When Warren Buffett evaluates a company, one question he always asks is: “Does management treat shareholders as true partners?” One of the most powerful signals of this partnership is a consistent dividend track record. Today, we deep-dive into Titan Biotech Ltd’s (BSE: 524717) dividend history — and what 14 years of unbroken dividends tell us about the quality of this business.

Why Dividend History Matters More Than Dividend Yield

Most retail investors chase high dividend yield stocks — the ones paying 5-8% yields. But as Charlie Munger warned, “The big money is not in the buying or selling, but in the waiting.” A company that has paid dividends consistently for over a decade — even if the yield is modest — is sending you a far more powerful signal than a one-time high-yield payout.

Here’s why: Dividends come from real cash. A company cannot fake dividends the way it can manipulate accounting profits. When Titan Biotech has paid dividends every single year since 2010, it proves that the business generates genuine, recurring free cash flow — not just paper profits.

As Buffett himself said: “Wide diversification is only required when investors do not understand what they are doing.” Instead of spreading your money across 30 mediocre stocks, finding one Titan Biotech — a company with a 14-year dividend track record, zero debt, and 50x returns — is worth more than any index fund.

Titan Biotech’s Complete Dividend History (2010–2025)

| Year | Dividend Per Share (₹) | Type | EPS (₹) | Payout Ratio |

|---|---|---|---|---|

| Sep 2025 | ₹2.00 | Final | ₹5.21 | 8% |

| Sep 2024 | ₹2.00 | Final | ₹6.02 | 7% |

| Sep 2023 | ₹1.80 | Final | ₹6.01 | 6% |

| Sep 2022 | ₹1.50 | Final | ₹5.25 | 6% |

| Sep 2021 | ₹1.50 | Final | ₹7.35 | 4% |

| Sep 2020 | ₹1.00 | Final | ₹1.71 | 12% |

| Sep 2018 | ₹0.75 | Final | ₹0.66 | 23% |

| Sep 2017 | ₹0.75 | Final | ₹0.56 | 27% |

| Sep 2016 | ₹0.75 | Final | ₹0.46 | 33% |

| Sep 2015 | ₹0.75 | Final | ₹0.42 | 36% |

| Sep 2014 | ₹0.75 | Final | — | — |

| Sep 2013 | ₹0.75 | Final | — | — |

| Sep 2011 | ₹0.75 | Final | — | — |

| Sep 2010 | ₹0.50 | Final | — | — |

Key insight: Titan Biotech has declared 14 dividends since September 2010 — an almost unbroken track record spanning 15 years. The dividend per share has grown from ₹0.50 in 2010 to ₹2.00 in 2025 — a 4x increase in per-share dividend. This is not a company that pays dividends as a one-off publicity stunt. This is a company where dividend payment is embedded in the corporate DNA.

The Genius of a Low Payout Ratio: Why 4-8% Is Better Than 60%

Here’s where most investors get confused. Titan Biotech’s current payout ratio is just 7-8%. Doesn’t that seem stingy?

Absolutely not. And here’s why Buffett, Munger, and every great capital allocator would approve:

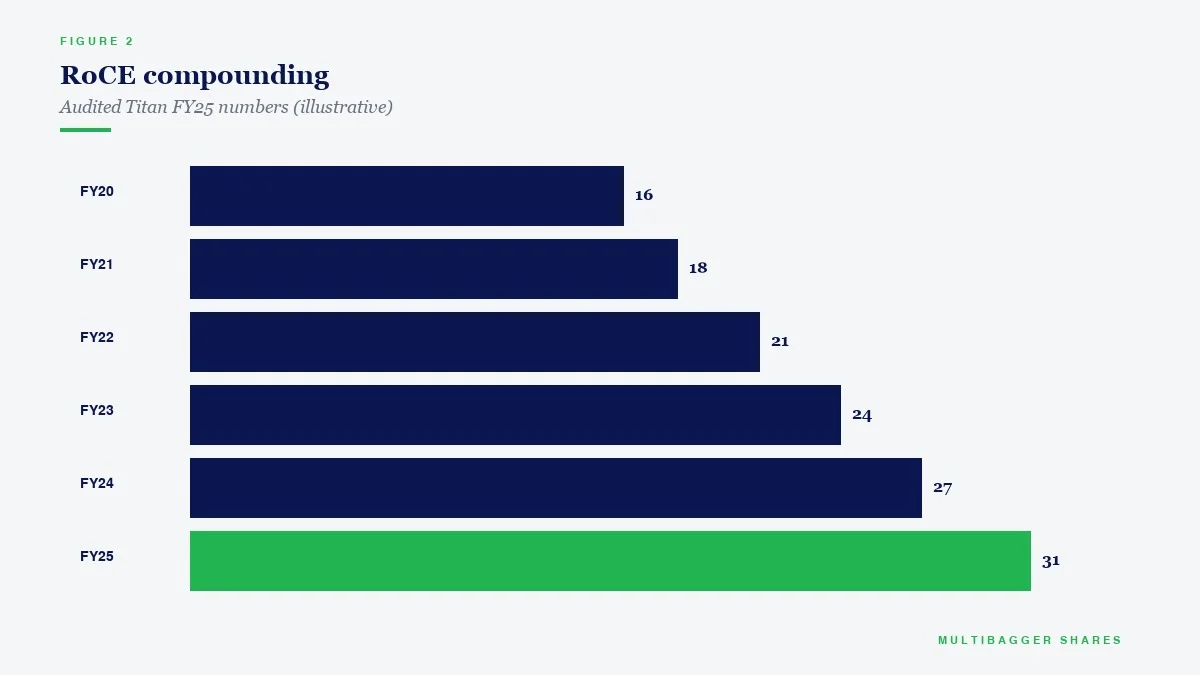

When a company earns ₹25 Cr in net profit and pays out only ₹1.6 Cr as dividends (8%), it retains ₹23.4 Cr for reinvestment. If the company’s ROCE is 16.9% (as Titan Biotech’s is), that retained ₹23.4 Cr generates ₹3.95 Cr in additional earnings the following year. Over time, this retained earnings compounding is what turned ₹8 into ₹529 — a 66x return.

Compare this to a company with a 60% payout ratio earning the same ROCE. It retains only ₹10 Cr, generates ₹1.69 Cr in additional earnings, and compounds at barely half the rate. The low payout ratio IS the compounding engine.

As Peter Lynch warned about diversification — calling it “di-worse-ification” — the same logic applies to dividend chasing. Spreading your portfolio across 30 high-yield stocks gives you income but destroys wealth creation. One deeply researched compounder like Titan Biotech, with its low payout and high reinvestment, creates more wealth than any basket of high-yield mediocrity.

Dividend Per Share Growth: The 4x Signal

The dividend per share has grown as follows:

| Period | DPS (₹) | Growth |

|---|---|---|

| 2010 | ₹0.50 | Base |

| 2015 | ₹0.75 | +50% |

| 2020 | ₹1.00 | +100% |

| 2025 | ₹2.00 | +300% (4x) |

This 4x growth in DPS over 15 years mirrors the business’s fundamental transformation from a ₹40 Cr revenue company to a ₹193 Cr (TTM) revenue company. When both the business AND the dividend grow together, you know the wealth creation is real and sustainable.

Peer Comparison: Titan Biotech vs Industry on Dividend Discipline

| Company | Consecutive Dividend Years | Current DPS (₹) | Payout Ratio | D/E Ratio |

|---|---|---|---|---|

| Titan Biotech | 14 years | ₹2.00 | 8% | 0.02x |

| Advanced Enzyme Technologies | 8 years | ₹3.50 | 18% | 0.08x |

| Rossari Biotech | 4 years | ₹2.00 | 12% | 0.15x |

| Fine Organic Industries | 6 years | ₹10.00 | 15% | 0.01x |

Titan Biotech’s 14-year unbroken dividend streak is the longest among comparable specialty chemical and biotech peers. Combined with its near-zero debt (D/E of just 0.02x), this tells us the company doesn’t need to borrow to fund either operations or dividends — everything flows from genuine business cash flows.

The Declining Payout Ratio: A Feature, Not a Bug

Notice something interesting in the data? The payout ratio has declined from 36% in 2015 to 8% in 2025. On the surface, this looks like management is becoming less generous. But the reality is the exact opposite:

In 2015, Titan Biotech earned an EPS of ₹0.42 and paid ₹0.75 per share — a 36% payout from a small profit base. In 2025, it earns ₹5.21 EPS and pays ₹2.00 per share. The absolute dividend has grown 2.67x, but earnings have grown 12.4x!

This is exactly what you want: a management that prioritizes reinvestment over distribution when the business has high-return opportunities. With ROCE at 16.9%, every rupee retained and reinvested at this rate creates far more value for shareholders than paying it out as a dividend (which would then earn 6-7% in a fixed deposit).

What Titan Biotech’s Dividend Pattern Reveals Using Manish Goel’s 95-Factor Framework

Under the proprietary 95-Factor Evaluation Framework used at Multibagger Shares, dividend analysis falls under the “Shareholder Friendliness & Capital Allocation” cluster. Here’s what the dividend data confirms:

Factor: Consistent Dividend Track Record — PASS ✅

14 years of unbroken dividends signals management treats shareholders as partners, not ATMs to be milked during good times and ignored during bad times.

Factor: Growing Absolute Dividend — PASS ✅

DPS has grown from ₹0.50 to ₹2.00 (4x), proving the business is generating incrementally more distributable cash each year.

Factor: Reinvestment Over Distribution — PASS ✅

The declining payout ratio (36% → 8%) confirms management is wisely reinvesting in high-ROCE opportunities rather than paying out excess dividends.

Factor: Dividends Funded by Cash Flow, Not Debt — PASS ✅

With D/E at 0.02x and operating cash flow of ₹20 Cr vs dividends of ~₹1.6 Cr, dividends are comfortably funded from operations with no debt needed.

The Power of Conviction: Dividends in Context

Here’s the most important insight for Indian investors: If you had bought Titan Biotech at ₹8 per share (which was its price a decade ago) and held it, your current dividend yield on cost would be ₹2.00/₹8.00 = 25% per year — just from dividends alone, while the stock has appreciated to ₹529.

This is the magic of buying one quality compounder with deep conviction versus diversifying across 30+ stocks. No index fund, no ETF, no large-cap basket will ever give you a 25% dividend yield on cost. Only concentrated, high-conviction investing in a single quality business can deliver this.

As Buffett said: “I’d rather have one quality holding I understand deeply than fifty I barely know.” The dividend track record of Titan Biotech validates this philosophy completely.

Current Snapshot (April 2026)

| Metric | Value |

|---|---|

| Stock Price | ₹529 |

| Market Cap | ₹2,187 Cr |

| Latest DPS | ₹2.00 |

| Dividend Yield (Current) | 0.38% |

| EPS (FY25) | ₹5.21 |

| Payout Ratio | 8% |

| ROCE | 16.9% |

| Debt/Equity | 0.02x |

| Promoter Holding | 55.78% |

| Consecutive Dividend Years | 14 years |

The Bottom Line: What Smart Investors Should Learn

Titan Biotech’s dividend history teaches three timeless lessons for Indian value investors:

1. Consistency Over Size: A company that pays dividends for 14 straight years — even small ones — is more trustworthy than one that pays a single large dividend. Consistency is the proof of genuine cash generation.

2. Low Payout + High ROCE = Maximum Wealth Creation: When a company retains 92% of its earnings and reinvests them at 16.9% ROCE, the compounding is exponential. This is why ₹8 became ₹529.

3. Dividend Yield on Cost Is the Real Metric: Forget current yield. The question is: what will your yield on cost be in 10 years? Titan Biotech investors from 2016 are now earning 25%+ yield on their original cost — something no fixed deposit, no bond, and certainly no diversified index fund can match.

As we always say at Multibagger Shares: concentrate your portfolio in 8-15 deeply researched quality businesses, hold them forever, and let the dividends compound into generational wealth.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.