Value Investing — Educational Series

Picture two neighbours in the same building. Both put one lakh rupees into the stock market on the same morning. The first one, Sharmaji, spends an hour reading about a simple, steady business he understands — a company that sells something people buy again and again, earns honest profits, and carries little debt. He buys a few shares of it, and then, quite calmly, he forgets about them for years. The second neighbour, young Rohit, opens a trading app and starts buying and selling Nifty options (a fast bet on which way the market index will move in the next few hours or days). His screen is green and red all day. His heart races. By night he is either thrilled or crushed.

Both of them will tell you, proudly, that they are “in the stock market.” Both call themselves investors. But they are not doing the same thing at all. In fact, they are doing two completely different things that happen to use the same screen. One of them is investing. The other is speculating. And the quiet difference between those two words is, perhaps, the single most important lesson a beginner can ever learn — because it very often decides who slowly builds wealth and who slowly loses it.

Today, let us understand that difference in the simplest possible way. By the end, you will be able to look at any decision with your own money and answer one honest question: am I investing here, or am I only speculating?

What “investing” and “speculating” really mean

The clearest definition ever written came from Benjamin Graham — the father of value investing, and the man who taught Warren Buffett himself. In his 1934 classic Security Analysis, and again in his famous 1949 book The Intelligent Investor, Graham wrote: “An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.” That one sentence is worth reading twice. Let us unpack it in plain words, because hidden inside it are three simple ideas.

First, thorough analysis (doing your homework — actually understanding the business behind the share). Second, safety of principal (your original money is reasonably protected, because you own a piece of a real, sound, profitable business rather than a wild bet). Third, an adequate return (a fair, sensible reward over time — not a dream of getting rich by Friday). If a decision has all three, Graham calls it an investment. If it is missing even one of them, he calls it speculation (betting on price moves in the hope of a quick gain, without the homework or the safety underneath).

Here is the everyday version. Imagine your uncle buys a small kirana shop (a neighbourhood grocery store). He checks its daily sales, its location, its regular customers, and the rent. He plans to run it for many years and live off its steady profit. That is investing — he owns a real business, he did his homework, and he expects a fair return over time. Now imagine your cousin bets five thousand rupees on tonight’s cricket match because he has a “strong feeling” about the result. He owns nothing afterwards. He simply wins or loses based on what happens in a few hours. That is speculation. Buying a share can be either one — it all depends on which of these two things you are really doing.

The simple test to tell them apart

You do not need a finance degree to know which one you are doing. You only need to ask yourself three honest questions. They are the quiet line between Sharmaji and Rohit.

Question one — did I do my homework? An investor can explain, in plain language, what the business does, how it earns money, and why it is likely to keep doing well. A speculator usually cannot. He bought because of a tip on WhatsApp, a hot rumour, a friend’s bragging, or simply a feeling that the price will jump. If your only reason for buying is “I think the price will go up,” that is a warning sign — you are speculating.

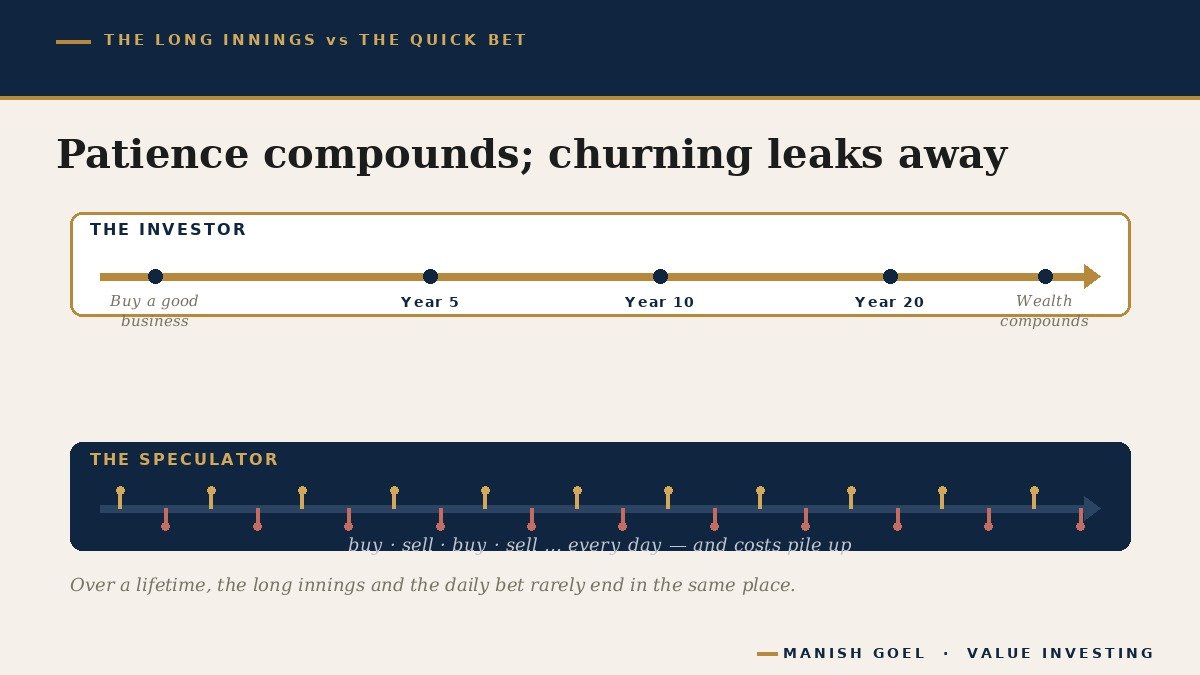

Question two — what is my time frame? An investor thinks in years, like an owner. He is happy to hold a good business through ups and downs, the way a patient batsman settles in for a long cricket innings rather than swinging wildly at every ball. A speculator thinks in hours, days, or weeks. He needs the price to move soon, or his bet does not work. Time is the investor’s friend and the speculator’s enemy.

Question three — where will my reward come from? This is the deepest question of all. Warren Buffett puts it beautifully: an investor looks at what the asset will do, while a speculator looks at what the price will do. The investor’s reward comes from the business itself growing — earning more, expanding, and sharing those profits with him over the years. The speculator’s reward can only come from one place: another person, later, agreeing to pay a higher price than he did. The investor is fed by a real, working business. The speculator is fed only by the next buyer’s mood. When that next buyer does not show up, the speculation simply collapses.

Why the difference decides who builds wealth

Why does this matter so much for your money? Because the two paths add up very differently over a lifetime. When you invest in good businesses and stay patient, the whole pie grows. The companies you own earn profits, those profits grow, and over many years your slice of a bigger and bigger pie can quietly turn into real wealth. Everyone who owns a piece can win together, because the value is being created by real work in the real world.

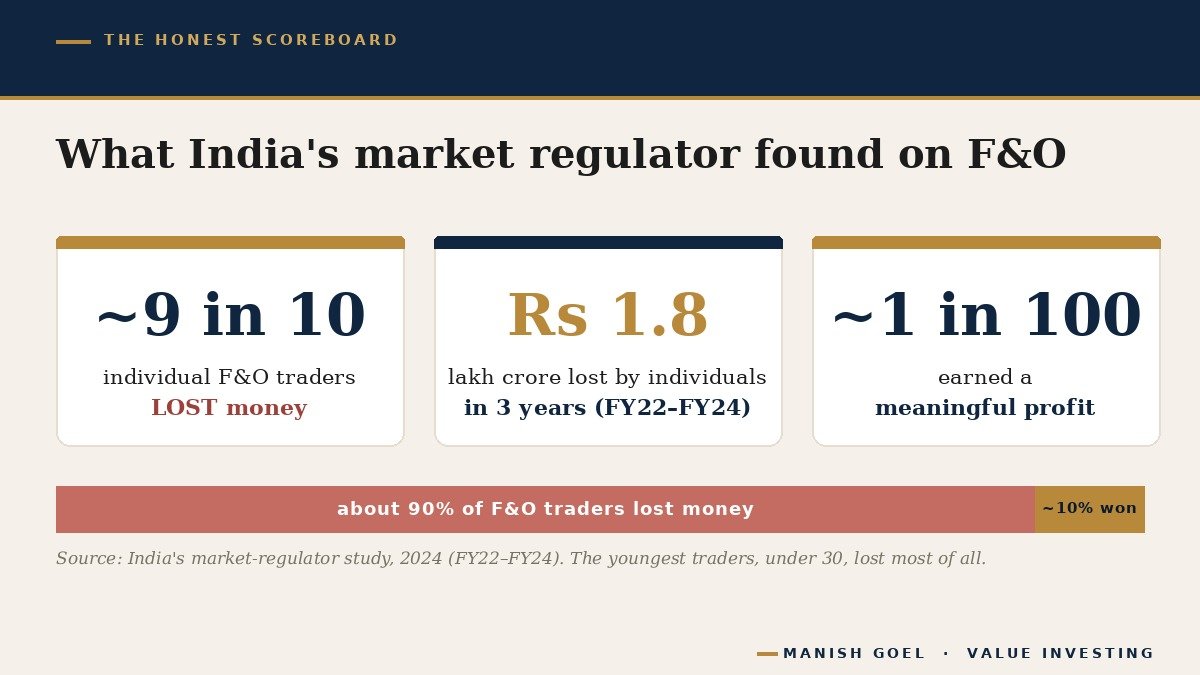

Short-term speculation is a far harder game. It is much closer to a betting ring: for every person who wins on a quick price move, someone on the other side tends to lose, and after you subtract brokerage, taxes and fees, the group as a whole usually ends up behind. And this is not just a theory. India’s own market regulator has measured it carefully. In a study released in 2024, it found that about 9 out of every 10 individual traders in the equity Futures and Options segment (a fast, leveraged form of speculation) lost money. Over the three years from FY22 to FY24, these individual traders lost more than ₹1.8 lakh crore between them. Only about one in a hundred managed to earn even a modest profit. And the youngest traders, under the age of 30, lost most often of all.

Read those numbers slowly, because they are the plain truth behind the excitement. Nine out of ten lost. This is exactly why Graham drew his line so firmly. Speculation dressed up as investing is one of the most expensive mistakes an ordinary family can make. The trader feels like a smart market player, full of action and tips and adrenaline — but the scoreboard, kept honestly by the regulator itself, shows the opposite. Slow, patient ownership of good businesses has built far more lasting wealth than fast betting on prices ever has.

A real story, and an honest word

Consider Rakesh Jhunjhunwala, the late investor whom many called India’s own Warren Buffett. He was famous on television as the “Big Bull,” and yes, he actively traded the market for income — he never hid it. But here is the part worth remembering: his lasting fortune was not built by his quick trades. It was built by investing. Around 2002 to 2003, when the watch-and-jewellery company Titan was struggling and unloved, he studied the business, believed in it, bought its shares, and then did the hardest thing of all — he simply held on. He kept holding for nearly twenty years. By the time he passed away in 2022, that single long-term holding was worth more than ₹11,000 crore. (This is shared only as a story to learn from, not as advice to buy or sell any share.)

Notice the lesson hiding in his life. The same man both traded and invested — and it was the patient investing, not the busy trading, that created the generational wealth. The trades paid some bills; the twenty-year ownership of a good business changed the family’s fortune forever. That is the quiet power of being on the right side of Graham’s line.

Now, an honest and balanced word, because Graham himself was fair about this. He did not say speculation was evil. He wrote that “outright speculation is neither illegal, immoral, nor (for most people) fattening to the pocketbook.” In other words, a little speculation, done knowingly and in small size, is a normal part of life — like buying one lottery ticket for fun. The real danger, Graham warned, is “speculating when you think you are investing.” That is the trap. It is the person who bets the family’s savings on options or hot tips while sincerely believing he is being a wise long-term investor. He has fooled himself about which game he is playing — and that self-deception, not the bet itself, is what quietly destroys wealth.

How you can use this — three simple steps

You do not have to give up the market or live in fear. You simply have to know, every single time, which game you are playing. Three plain habits are enough.

One: before you buy anything, ask the owner’s question. Pause and ask yourself honestly: “Am I buying a piece of a real business that I understand — or am I just betting that this price will go up?” If you cannot explain the business in a few simple sentences to a family member, you are probably speculating. There is no shame in stepping back until you can. This one question, asked calmly before every purchase, will protect you more than any tip ever could.

Two: if you must speculate, keep it tiny and separate. Graham’s rule for any speculation was wise and simple: never risk more than you can comfortably afford to lose, and treat it as a pastime, not as your plan for the future. Keep your serious, long-term money — your children’s education, your retirement, your safety — completely away from the fast betting. Never let a small bit of fun quietly grow into a gamble with money you truly need.

Three: do your homework, then give it time. Real investing is wonderfully boring. You find a sound, well-run business that you understand, you make sure it is not drowning in debt, and then you let the years do the heavy lifting — the way a tree planted today gives its best shade many summers later. Action, excitement and constant buying-and-selling feel productive, but in investing they are usually the enemy. Patience, not adrenaline, is what fills the account.

Key takeaways

- Investing and speculating use the same screen but are two different games. Benjamin Graham defined an investment as something that, after thorough homework, offers reasonable safety and a fair return; anything else is speculation.

- A simple test: did you do your homework, are you thinking in years (not hours), and will your reward come from the business growing — or only from someone later paying a higher price?

- The scoreboard is real. India’s market regulator found that about 9 in 10 individual F&O traders in India lost money, losing more than ₹1.8 lakh crore over three years — speculation feels exciting but rarely builds wealth.

- Even Rakesh Jhunjhunwala, famous as a trader, built his lasting fortune by investing — patiently holding a good business for nearly twenty years, not by quick bets.

- The biggest danger, Graham warned, is “speculating when you think you are investing.” Know which game you are playing, keep any speculation tiny and separate, and give real investments time.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.