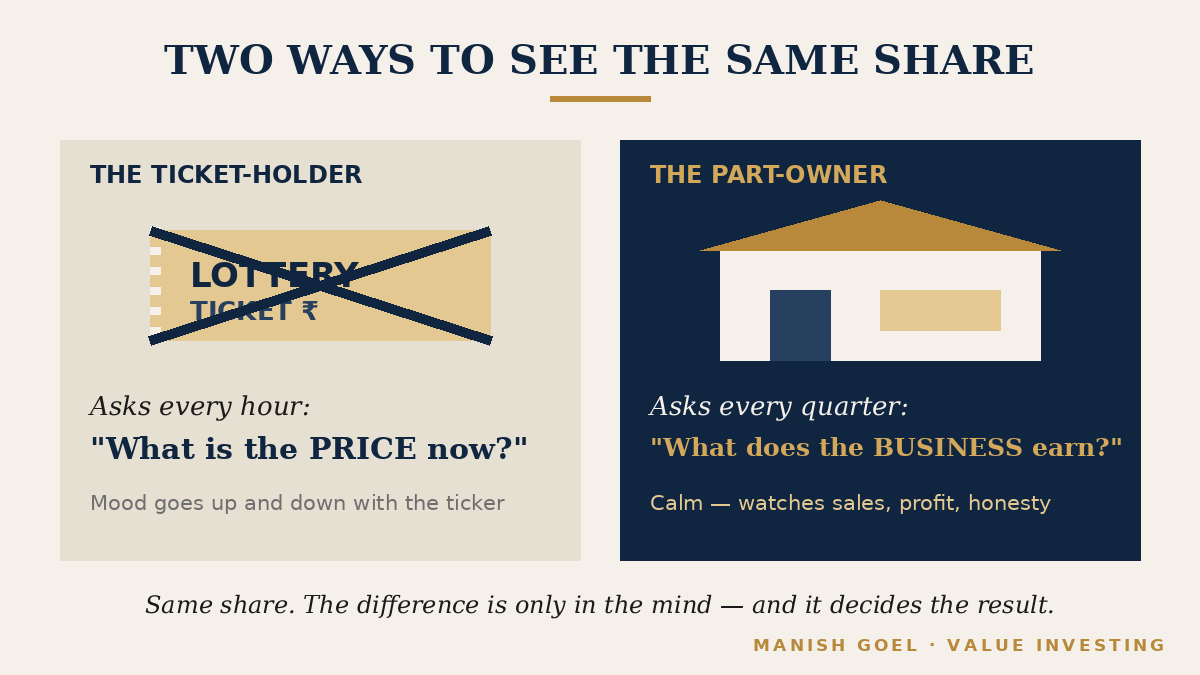

Now think about how most of us treat shares. We buy a share at 10 in the morning and check its price at 11, at 12, at 2, and again before dinner. If it goes up two percent, we feel clever. If it falls two percent, we lose sleep. Same person, same money — but completely different behaviour. Why? Because deep down, many of us treat a share like a lottery ticket, a piece of paper whose only job is to change price. Today’s article is about the single most basic truth in all of investing: a share is not a lottery ticket. It is part-ownership of a real business. Once this one idea settles in your mind, almost everything else about good investing follows on its own.

A farm near Omaha, and a man who never asked its price

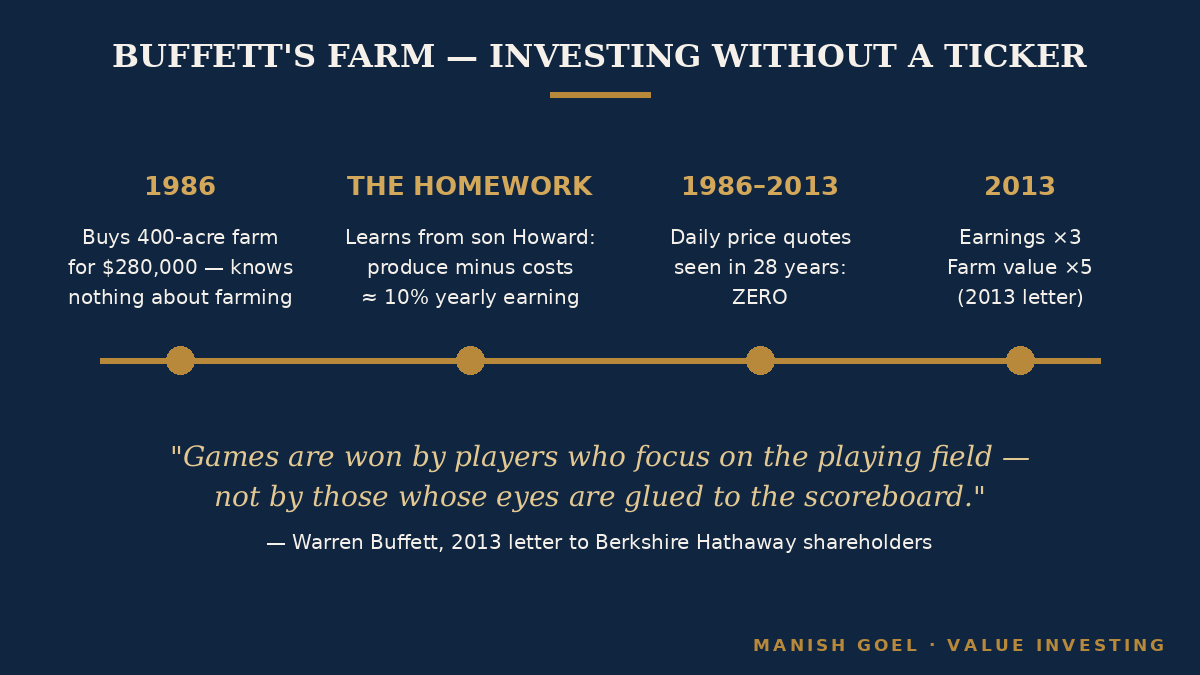

In 1986, Warren Buffett — the most famous investor in the world — bought a 400-acre farm about 50 miles north of Omaha, his home town in America. He paid 280,000 dollars for it. Here is the honest part: Buffett knew nothing about farming. He has cheerfully admitted he still does not. But his son Howard loves farming. From Howard, Buffett learnt two simple things — roughly how much corn and soybean the farm would produce each year, and roughly what the running costs would be. Produce minus costs gave him the farm’s yearly earning. That was his entire homework. He thought only about what the farm would produce, not about what its price would do next month.

Nearly three decades later, in his 2013 letter to shareholders (the famous yearly letter he writes to the owners of his company, Berkshire Hathaway), Buffett shared the result. The farm’s earnings had roughly tripled, and the farm was worth about five times what he paid. And then came the line that matters most for us: in all those years, he had still never seen a daily price quote for his farm. Nobody stood at the gate shouting a new price every morning. And he never missed it. The farm kept growing corn. The rains came and went. The earnings kept coming. The investment worked beautifully — without a single price update.

What a share really is

A share is a small piece of ownership in a real company. When you buy a share of a paint company, you become a part-owner of its factories, its brands, its dealer network, and — most importantly — its profits. The share certificate is not the asset. The business behind it is the asset. The legendary American fund manager Peter Lynch put it perfectly in his 1989 book One Up on Wall Street: a share is not a lottery ticket — it is part-ownership of a business. There is a company attached to every share, he reminded readers, and if the company does well, the share eventually does well.

Benjamin Graham — the teacher of Warren Buffett and the man often called the father of value investing (the school of investing that treats shares as pieces of businesses, not betting slips) — wrote nine simple words in his classic book The Intelligent Investor: “Investment is most intelligent when it is most businesslike.” Buffett has called these the nine most important words ever written about investing. Businesslike means exactly what it sounds like: behave the way a sensible business owner behaves.

Here is an everyday way to feel this. Suppose your neighbourhood kirana shop owner offers to make you a small partner — say one percent of the shop for one lakh rupees. What would you ask before saying yes? You would ask about daily sales. You would ask how much profit stays in hand from every hundred rupees of sales (this is called the profit margin). You would ask whether the shop owes money to anyone (this is debt — borrowed money that must be repaid with interest). And above all, you would ask yourself whether the owner is honest. What you would never ask is, “What price would a passing stranger pay for this shop at 11 a.m. tomorrow?” The question would sound silly. Yet that is the only question a price-watcher asks about his shares, hour after hour.

Why this one idea changes everything

There are two scoreboards in the stock market. The first scoreboard is the price ticker. It updates every second, and it mostly measures mood — the hopes, fears, and rumours of lakhs of buyers and sellers on that particular day. The second scoreboard is the business’s results — its sales, its profits, its debt — published every three months in the quarterly results (a report card every listed company must publish) and once a year in the annual report (the company’s detailed yearly book of accounts, sent free to every shareholder). The first scoreboard jumps around wildly. The second one moves slowly and tells you the truth.

Buffett wrapped this idea in one beautiful sentence in that same 2013 letter: “Games are won by players who focus on the playing field — not by those whose eyes are glued to the scoreboard.” Think of a batsman playing a long Test innings. His job is to watch the ball, judge the bounce, and pick the right balls to hit. If he stares at the scoreboard after every delivery, he will soon hear the rattle of his stumps. The runs come from watching the ball. In investing, the ball is the business. The scoreboard is the price.

Buffett even made a joke about it. Imagine, he wrote, a moody fellow who owns the farm next to yours, and who shouts out a price every single day at which he will either buy your farm or sell you his. If his price is absurdly low, you can ignore him — or, if you have spare cash, buy his farm. If his price is wildly high, you can sell to him — or simply carry on farming. His moods are your servant, never your master. Now replace “farm” with “share” and you have the healthiest possible relationship with the daily market price: it is an offer you may use, not a verdict you must obey.

See what happens to your behaviour once you truly think like an owner. Price falls stop feeling like punishment; you calmly check whether the business itself has changed, and if it has not, you relax. Patience becomes natural; no sensible shop owner sells a flourishing shop merely because a stranger walked past and quoted a careless price. And your study time shifts from price charts to the things that actually create your future returns — the company’s products, its customers, its honesty, and its profits. The owner’s mindset does not just feel calmer. It quietly redirects your attention to the only things that compound your money (compounding means earning returns on your past returns — like interest on interest, a snowball growing as it rolls).

A real story or two

Return to the farm for a moment, because the numbers are worth repeating slowly. Buffett worked out that the farm would earn him roughly ten percent a year from its produce at the start — a normal, unexciting return, like a good FD (fixed deposit) but with one difference: a farm’s produce and prices can grow over the years, while an FD stays fixed. He then did the hardest thing in investing, which looks like the easiest: nothing. No daily quotes, no panic, no excitement. Twenty-eight years of corn and soybean later, the earnings had tripled and the farm was worth five times the purchase price. The result came from the asset’s produce and from patience — not from cleverly jumping in and out.

India has its own famous voice for the same idea. Raamdeo Agrawal, the co-founder of Motilal Oswal and one of India’s most respected investors, has spent decades teaching a four-word philosophy: “Buy Right, Sit Tight.” Buy right means choose a genuinely good business — quality of the business and the management first, growth in earnings next, and a long-lasting edge (a moat — something that protects a business from competitors, the way a moat of water protected an old fort). Sit tight means hold it for years and let the business do the heavy lifting. Agrawal openly credits Warren Buffett as his inspiration, and his message to ordinary Indian investors has always been the same: the skill is in picking the right business, and the even rarer skill is in sitting still while it grows. Notice that both halves of his philosophy are owner’s behaviour. A ticket-holder can do neither — he cannot “buy right” because he never studies the business, and he cannot “sit tight” because the flashing price will not let him.

And we have all seen the opposite story in our own circles. Think of March 2020, when the market crashed during the Covid panic. Two neighbours could hold shares of the very same strong company. The one who thought of it as a blinking number sold in fear near the bottom and locked in his loss forever. The one who thought of it as part-ownership of a fine business asked a different question — “Will people stop buying paint, or biscuits, or medicines five years from now?” — answered “obviously not,” held on, and watched both the business and his wealth recover. Same company, same crash, opposite outcomes. The difference was not intelligence or inside information. It was simply what each of them believed a share to be.

How you can use it from tomorrow morning

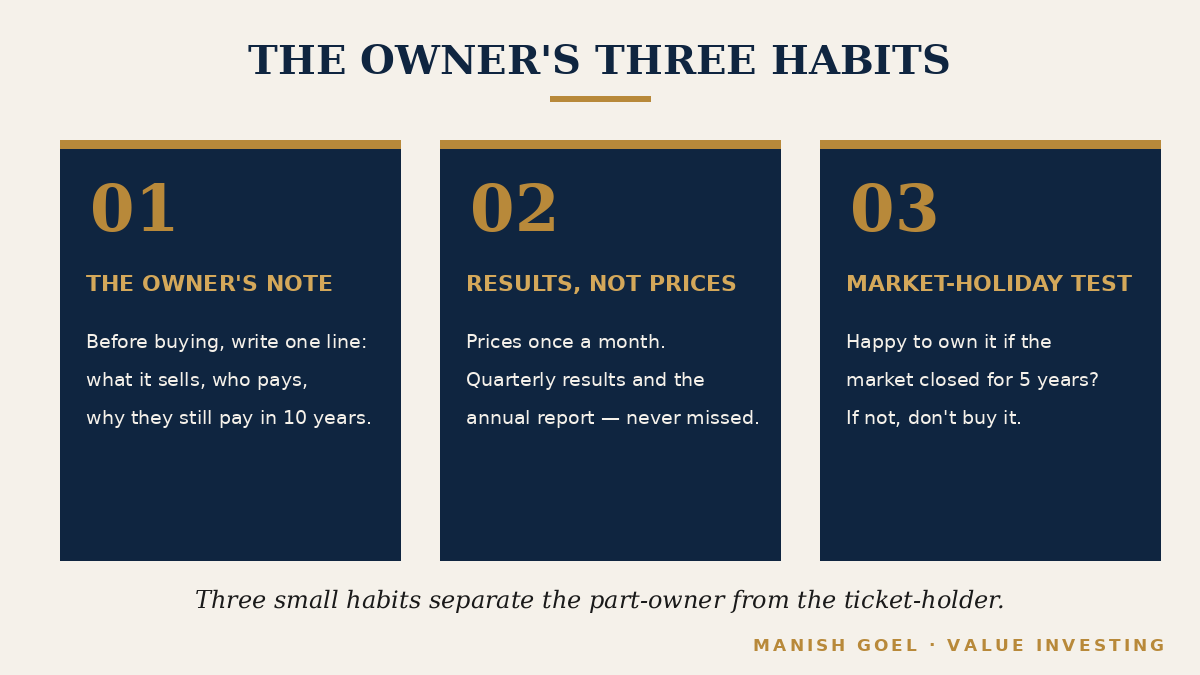

One — write the owner’s note before you buy. Before buying any share, write one plain sentence in a notebook: “This company sells ___, its customers are ___, and they will keep paying for it ten years from now because ___.” If you cannot fill in the blanks, you are not ready to be an owner of that business yet — you would only be holding a ticket. This one small habit filters out most bad decisions before they happen.

Two — track results, not prices. Decide a fixed, low frequency for looking at prices — once a week, or even once a month — and keep that promise. In exchange, never miss the things an owner reads: the quarterly results every three months and the annual report once a year. Watch four simple items — are sales growing, are profits growing, is debt under control, and does the management speak honestly about both good news and bad. If those four stay healthy, the daily price needs no babysitting from you.

Three — apply the market-holiday test. Before buying, ask yourself: “If the stock market closed for the next five years and I could not sell, would I still be happy owning this business?” Buffett has often offered exactly this test, with a ten-year holiday. If the thought makes you uncomfortable, you do not really trust the business — you only trust the exit door. An owner trusts the shop; only a gambler keeps one eye on the door.

Key takeaways

- A share is not a lottery ticket; it is part-ownership of a real business — the business behind the share is your actual asset.

- Buffett ran his Nebraska farm for decades without ever seeing a daily price quote; he watched what the farm produced, and the value followed.

- There are two scoreboards — the minute-by-minute price (mood) and the quarterly and yearly results (truth); owners read the second one.

- Raamdeo Agrawal’s “Buy Right, Sit Tight” is the owner’s mindset in four words: pick a quality business carefully, then let time and the business do the work.

- Three habits make you an owner: write a one-line owner’s note before buying, track results instead of prices, and apply the five-year market-holiday test.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.