Most Indian investors who have read a few value-investing books know three names by heart: Benjamin Graham, Warren Buffett and Charlie Munger. A few will throw in Philip Fisher or Peter Lynch. Almost no one talks about Walter Schloss — and that silence is itself a clue. Schloss did not write books, did not appear on television, did not run a research empire of two hundred analysts. He sat in a small windowless room at the back of Tweedy, Browne’s office in Manhattan with his son Edwin, kept a single rotary telephone, refused to use a computer, never met the management of a company he owned, and from 1955 to 2002 quietly compounded his clients’ capital at roughly 16 per cent a year before fees, against the S&P 500’s 10 per cent.

Forty-seven years of beating the market by six percentage points annually, with no MBA, no CFA, no factory visits, no sell-side research subscriptions and no Bloomberg terminal. Just the WSJ, Standard & Poor’s monthly stock guide, the annual report, and the discipline of a man who treated the stock market like a grocery store: judge by the price tag, not the storyteller behind the counter. If there is a single value investor whose method translates almost word-for-word to the situation of a serious Indian retail investor in 2026, it is Schloss — and yet he is the most under-quoted name in our community.

The 16 Factors — Schloss’s Working Manual, Not a Theory

In the early 1990s Schloss put down on paper what he had been doing for forty years. He called it “Factors Needed to Make Money in the Stock Market.” The list reads less like a framework and more like the working notes of a craftsman finally asked to explain his trade. The full list runs to sixteen items; let me distil the seven that matter most for an Indian investor sitting in front of an annual report tonight.

One — price is the most important factor in relation to value. Schloss insisted that the cheapness of a stock relative to its assets is the single largest predictor of long-term return. He rarely paid more than book value and frequently paid much less. In an Indian market where small-cap quality regularly trades at three to six times book without flinching, this is a radical anchor.

Two — try to establish the value of the company. Schloss meant balance-sheet value first, earnings power second. Cash, receivables, inventory at conservative valuations, fixed assets at depreciated cost minus liabilities — that is your floor. Earnings can be massaged; assets can be touched.

Three — use book value as a starting point. Not as a verdict, but as the soil from which the analysis grows. A company growing book value per share at fifteen per cent a year for a decade is, almost by definition, creating wealth at the balance-sheet level. The market price is a secondary phenomenon to that primary fact.

Four — have patience. Stocks don’t go up immediately. Schloss’s average holding period was four to five years. He bought when nobody wanted the stock and sold when the crowd showed up. The Indian small-cap investor who cannot stomach two flat quarters has already disqualified himself from the Schloss method.

Five — don’t buy on tips. Schloss read the company’s reports and made his own decision. He did not call brokers. He did not act on WhatsApp forwards. In 2026 India, where the average retail investor receives forty buy-recommendation messages a day across telegram channels and stockbroker apps, this single rule, if obeyed, would protect more capital than any other.

Six — buy assets at a discount rather than buy earnings. Schloss’s reasoning was simple: earnings change quickly with the business cycle; assets — buildings, plant, working capital, cash — change slowly. A discount to assets is a more durable margin of safety than a discount to last year’s earnings.

Seven — listen to suggestions from people you respect, but don’t follow them blindly. Schloss was friends with Buffett and Graham. He listened, then checked everything himself.

Notice what is absent. No rule about CEO interviews, scuttlebutt, macro positioning, technical charts, quarterly beats, or concentration into ten conviction names. Schloss often held sixty to a hundred stocks at a time and considered that a feature, not a bug — his edge came from buying many cheap things and waiting, not from being heroically right about a few.

Why the Schloss Method Fits the Indian Retail Investor Better Than Fisher’s or Pabrai’s

The conversation in Indian value-investing circles tilts heavily toward Philip Fisher’s scuttlebutt method or Mohnish Pabrai’s concentrated Dhandho framework. Both are brilliant. Both are also hard to execute as a working professional in a Tier-2 Indian city. You cannot fly to Hyderabad to interview the plant manager of a small-cap chemical company. You cannot call up the CFO of a five-hundred-crore promoter-driven business and expect a return call. You cannot match Pabrai’s nerve to put 25 per cent of the portfolio into a single stock when your entire savings are at stake.

Schloss’s method requires only what is freely available: an annual report, a screener, a pen, and the temperament to do nothing for years at a time. The annual report alone — properly read — contains every input Schloss used to compound at 16 per cent for nearly half a century. That is the most democratic insight in the value-investing canon, and it is the one most Indian retail investors have never heard.

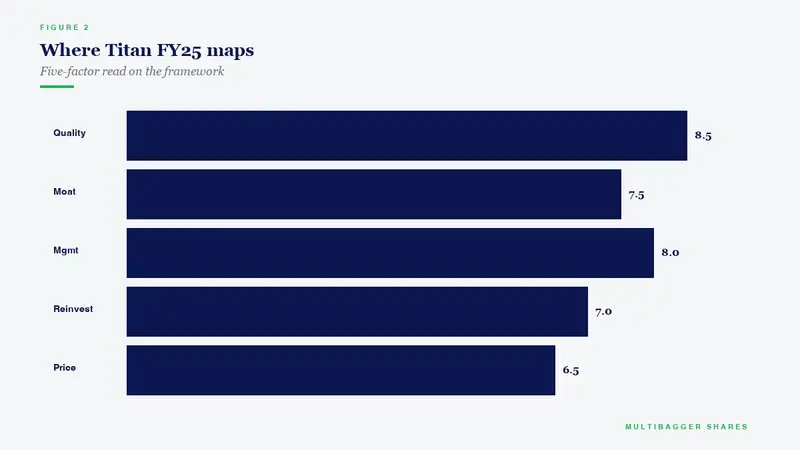

How Titan Biotech’s FY25 Numbers Illustrate the Schloss Framework

Titan Biotech (BSE: 524717), the small-cap Delhi-based biotechnology and pharmaceutical ingredient manufacturer with operations in over a hundred countries, is a useful mirror for the Schloss factors. I am not making any valuation comment here — only showing how the audited FY25 numbers map onto Schloss’s seven essential factors above.

Book value per share has compounded roughly nine times in eleven years. Schloss’s third factor — book value as the starting soil — finds a clean illustration here. Wealth has been built at the balance-sheet level first, before the share price ever recognised it.

Debt-to-equity in FY25 stands at approximately 0.02 — effectively a debt-free balance sheet. A net cash position of around forty crore rupees from a starting point of net debt a decade ago. Schloss favoured companies whose balance sheet alone could survive almost any storm. This is exactly the asset-led safety he was pointing at in factor six.

Promoter holding has risen from forty-eight per cent to fifty-five point eight seven per cent over the last several years through open-market purchases — zero pledging. Schloss’s trust was in numbers and behaviour, not management charisma. The behaviour of insiders steadily increasing skin in the game speaks louder than any concall ever could.

Return on capital employed has held in the high teens — around sixteen point nine per cent in FY25 — with operating margin compounding from roughly ten per cent to nineteen per cent. Schloss did not hunt for high-quality operating economics; he hunted for cheap balance sheets. But a cheap balance sheet that also happens to compound earnings power was the rare case where his patience paid extraordinary dividends.

Fourteen consecutive years of unbroken dividends paid out of growing earnings, while still building a roughly thirty-eight crore rupee cash war chest. Schloss watched what management did with cash, not what they said. Fourteen years of disciplined capital allocation plus net cash accumulation is exactly the behaviour pattern he would have noticed without picking up the phone.

Revenue grown at roughly fifteen per cent CAGR for over a decade, with thirty-four point five per cent of revenue exported to over a hundred countries. Schloss’s fourth factor was patience. A decade of steady fifteen per cent compounding does not look exciting on a quarterly chart. It looks extraordinary on a fifteen-year chart.

Six audited FY25 datapoints, every one of which a Schloss-style investor at his kitchen table could have extracted from the published annual report — no factory visit, no management call, no analyst access required. That is the point.

The Takeaway You Can Use Tonight

Schloss’s quiet 16 per cent compounded for 47 years out of a back office in Manhattan tells us something the loud value-investing influencer ecosystem in India will not. You do not need access, contacts, a Bloomberg terminal or a friendship with the promoter. You need an annual report, a calculator, the discipline to anchor on price-to-assets rather than price-to-narrative, and the patience to hold for five years while Dalal Street rotates through six market cycles.

Pull out one annual report tonight. Not the investor presentation — the audited statements. Read the balance sheet first, the cash flow second, the P&L third, and the management discussion last. Then ask Schloss’s seven questions. If the answers are good and the price is below your estimate of asset-based value, you have a candidate worth following for four years. If not, move to the next report. That is the entire method. It worked for forty-seven years for a man with no MBA, no laptop and no ego. It will work for you too, if you let it.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.