Value Investing — Educational Series

A caterer who spends your money first

Think about a wedding caterer in your town. The wedding is two months away, but the family pays most of the bill today, in advance, to book the date. The caterer takes that cash and uses it to run the kitchen, pay small advances to his cooks, and even take the next booking — long before he has spent a single rupee on your event. He is, very simply, running his business on your money.

Now think about your gym. You pay a full year’s fee on day one. The gym has your money for twelve months, but it gives you the service slowly, month by month. The same thing happens with a magazine subscription, an insurance premium, or an advance you pay to a contractor to start building your house. In every case, the customer pays first and gets the product or service later.

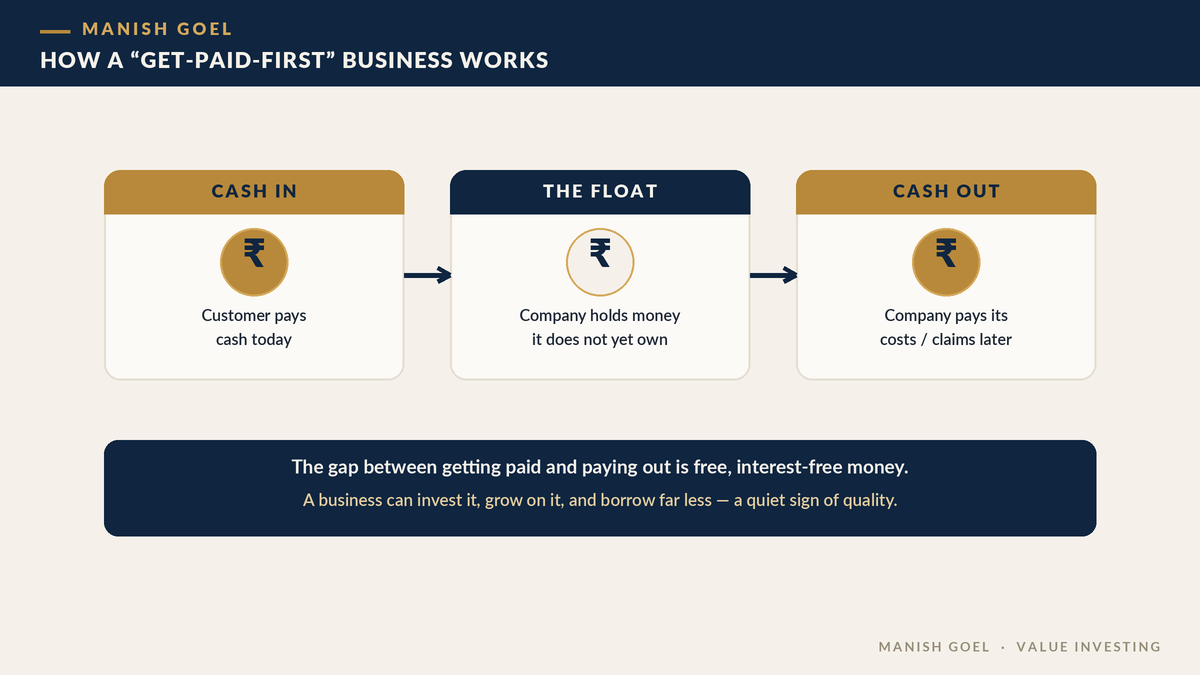

Most of us never notice this. But some of the best businesses in the world are built exactly on this quiet idea — get paid before you spend. When a company collects cash from its customers earlier than it has to pay its own bills, it ends up holding a big pile of money that is not really its own, yet it can use that money for free. Warren Buffett, widely seen as the greatest investor of our time, gave this pile of money a simple name: float. Learning to spot it is one of the most useful skills a beginner can build, because it points you straight towards high-quality businesses.

What “float” really means

Let us define the two terms you will meet today, in the plainest words.

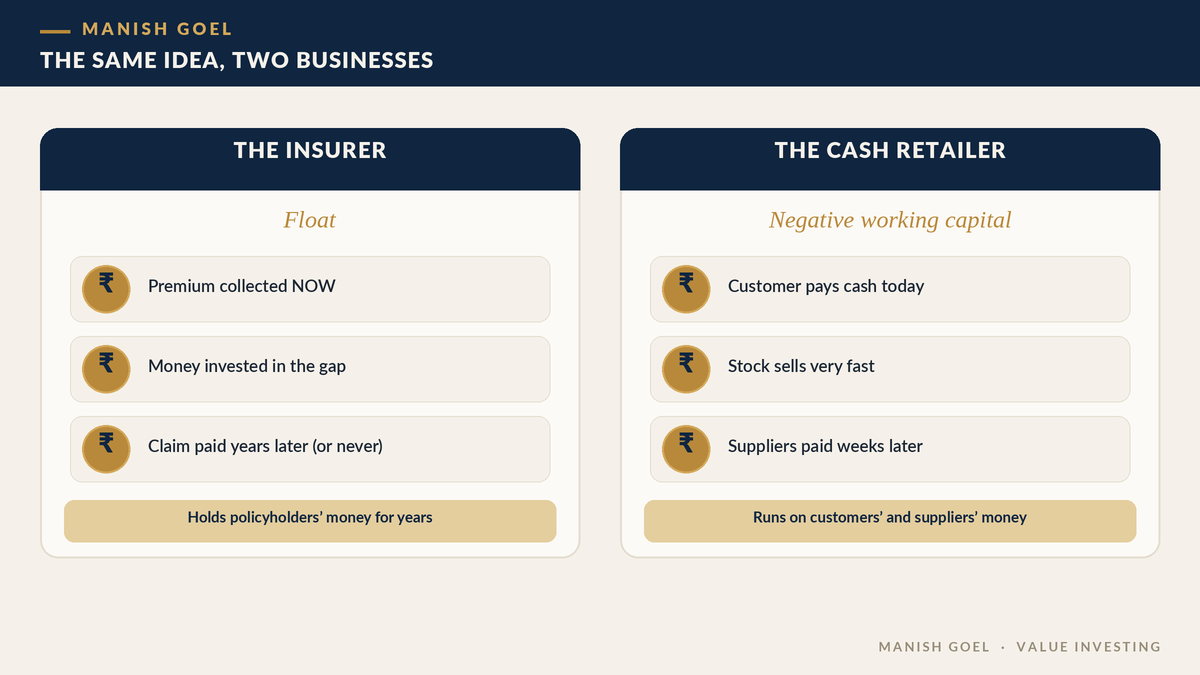

Float is money a company holds but does not own. Buffett describes it exactly like that — “money we hold but don’t own.” The clearest example is insurance. When you buy a health or car insurance policy, you pay the premium now. The company may have to pay a claim only years later — or never. In the gap between collecting your premium and paying any claim, it holds your money and can invest it. Multiply this by crores of policyholders and you get an enormous pool of cash sitting in the company, available to be put to work, even though it will eventually be paid out.

Negative working capital is the same idea wearing different clothes. “Working capital” (the everyday money a business needs to run — to hold stock and wait for customers to pay) is normally a cost you must fund. But in some businesses the customer pays in cash immediately, while the suppliers are paid weeks later. So instead of the business funding its day-to-day cycle, its customers and suppliers fund it. The number turns negative, which sounds like a problem but is actually a sign of strength here. The shop is, in effect, running on other people’s money.

Here is the homely way to remember it. A normal business is like you buying vegetables, cooking, and only later hoping a guest pays you back — your own money is stuck in between. A float business is like a guest handing you the money first, and the sabziwala letting you pay him next week. You are sitting in the middle holding cash that is not yet yours. That cash is the float.

Why this is such a powerful sign of quality

This matters for one simple reason: free money compounds. (Compounding just means earning returns on your past returns — like interest on interest, or a snowball getting bigger as it rolls downhill.) A business that gets paid first does not have to borrow as much from banks, so it pays less interest and carries less risk. It can fund its own growth — new stores, new factories, new products — from the cash its customers have already handed over. Less debt, more self-funded growth: that is a recipe for a business that can survive bad years and keep compounding for decades.

There is a second, deeper benefit. Because the business uses other people’s money to grow, the owners (the shareholders, which is what you become when you buy a share) need to put in very little of their own money. So the profit they earn, measured against their own small investment, looks very high. This is why so many “wonderful businesses” — the kind that turn a small sum into a large one over many years — quietly share this feature. They are growing on a cushion of free cash that keeps refilling itself.

And that refilling is the magic part. You might worry that the float is only borrowed for a while — surely the insurer must pay the claims, and the shopkeeper must pay the suppliers? Yes, but as old money flows out, new money flows in: fresh premiums, the next day’s cash sales, the next year’s subscriptions. It is like a water tank where the inflow tap runs as fast as the outflow tap, so the tank stays full even though the water keeps changing. As long as the business stays healthy and keeps getting customers, the pool of free money never really empties. In practice it behaves like a loan the company never has to fully repay — and often pays no interest on.

And notice what we are not doing. We are not asking whether the share is cheap or expensive today. We are asking a quality question: does this business get paid before it pays? A high-quality business is worth understanding at any price. Float and negative working capital are clues that you may be looking at one.

A real story — and an Indian one too

The most famous example in the world is Warren Buffett’s. In 1967 he bought a small insurance company called National Indemnity. At that time the float — the pile of policyholders’ money it held — was about 16 million dollars. Buffett saw something most people missed: if the insurer was run carefully, that float was like an interest-free loan that never had to be fully repaid, because as old policies ended new premiums kept coming in. He could invest that money and keep the profits.

Over the decades he repeated the trick, buying more insurers such as GEICO. By the end of 2024, the float held by his company, Berkshire Hathaway, had grown to roughly 171 billion dollars — from 16 million to 171 billion, a rise of about eight-thousand times since 1967. Buffett has called this float “money we hold but don’t own,” and in good years it has cost the company less than nothing, because the insurance business itself made a small profit on top. A river of free money to invest, refilling every single day: that, more than any clever stock pick, is the engine behind one of history’s greatest fortunes.

You do not have to look abroad to see the idea. India’s big consumer companies live on it. Hindustan Unilever — the maker of everyday brands like soap, shampoo and tea — has run with negative working capital for many years. Shopkeepers and distributors effectively fund its cycle: the goods sell quickly for cash while suppliers are paid later. The supermarket chain DMart works the same way — it sells groceries for cash to customers every day but pays many of its suppliers only after a short gap, and it turns over its stock very fast. The result is a business that needs surprisingly little outside money to grow. (These names are only examples to explain the idea — nothing here is a suggestion to buy or sell any share.)

Indian insurance shows the float idea at its purest. When crores of Indians pay their yearly life-insurance or health premiums, the insurer collects that cash today and may pay out only far in the future. The Life Insurance Corporation of India — the insurer almost every Indian family has heard of — sits on an enormous pool of policyholders’ money for exactly this reason. The lesson is not about any one company’s share; it is that the structure of an insurance business hands it a giant, slow-moving pile of cash to invest. That is the same engine Buffett spotted in 1967, just closer to home.

Even institutions you use daily run on float. When you book a train ticket weeks ahead, or pay a year’s school fees in advance, or recharge your mobile, or buy a gift card, someone is holding your money before delivering the service. Once you start noticing it, you will see “get paid first” businesses everywhere — and you will start to understand why some of them are so strong and steady.

How you can use this as an ordinary investor

You do not need a finance degree to put this to work. Here are three simple things any beginner can do.

1. Ask the “who pays first?” question. For any company you are studying, ask in plain words: does the customer pay before or after the company spends its money? Insurance, subscriptions, memberships, prepaid services and fast-selling cash retailers usually get paid first. A company that has to build expensive things and wait months to be paid (many construction or heavy-project businesses) does the opposite. The first kind enjoys a quiet, structural advantage.

2. Check the cash, not just the profit. In a company’s yearly report, look for a line called “cash flow from operations.” If a business is genuinely collecting cash early, this number tends to be strong and steady — often as big as, or bigger than, its reported profit. Float should show up as real cash in the bank, not just numbers on paper. (Cash flow from operations simply means the actual cash the main business brought in during the year.)

3. Make sure it is strength, not stress. Here is the one caution, and it matters a lot. Negative working capital is a sign of quality only when it comes from a strong business that customers happily pay in advance. The very same negative number can appear in a weak company that is simply delaying payments to its suppliers because it is short of cash — a sick patient and a fit athlete can have the same heart rate for very different reasons. Tell them apart by checking three things in plain sight: are profits steady, is cash flow from operations healthy, and is borrowing low? If yes, the negative working capital is a genuine edge. If the company is also drowning in debt and its profits keep slipping, the “float” is really just unpaid bills piling up — a warning, not a strength. Free float inside a genuinely good business is a wonderful combination; a cash crunch dressed up as float is a trap to avoid.

Put these three habits together and you have a simple, powerful lens. You are no longer staring only at the share price and guessing. You are asking how the business actually earns and holds its money — and a business that gets paid first, keeps its cash flow strong, and carries little debt is exactly the kind of quality you want to own for the long run.

Key takeaways

- Float is money a company holds but does not own — cash collected from customers before it must pay its own costs.

- Getting paid first means a business can grow on other people’s money, borrow less, and earn high returns on the owners’ small investment.

- Buffett built much of his fortune on insurance float, which grew from about $16 million in 1967 to roughly $171 billion by 2024.

- In India, the idea shows up as negative working capital in strong consumer and retail businesses that sell for cash and pay suppliers later.

- Treat it as a quality clue, not a valuation tool — and always check that the negative number is a sign of strength, not of a cash shortage.

— Manish Goel