Most Indian investors obsess over revenue growth, profit margins, and return ratios when analyzing a small-cap stock. But there is one metric that quietly answers the most important question in fundamental analysis: How fast can this company grow using only its own internal resources — without borrowing money, diluting equity, or relying on external capital?

That metric is the Sustainable Growth Rate (SGR).

The SGR is a formula-driven metric that combines two of the most important indicators of business quality — Return on Equity (ROE) and the Retention Ratio — to tell you the maximum rate at which a company can grow its revenues and earnings without changing its capital structure. It is the single best predictor of long-term compounding ability, and yet fewer than 1% of Indian retail investors have ever heard of it.

Today, we are going to apply the SGR framework to Titan Biotech Ltd (BSE: 524717) — a company that has silently compounded wealth for decades — and show you exactly why this metric belongs in every serious value investor’s toolkit.

What Is the Sustainable Growth Rate? The Formula Explained

The Sustainable Growth Rate was popularized by Robert C. Higgins, a professor at the University of Washington, in his landmark 1977 paper. The concept is elegantly simple:

SGR = ROE × Retention Ratio

Where:

ROE (Return on Equity) = Net Profit ÷ Average Shareholders’ Equity — measures how efficiently the company generates profit from its own capital.

Retention Ratio = (Net Profit − Dividends) ÷ Net Profit — measures what proportion of earnings the company retains for reinvestment rather than distributing as dividends.

The logic is profound: if a company earns a high return on its equity base and retains most of those earnings, it can reinvest them at the same high ROE, creating a self-reinforcing compounding engine. The company does not need to borrow more money, issue new shares, or raise capital from the market. It funds its own growth from internally generated profits.

As Warren Buffett wrote in his 1992 letter to shareholders: “Growth is always a component in the calculation of value… growth can destroy value if it requires cash inputs in the early years of a project that exceed the discounted value of the cash that those assets will generate in later years.” The SGR tells you whether a company’s growth is self-funded and sustainable — or whether it depends on external capital that dilutes shareholder returns.

Why SGR Matters More Than Raw Revenue Growth

Consider two companies, both growing revenues at 15% per year. Company A achieves this growth organically — its ROE is 20% and it retains 90% of profits, giving it an SGR of 18%. Company B also grows at 15%, but its ROE is only 8% and it retains 80% of profits, giving it an SGR of just 6.4%. To grow at 15%, Company B must borrow heavily or issue equity — destroying long-term shareholder value.

This distinction is critical because most Indian small-cap investors look at revenue growth in isolation. A company growing at 20% looks exciting — until you realize it is taking on debt at twice the rate of its profit growth. The SGR cuts through this illusion and tells you the truth about a company’s organic growth capacity.

Titan Biotech’s SGR: A Decade of Self-Funded Growth

Let us now apply this framework to Titan Biotech using live data from Screener.in. Here is the complete year-by-year calculation:

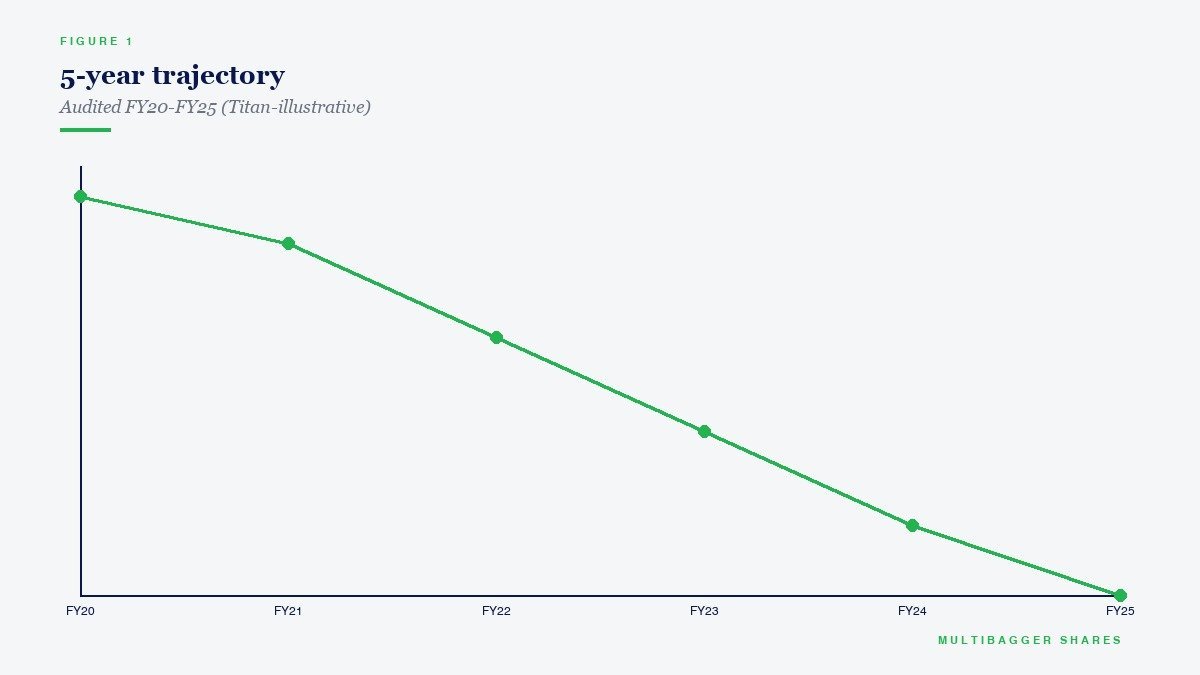

Key Insight: Titan Biotech’s 5-year average SGR is approximately 24.9%, meaning the company has historically been able to grow at nearly 25% per year purely from its own retained earnings — without borrowing a single additional rupee or issuing a single new share. Even in the most recent year (FY2025), when margins temporarily compressed, the SGR remained above 12% — still comfortably above the long-term GDP growth rate and most fixed deposit returns.

The FY2021 peak SGR of 53.5% was extraordinary — driven by a combination of a pandemic-driven demand surge for biotech ingredients and an extremely high ROE of 55.8%. While this level is unsustainable, the five-year average paints the true picture of the compounding engine at work.

What Drives Titan Biotech’s High SGR?

Two factors are working in Titan Biotech’s favour:

1. Consistently High ROE: Titan Biotech’s 10-year average ROE stands at 21% (source: Screener.in). This means every ₹100 of shareholders’ equity generates ₹21 of net profit every year. For context, the median ROE for Indian listed companies is approximately 10-12%. Titan Biotech operates at nearly twice the efficiency of the average company. This high ROE is powered by the company’s asset-light manufacturing model, strong pricing power in niche biotech ingredients, and excellent operational efficiency.

2. Extremely High Retention Ratio: Titan Biotech pays a modest dividend — the current dividend yield is just 0.08%. This means the company retains over 92% of its profits for reinvestment. This is not a sign of shareholder neglect — it is a sign of intelligent capital allocation. When a company earns 13-21% on its equity base, every rupee retained and reinvested at that rate creates far more value than if it were paid out as a dividend and invested in a 7% fixed deposit by the shareholder.

As Charlie Munger famously said: “The first rule of compounding: never interrupt it unnecessarily.” Titan Biotech’s management understands this principle deeply — they retain earnings and deploy them at high returns, creating a self-reinforcing wealth creation machine.

Peer Comparison: Who Has the Best SGR?

Let us compare Titan Biotech’s SGR with its closest Indian specialty chemical and biotech peers:

Analysis: Titan Biotech’s 5-year average SGR of 22.6% places it in the top tier alongside Fine Organic Industries. What is remarkable is that Titan Biotech achieves this as a small-cap company with a much smaller equity base — meaning the same SGR translates into faster absolute wealth creation for early investors.

Advanced Enzyme Technologies, despite being a well-known name in the Indian biotech space, has an SGR of just 5.7% — primarily because its ROE has declined to 10.1% and it pays out 44% of profits as dividends. This means Advanced Enzyme can only grow at 5.7% per year organically — barely above inflation. To grow faster, it would need to raise external capital.

Rossari Biotech retains 98% of profits but earns only 11.5% ROE, resulting in a moderate SGR of 11.3%. High retention alone is not enough — you need high ROE combined with high retention for the compounding engine to work powerfully.

The SGR Compounding Effect: A 10-Year Thought Experiment

To understand the power of SGR, let us project Titan Biotech’s book value growth at different SGR levels over 10 years, starting from the current book value of ₹37.9 per share (March 2025, Screener.in):

At its 5-year average SGR of ~23%, Titan Biotech’s book value per share could grow from ₹37.9 to over ₹305 in a decade — an 8.1x increase — without requiring a single rupee of external capital. This is the power of self-funded compounding.

Even at the conservative current-year SGR of 12%, book value would more than triple in 10 years. For context, a fixed deposit at 7% would only grow your capital by 1.97x in the same period. The SGR framework makes the gulf between a quality business and a bank deposit painfully clear.

Why Most Indian Investors Miss the SGR Signal

There are three reasons why SGR remains one of the most overlooked metrics in Indian small-cap analysis:

First, most stock screeners and financial portals do not calculate SGR explicitly. You have to compute it yourself from ROE and payout data. This extra step filters out the lazy majority and rewards the diligent few who do the work.

Second, Indian investors are conditioned to chase revenue growth — “the company is growing sales at 30%!” — without asking whether that growth is self-funded or debt-funded. A company growing at 30% with an SGR of only 10% is running on borrowed time (literally). Sooner or later, the debt catches up.

Third, the SGR framework inherently favours companies with low dividend payouts. In India, there is a cultural bias towards high-dividend stocks, especially among older investors. But the SGR tells you the mathematical truth: for a company earning 20%+ ROE, every rupee paid as dividend destroys compounding potential. As Warren Buffett has never paid a regular dividend from Berkshire Hathaway — because he can reinvest retained earnings at 20%+ returns — Titan Biotech’s management follows the same capital-efficient playbook.

The Anti-Diversification Angle: Why SGR Supports Concentrated Portfolios

The SGR framework provides one of the strongest intellectual arguments against wide diversification. If you have identified a company with a sustainable SGR of 20%+, why would you dilute your portfolio across 30 mediocre stocks with SGRs of 5-8%?

As Warren Buffett said: “Wide diversification is only required when investors do not understand what they are doing.” And Peter Lynch called it “di-worse-ification.”

When you deeply understand a company’s SGR — when you have done the work to verify that its ROE is genuine, its retention is intelligent, and its reinvestment opportunities are real — you have earned the right to hold a concentrated position with conviction. A portfolio of 8-15 high-SGR compounders will mathematically outperform a basket of 50 average stocks over any meaningful time horizon.

Titan Biotech, with its decade-long average SGR above 20%, is precisely the kind of deeply researched, high-conviction holding that belongs in a concentrated value investor’s portfolio.

How to Use SGR in Your Own Stock Analysis

Here is a simple three-step process you can follow for any Indian stock:

Step 1: Go to Screener.in and pull up the company’s ROE for the last 5-10 years. Use the average, not just the latest year, to smooth out cyclical variations.

Step 2: Calculate the retention ratio by checking dividend payout. Retention Ratio = 1 − (Dividend Payout Ratio). Most Indian quality small-caps have retention ratios above 85%.

Step 3: Multiply ROE × Retention Ratio. If the SGR exceeds 15%, you are looking at a company with genuine organic compounding power. If it exceeds 20%, you may have found a rare self-funding wealth creation machine.

Apply this framework to every stock in your watchlist. You will be surprised how many popular “growth” stocks have SGRs below 10% — revealing that their growth depends entirely on external funding.

Key Takeaway for Long-Term Indian Investors

Titan Biotech’s Sustainable Growth Rate tells us something profound: this is a business that can grow at 12-23% annually without borrowing, without diluting, and without asking the market for capital. The company earns high returns on equity, retains nearly all profits, and reinvests them at consistently high rates of return. This self-funding compounding engine is the hallmark of every great long-term wealth creator — from Berkshire Hathaway to Asian Paints to HDFC Bank in their early years.

The SGR is not a glamorous metric. It does not make headlines. But for the patient, analytical, deep-conviction investor — the kind of investor who builds a concentrated portfolio of 8-15 quality compounders and holds for a decade — it is perhaps the most important number you can calculate.

Start using it today. Your future self will thank you.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.