In 1991, on stage at the University of Notre Dame, Warren Buffett offered a single thought experiment that, if taken seriously, would have saved Indian retail investors from roughly ₹1.8 lakh crore of F&O losses, several thousand small-cap blow-ups, and an entire decade of churning their own portfolios into the ground. Imagine, he said, that you started life with a punch card containing only twenty slots. Each time you bought a stock, you punched a hole. Once the twenty holes were used up, you were finished — no more buying, ever, for the rest of your life.

I have been an Indian markets investor for over two decades. I can tell you, hand on heart, that this single mental model — what I call the Twenty-Punch-Card Rule — has done more for my returns than any spreadsheet, any DCF, any factor model I have ever built. It is also the principle most violated by Indian retail investors, which is precisely why it remains so powerful.

The Card Is a Metaphor for Lifetime Scarcity

Notice what the rule does not say. It does not say “buy fewer stocks per year” — that is the cousin idea, the Fat Pitch Principle, where you wait for one good pitch out of many. The Twenty-Punch-Card is the parent of that idea, and it goes further. It says: across your entire investing life, you will make twenty real decisions. Twenty. Not twenty per year. Twenty in seventy years.

The arithmetic is brutal. If you begin at age twenty and live to ninety, that is one buy decision every three and a half years. Most Indian retail accounts now turn over their entire portfolio in less than nine months. They have already, mathematically, spent their entire lifetime allocation in a single financial year — and they did it before they understood the second balance sheet they bought.

The rule forces three behaviours that no other discipline forces simultaneously. First, ferocious pre-purchase research, because each punch is irreplaceable. Second, long holding periods, because you cannot afford to use a punch on something you intend to flip in three months. Third, position concentration, because if you only get twenty buys in a lifetime, each one must be sized to matter. Selectivity, patience, and conviction — the entire Buffett trinity — fall out of one constraint.

Buffett’s Own Punch Card

Look at how Buffett actually lives this. American Express in 1964, the salad-oil scandal year — one punch, forty per cent of the partnership goes in. Coca-Cola in 1988 — one punch, held for thirty-eight years and counting. See’s Candies in 1972 — one punch, never sold. Apple in 2016 — one punch, now Berkshire’s largest holding by far. Across a sixty-year career, the meaningful Berkshire purchases that drove the bulk of returns number well under twenty. He is not a hypothetical user of the rule. He is the empirical proof.

The Indian application is even more uncomfortable. Look at the multibaggers of the 2014-2024 decade — Bajaj Finance, Page Industries, Asian Paints, Pidilite, Nestle India, HDFC Bank, Titan Company, Eicher Motors. Almost every household name. The investor who, in 2014, used six punches on six of these and then literally lost the punch card for ten years, would have outperformed ninety-five per cent of professional fund managers in this country. Doing nothing, by design, has been the highest-IQ Indian strategy of the last decade. The Twenty-Punch-Card simply formalises that observation.

Why does it work? Because it inverts the default Indian retail wiring. Default wiring says: when in doubt, transact. Punch-card wiring says: when in doubt, do nothing. Default wiring says: an idea sitting in your head must be acted upon today. Punch-card wiring says: an idea sitting in your head is fine — it can sit there for two more years while you watch the business compound or stumble. Default wiring says: a missed opportunity is a loss. Punch-card wiring says: a missed opportunity costs nothing. A bad punch costs you a slot you can never get back.

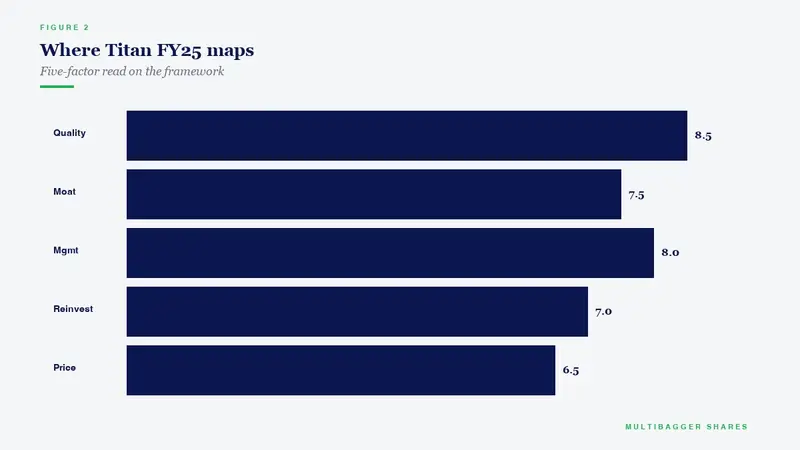

How Titan Biotech’s FY25 Numbers Reward the Investor Who Saves the Punches

The Twenty-Punch-Card discipline is not abstract philosophy — it is a filter. The investor with twenty lifetime punches looks at a candidate business and asks one brutal question: would I be comfortable holding this on my card for the next twenty years? Titan Biotech (BSE: 524717) is interesting precisely because its FY25 audited numbers read like a checklist for that question.

Start with the balance sheet, because that is where punches get destroyed. Titan Biotech ended FY25 with total borrowings of approximately ₹3 crore against a strong net worth — a debt-to-equity ratio of roughly 0.02x. The company runs a net cash position with around ₹38 crore of investments and cash equivalents accumulated from internal accruals. A punch-card investor cares about this because leverage is the single most common reason a multi-decade compounder turns into a zero. Titan’s balance sheet has, for now, removed that risk from the equation.

Next, profitability discipline. FY25 EBITDA margin sat in the ~18-22 per cent operating-profitability band. Return on capital employed printed at approximately 16.9 per cent, and return on equity in a similar zone — both comfortably above the ~12-14 per cent cost-of-capital floor most Indian SMEs cannot clear consistently. A Twenty-Punch-Card investor wants businesses that earn more on each rupee of capital than the rupee costs to raise. Titan’s FY25 numbers clear that bar.

Cash conversion is the third filter, and arguably the cruellest. Many Indian small-caps print profits but never collect them. Titan’s FY25 cash flow from operations came in at roughly 103 per cent of operating profit — meaning every reported rupee of profit was backed by an actual rupee of bank-deposit cash. A 261-day cash conversion cycle is funded entirely by internal float, with zero working-capital borrowing. This is the audited, signed-off-by-statutory-auditors version of “the earnings are real.”

Then management alignment. Promoter holding sits at approximately 55.87 per cent in FY25, having moved up from 48 per cent over the past several years through open-market purchases. Promoter pledging is zero. Director compensation totalled around ₹4.56 crore against the company’s profitability base — comfortably inside the corporate-governance smell test. An unbroken fourteen-year dividend track record and a conservative depreciation policy on the ~₹57 crore gross block round out a picture of patient, owner-mindset capital allocation. Twenty-Punch-Card investors want to hold the same shares the promoter is accumulating. Titan’s FY25 disclosures show that alignment.

Finally, the geographic and operational moat. FY25 export revenue at approximately 34.5 per cent of total, served across roughly 100 countries, with ~467 employees generating approximately ₹33 lakh of revenue per head — these are the operational signatures of a business that has earned the right to be considered for a punch. The Twenty-Punch-Card discipline asks for candidate businesses where the audited numbers, today, reward patience rather than punishing it. Titan’s FY25 file does that.

The Takeaway

The hardest part of Indian investing is not finding good ideas. The Indian market produces dozens of genuine compounders every decade. The hard part is restraining yourself from punching a new hole every time CNBC, a Telegram tip, or your brother-in-law mentions a stock name. The Twenty-Punch-Card Rule is a violence-of-scarcity tool. It does not ask you to be smarter than anyone else. It asks you to act as if punches were finite — because, in any honest accounting of your life, they should be.

If you implement exactly one change in your investing life after reading this article, let it be this: count your punches for the next twelve months. Every fresh stock purchase is one punch. If you cross five, you are running at a 175-stock-lifetime pace, which is roughly eight times Buffett’s recommended rationing. That single number, tracked monthly, does more to fix Indian retail behaviour than any technical chart ever has.

The card in your hand has twenty slots. Most of them are still empty. Treat them like that.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.