Value Investing — Educational Series

Imagine you buy a small flat in your city for ₹50 lakh. You plan to keep it for twenty years. A few months later, a property dealer knocks on your door and says, “Prices have softened — today your flat might fetch only ₹42 lakh.” A year after that, another dealer says, “The area is booming now — you could get ₹65 lakh.” The walls have not moved. The roof has not leaked. You are still living in the same home. So the real question is simple: have you actually lost or gained anything? The honest answer is no — not unless you are forced to sell on the day the quote is low, or the building itself turns out to be unsafe.

Shares work exactly the same way, but most beginners forget it. They see the price of a good company fall on their phone screen and feel they have “lost money,” even though they have not sold a single share and the business is doing just fine. This confusion sits at the heart of one of the most important lessons in all of investing: volatility is not risk. The day-to-day up-and-down of prices is not the same thing as the danger of truly losing your money. Today, in very plain words, let us understand the difference — because once you do, market falls will frighten you far less, and you will make far better decisions.

A quick promise before we begin: this is not about whether the market is “cheap” or “expensive” today, and it is not a tip to buy or sell anything. It is about something deeper — what the word risk actually means, and how the world’s greatest investors think about it very differently from everyone else.

Two words everyone mixes up

Let us define our two words slowly and clearly, because almost everyone blurs them together.

Volatility simply means how much a price jumps around in the short term — up one week, down the next. A share that swings widely is called “volatile.” Think of the price of tomatoes in the mandi: cheap after a good harvest, dear after heavy rain, calm again a month later. The tomatoes are the same tomatoes. Only the daily price tag is restless. Volatility is just that restlessness of the price tag.

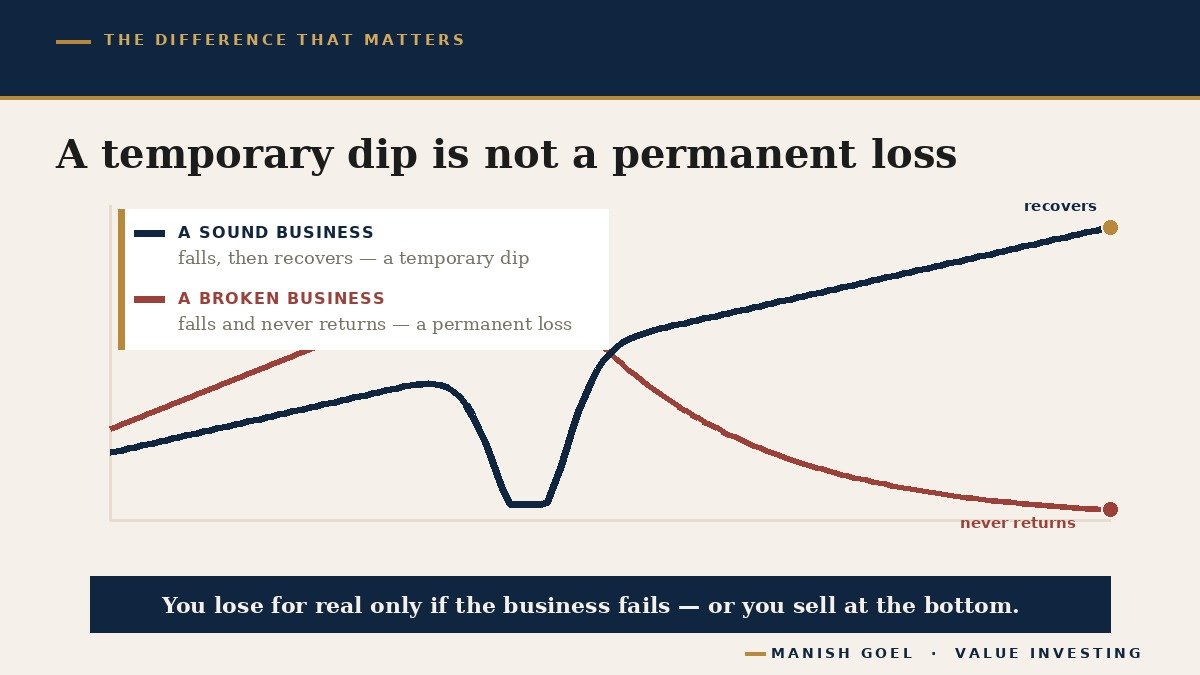

Risk, for a sensible long-term investor, means something far more serious: the chance of a permanent loss of capital — that is, the danger of losing your original money (your capital) for good, with no way to ever get it back. A temporary fall that later recovers is not a permanent loss. A loss becomes permanent only in two ways: either the business you own genuinely fails — it goes bankrupt, drowns in debt, or slowly dies — or you are forced to sell at the bottom, turning a paper fall into a real, locked-in loss.

Hold on to that distinction, because it is the whole lesson. A falling price is not a loss. It is only a quote — an offer of the day. You lose money for real only if the business is broken, or if you sell into the panic. As Howard Marks, one of the most respected investors alive, wrote in his book The Most Important Thing: “Permanent loss is very different from volatility or fluctuation. A downward fluctuation — which by definition is temporary — doesn’t present a big problem if the investor is able to hold on and come out the other side.”

Why the great investors refuse to call volatility “risk”

In universities and on trading desks, people often measure “risk” by how much a price wobbles. The more a share jumps about, the “riskier” they call it. The legends of value investing think this is simply wrong — even a little silly.

Warren Buffett, the most successful investor of our age, wrote plainly to his shareholders in 2014: “Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEOs astray.” In simple words: just because a price moves a lot does not mean you are in danger of losing your money. His lifelong partner, Charlie Munger, was even blunter: “Using volatility as a measure of risk is nuts. Risk to us is the risk of permanent loss of capital.”

Why are they so sure? Because in their experience, real danger does not come from the price chart at all — it comes from not understanding what you own. Buffett famously said, “Risk comes from not knowing what you’re doing.” The person who buys a strong, simple business they understand, with little debt, faces very little real risk even if its price swings wildly. The person who buys something they do not understand, or a company buried in loans, faces enormous real risk even if its price happens to look calm for a while.

Here is a thought that surprises beginners: a fixed deposit (an FD, where the bank guarantees your money back with steady interest) has almost no volatility — the number never falls — yet it carries a quiet risk of its own. If your FD earns 6% while prices in the shops rise 7% a year, your money slowly buys less and less over time. No drama, no falling chart, but a real shrinking of your wealth. “No volatility” did not mean “no risk.” And a wonderful business whose share price drops 40% in a panic, only to recover and grow for years afterwards, gave you a very bumpy ride but no permanent loss at all. The calm thing was riskier; the bumpy thing was safer. That is the whole idea, upside down from what most people believe.

A real story: the great fall of 2008

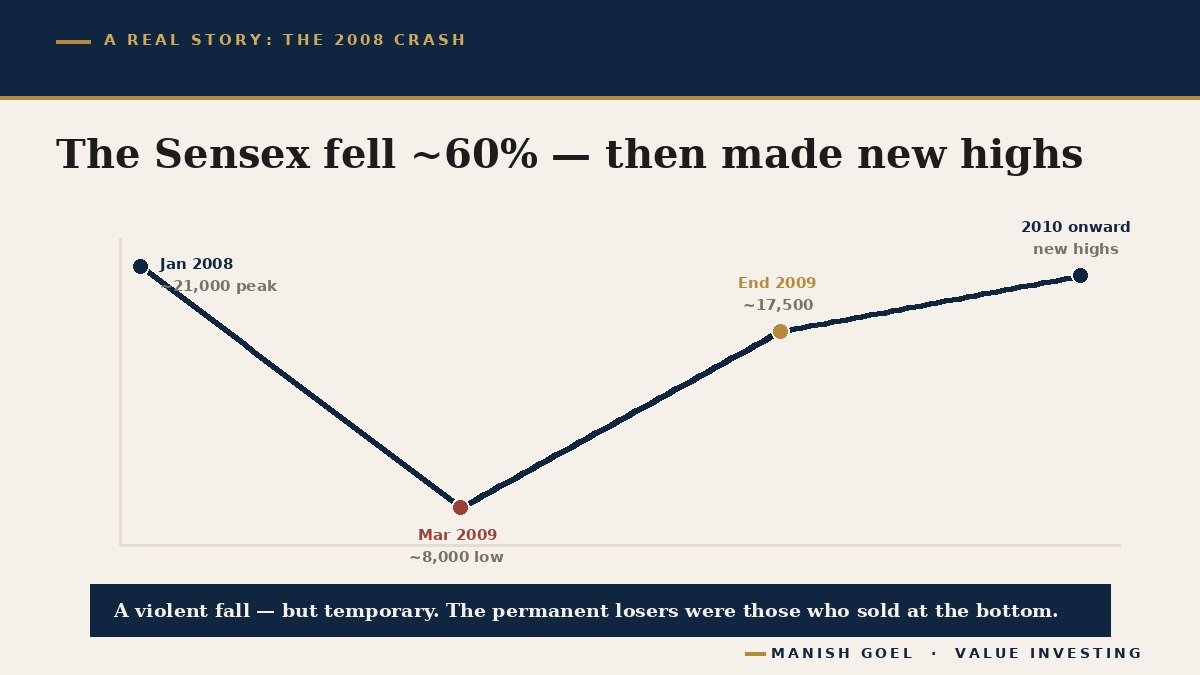

India lived through a perfect lesson in this during the global financial crisis. The Sensex (the index, or basket, that tracks 30 of India’s largest companies) had climbed to a peak of nearly 21,000 in January 2008. Then the storm hit. Over the next fourteen months it fell all the way to about 8,000 by March 2009 — a terrifying drop of around 60%. Newspapers screamed. Ordinary investors who had felt rich now felt ruined. Many sold everything near the bottom, convinced the market would never come back.

But look at what actually happened next. From that low in March 2009, the Sensex jumped about 81% before the year was even over, and by 2010 it had climbed back above 20,000 — and in the years that followed it went on to make many new all-time highs. The enormous fall, as frightening as it was, turned out to be temporary — a deep dip in the price tag, not a permanent loss of value. The people who suffered a real, permanent loss were not those who simply held on through the storm. They were the ones who were forced to sell, or who panicked and sold, at the very bottom. They converted a temporary fall into a permanent loss with their own hands.

Now compare that with a different kind of fall — the kind that never comes back. Picture a company that borrowed far more than it could ever repay, the way an airline of that era kept flying on loan after loan until it simply could not pay its lenders and finally stopped flying altogether. When a business like that collapses, its shares do not “recover.” The money is gone for good. That is a permanent loss of capital — and notice that it had nothing to do with day-to-day price wobbles. It came from a broken, over-borrowed business. The danger was in the company all along, not in the chart.

India’s own market history shows the calmer path too. The late Rakesh Jhunjhunwala, often called India’s Warren Buffett, lived through the crashes of 1992, 2000, 2008 and 2020. He did not build his fortune by fleeing every time prices fell. He backed strong businesses he understood and held them through every storm, treating the falls as temporary weather rather than permanent damage. His staying power, not a magic sense of timing, was his real edge.

How you can use this idea

Understanding that volatility is not risk is not just a clever thought — it changes how you behave when it matters most. Here are three simple habits any beginner can follow.

First, make sure you can never be a forced seller. The surest way to turn a temporary fall into a permanent loss is to be forced to sell at the worst possible moment — because you suddenly need the cash, or because you borrowed money to invest and the lender wants it back. So keep a separate emergency fund (a few months of expenses in a safe place like an FD or savings account), never invest borrowed money in shares, and only put money into the market that you will not need for at least five to seven years. When you are never forced to sell, a falling price loses most of its power to hurt you. You can simply wait for the weather to pass.

Second, judge a fall by the business, not by the screen. When a stock you own drops, ask the only question that matters: has the actual business broken, or has only the price tag moved? If sales are still strong, debt is low, cash is still flowing in, and honest managers are still running it well, then a lower price is just noise — the mandi quoting cheaper tomatoes. But if the company is drowning in loans, losing customers, or the numbers no longer make sense, that is real danger, whatever the price happens to be. Watch the business, not the wobble.

Third, protect yourself from real risk by owning quality. Since true risk is the permanent failure of a business, your best defence is to own businesses that are very hard to break: companies with low debt, steady cash profits, a durable edge over rivals, and trustworthy promoters. A strong business can survive a bad year, a recession, even a crash, and come out the other side. A weak, heavily-indebted one may not. Choosing quality does not make the price stop wobbling — but it makes the wobbles temporary instead of fatal. And notice we are not asking whether the price is cheap or dear; we are asking whether the business is built to last.

Put it all together and a calm picture appears. The restless daily price — the volatility — is mostly noise, the property dealer’s shifting quote on a flat you have no intention of selling. The real risk is something else entirely: the chance that the business itself fails, or that you are forced to sell at the bottom. You cannot control how much prices jump around, and you do not need to. You can control the two things that turn a temporary fall into a permanent loss: the quality of what you own, and whether you ever have to sell. Guard those two, and you can watch a 40% fall with a steady heart, knowing the difference between a passing storm and a sinking ship.

Key takeaways

- Volatility (how much a price jumps around in the short term) is not the same as risk; a falling price is only a temporary quote, not a real loss, unless the business fails or you sell into it.

- For a long-term investor, true risk means the permanent loss of capital — losing your money for good — which happens when a business genuinely fails or when you are forced to sell at the bottom.

- The great investors agree: Buffett says “volatility is far from synonymous with risk,” Munger calls measuring risk by volatility “nuts,” and Howard Marks says real risk is the chance of permanent loss, not fluctuation.

- The 2008 crash saw the Sensex fall about 60% and then recover to new highs — a violent but temporary dip; the only people who suffered a permanent loss were those forced or frightened into selling at the bottom.

- Protect yourself from real risk by owning quality businesses with low debt, keeping an emergency fund, never investing borrowed money, and judging every fall by the health of the business rather than the number on the screen.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.