Value Investing — Educational Series

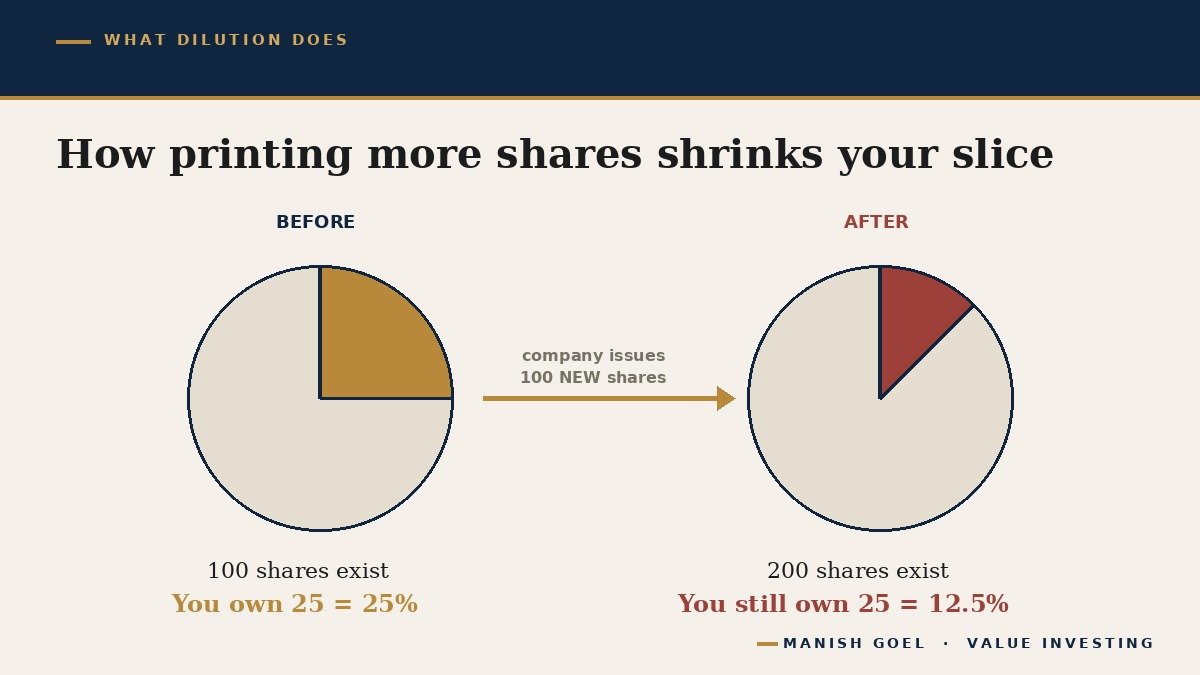

Imagine four friends open a small tea stall near a busy railway station. To keep it fair, they print 100 paper slips that say “I own a piece of this stall.” Each friend takes 25 slips. So each one owns 25 out of 100 slips — that is one-fourth, or 25%, of the stall. At the end of the year the stall earns ₹100. Each friend’s slice of that profit is ₹25.

Now suppose the stall needs money for a second cart. Instead of saving up, the friends quietly print 100 brand-new slips and hand them to an outsider in exchange for cash. There are now 200 slips in total. Your 25 slips have not changed — but they are now 25 out of 200, which is only one-eighth, or 12.5%. Your ownership has been cut in half without you selling a single slip. If the stall still earns only ₹100, your share of the profit drops from ₹25 to ₹12.50.

This quiet shrinking of your slice has a name in the stock market: share dilution. It is one of the most important ideas a beginner can learn, because it works silently in the background. The share price on your screen does not warn you about it. Yet over many years, dilution can quietly eat a large part of the wealth you thought you owned. Today, in very simple words, let us understand what it is, why it matters, and how it helps you tell a high-quality business from a weak one.

What share dilution really means

When you buy a share of a company, you are buying a tiny piece of that whole business — exactly like one of those tea-stall slips. The total number of slips a company has issued is called its shares outstanding (the full count of all the ownership pieces that exist). Your stake in the business is simply your shares divided by this total.

Dilution happens when a company creates and gives out new shares. Suddenly there are more pieces of the same business. Each old piece — including yours — now represents a smaller fraction of the company. You did nothing wrong, you did not sell, yet your ownership percentage falls. It is like a joint family property being divided among more and more cousins: each person’s share of the same house keeps getting smaller as new claimants are added.

Companies issue new shares for several reasons. Sometimes they sell a big block to large investors to raise money — this is called a placement. Sometimes they give shares to staff as a reward, known as ESOPs (Employee Stock Ownership Plans — shares handed to employees instead of, or on top of, salary). Sometimes they have borrowings (loans) they cannot repay, so they convert that debt into new shares. Every one of these adds slips to the pile and shrinks your slice a little more.

There is a simple piece of jargon that captures this, and you will see it in every company’s results. It is EPS, or earnings per share (the company’s yearly profit divided by its number of shares — in other words, the profit sitting behind each single share). Companies actually report two versions side by side. Basic EPS uses the shares that exist today. Diluted EPS is more honest: it also counts the shares that will probably be created later from ESOPs, convertible loans and similar promises. Diluted EPS is almost always a little lower than basic EPS, because the profit is being spread over a larger number of shares. When the gap between the two is wide, it is a warning that a lot of fresh shares are waiting in the wings to shrink your slice.

Why dilution can quietly cost you money

Here is the part that beginners almost always miss. As an investor, you do not really care about the company’s total profit. You care about the profit that belongs to each share you own. A company can grow its overall profit year after year, and yet you can still go nowhere — if the number of shares is growing just as fast, or faster.

Think of it like sharing a thali (a meal plate) at a dhaba. The kitchen may cook a bigger and bigger plate of food every year — that is the rising total profit. But if more and more people keep sitting down at the same table, the portion that actually reaches your mouth may stay the same or even shrink. What fills your stomach is your portion, not the size of the whole plate. In investing, your portion is the profit per share, and dilution keeps adding more people to the table.

This matters enormously for the magic of compounding (earning returns on your past returns, so wealth snowballs over time). Compounding only helps you if it works on a per-share basis. If a company doubles its profit over five years but also doubles its share count, the profit behind your share has not grown at all. The snowball never gets rolling. This is why a quietly rising share count is such a silent thief: the headline numbers in the news look healthy, while the value behind your specific shares stands still.

Compare it with a simple fixed deposit (FD) in a bank. When you put ₹1 lakh in an FD, nobody can quietly come along and split your deposit with a stranger; the full interest belongs to you alone. A share is different. The company’s management can, by issuing new shares, invite fresh owners to sit at the same table and share the very profits you were counting on. That is not always a bad thing — but it means you must watch the number of owners, not just the size of the profit. An FD protects your portion automatically; a share does not.

A weak business and a strong one

The clearest way to feel the difference is to look at two very different kinds of companies. Remember, these are only stories to learn from — not advice to buy or sell anything.

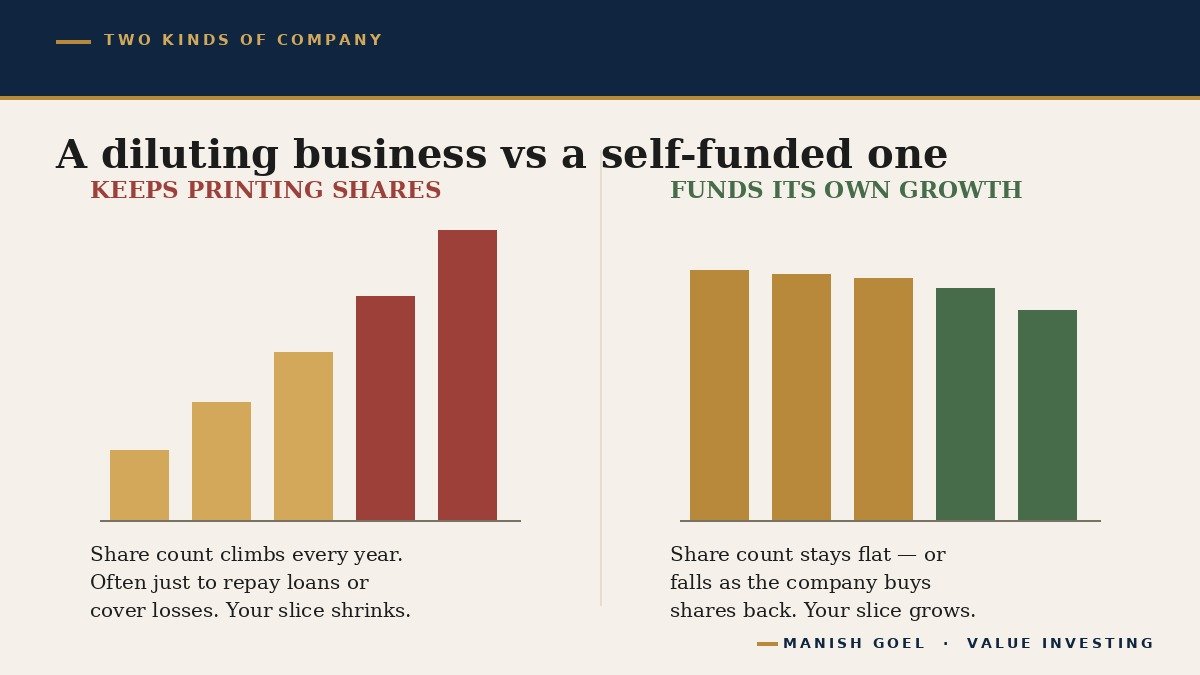

Consider the troubled telecom company Vodafone Idea. Weighed down by huge loans and years of losses, it has had to raise money again and again by printing new shares. In a single recent year its share count rose by roughly 43%. In April 2024 alone it sold nearly 1.4 billion new shares in one placement at about ₹14.87 each. When a business issues shares on that scale simply to survive and pay its bills, every existing owner’s slice is squeezed smaller and smaller. The pizza is being cut into ever more pieces, and not because the pizza is getting bigger — but because the company is desperate for cash.

Now look at the opposite kind of business. India’s large software services company TCS has, for years, generated far more cash than it needs to run and grow. Instead of issuing new shares, it has done the reverse: it has repeatedly bought back its own shares from the market — in 2017, 2018, 2020, 2022 and 2023, returning roughly ₹66,000 crore to shareholders. A buyback reduces the number of shares, so each remaining slice becomes a slightly bigger piece of the same business. This is the behaviour of a strong, self-funded company: it grows from its own cash flow (the actual cash the business earns each year) and does not need to keep asking shareholders for more.

The greatest investors watch this closely. Warren Buffett, in his 1992 letter to Berkshire Hathaway’s shareholders, wrote that the company had “a firm policy about issuing shares… doing so only when we receive as much value as we give.” In plain words: he refuses to print new shares unless the company gets back full value in return, because he treats every shareholder as a partner whose slice must be protected. A management team that thinks this way is showing you something precious — respect for the people who already own the business.

One special form of dilution is worth a beginner’s attention because it is so common today: ESOPs. Giving employees shares can be a fine way to keep talented people motivated, and a small, sensible ESOP pool is normal in good companies. The trouble starts when a company hands out shares to staff so generously, year after year, that the share count keeps swelling and the owners’ slices keep thinning. This is why reading the diluted EPS is so useful — it already counts these promised employee shares, so it quietly reveals how heavy the giveaway really is. A little is healthy; a flood is a red flag.

How you can use this idea

You do not need to be an accountant to put this to work. Here are three simple, practical habits any ordinary investor can follow.

First, track the share count over many years. Before you get excited about a company, look at its number of shares outstanding for the last five to ten years. Most free stock websites show this. Is the count roughly flat, slowly falling, or quietly climbing? A business that grows its profits while keeping its share count steady is doing the hard work the honest way — from its own earnings. A share count that keeps ballooning deserves a careful second look.

Second, always read the diluted EPS, not just the basic one. In every results table the two sit next to each other. If diluted EPS is much lower than basic EPS, it tells you a large wave of new shares is on the way. If the two are almost the same, the company is barely diluting — a quiet sign of quality.

Third, ask why the company is issuing shares. This is the most important question of all. There is a healthy kind of dilution and an unhealthy kind. A profitable company that issues a modest number of shares to fund a genuinely promising new factory may reward you later. But a company that prints shares again and again just to repay old loans, or to cover never-ending losses, is usually a weak business handing you a smaller and smaller piece of its problems. The reason behind the dilution separates the two.

Notice that none of this is about whether a share is “cheap” or “expensive.” We are not trying to put a price on the stock at all. We are simply learning to spot a mark of quality: a business so strong that it funds its own growth and rarely needs to dilute its owners. That kind of company is worth understanding deeply, whatever its price tag.

Key takeaways

- A share is a slice of a whole business; when a company prints new shares, your slice shrinks — this is called share dilution.

- What matters to you is profit per share, not the company’s total profit; a rising share count can keep your slice stuck even as total profit grows.

- Always read diluted EPS, not just basic EPS — a wide gap warns that many new shares are coming.

- Weak businesses dilute again and again just to survive; strong, self-funded ones keep the share count steady or even buy shares back.

- Before investing, check the share count over five to ten years and ask why the company is issuing shares.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.