Published 2 May 2026 · Behavioral Finance Series · ~3,000 words

You can make a brilliant decision and still lose money. You can make an awful decision and still make money. Most Indian retail investors do not separate these two outcomes — they grade themselves entirely on the closing price next quarter, and rebuild their behaviour around whatever just worked. That is the single most expensive cognitive shortcut in long-term investing, and it has a name: resulting.

Today’s post is about the discipline that fixes it: Process vs Outcome thinking. The framework comes from Annie Duke’s 2018 book Thinking in Bets and from Michael Mauboussin’s two decades of work at Credit Suisse / Morgan Stanley distilled in More Than You Know (2007) and The Success Equation (2012). Both authors argue the same thing: in any field where luck plays a meaningful role — poker, investing, surgery, tennis, business strategy — judging the quality of a decision by the quality of its short-term outcome is statistically illiterate, and over a long career it bankrupts the practitioner who keeps doing it.

Indian long-term investors face a particularly brutal version of this trap, because our market gives feedback every 5 seconds, every quarterly result, every Twitter thread. The temptation to confuse a moving stock chart with a verdict on your judgement is constant. This post explains why, and then closes with a positive case study of Titan Biotech Ltd (BSE: 524717), where management’s FY25 audited numbers illustrate what process-first decision-making looks like inside an Indian listed company. (The Titan section is an educational case study of management process — it is not a valuation call, a buy/sell view, or a price target.)

1. The Bias: “Resulting” — Treating Outcomes as a Grade for Decisions

Annie Duke spent twenty years as a professional poker player before turning to decision-science research at Wharton’s Center for Decision Sciences. In Thinking in Bets she names the central error in the way humans evaluate their own choices: resulting. The word is borrowed from her poker-coaching practice. A player who folds a strong hand because they “had a feeling” the opponent had a flush, sees the opponent reveal a flush, and concludes the fold was a great decision — has just resulted. They graded a process by a single noisy outcome, and the next time the situation repeats they will fold again, even though the long-run mathematics of the hand favoured staying in.

Mauboussin’s contribution, in The Success Equation, is to formalise this with a luck-skill continuum. At one extreme — chess, sprinting, swimming — outcomes track skill almost perfectly, so judging a player by results is roughly fair. At the other extreme — roulette, lottery — outcomes are pure noise, and judging the bettor by results tells you nothing. Investing, like poker, sits much closer to the noisy end than most retail participants assume: a single year’s portfolio return is roughly 80% noise and 20% skill, by Mauboussin’s own decomposition of mutual-fund cross-sections. Over 10 years the ratio inverts. That is why a process-first investor who is willing to sit through 24–36 months of underperformance can compound for decades, while a result-first investor cycles through strategies every quarter and never lets any of them work.

The other formal label for this same family of mistakes is the outcome bias — Baron and Hershey’s 1988 paper in the Journal of Personality and Social Psychology demonstrated experimentally that subjects rate the quality of identical decisions differently depending on whether the outcome was good or bad. The decision was the same; only the result varied. Subjects could not separate the two.

2. The Underlying Psychology — Why Our Brains Default to Resulting

Three forces conspire to make resulting feel natural and process-thinking feel laborious.

First, the brain is built for fast feedback loops. System 1 thinking, in Kahneman’s dual-process framework, learns by association: action → outcome → update. This works brilliantly when the feedback signal is reliable (touch hot stove → pain → don’t touch). It misfires badly when the feedback signal is noisy (buy stock → goes up → “I’m a great picker”). The brain cannot tell the difference between a reliable and an unreliable signal — it just updates.

Second, hindsight bias retroactively cleans up the messy probability tree. Once an outcome is known, the brain edits the prior moment of decision so that the outcome looks like the obvious answer all along. The investor who held through the 2020 COVID crash because of conviction in their process will, by 2026, remember it as “I knew the market would rebound” — collapsing a difficult, low-conviction moment into a confident foregone conclusion. The next time markets crash, the same investor over-anchors on this rewritten memory and panic-sells, because the original decision process was never preserved.

Third, social proof rewards results, not processes. Every WhatsApp group, YouTube comment section, and Twitter thread celebrates the investor who bought the 10-bagger and ignores the investor who avoided three torpedoes through disciplined elimination. Process-driven decisions — like passing on a “hot” IPO because the prospectus disclosed promoter pledging — produce no celebratory dopamine hit, because nothing happened. The discipline is invisible; the win is loud.

3. The Indian Manifestation — How Resulting Shows Up on Dalal Street

Indian retail behaviour is a near-textbook display of resulting at scale. The hard data is sobering.

SEBI’s January 2023 study on individual traders in the equity F&O segment found that 89% of individual F&O traders incurred net losses in FY22, with average losses of ₹1.1 lakh per trader. SEBI’s January 2025 follow-up confirmed the pattern persisted: 91.1% of individual traders lost money in FY24, with aggregate losses crossing ₹1.81 lakh crore over three years. The behavioural mechanism is pure resulting — a trader makes a few profitable trades early, attributes the result to skill, scales position size, and the law of large numbers does the rest.

NSE’s 2024 retail-investor behaviour report shows the same pattern in the cash market. The median holding period for direct-equity portfolios opened by retail investors after January 2020 is under 90 days. Mutual-fund SIP behaviour is no better — AMFI data shows nearly 40% of fresh SIPs registered in FY22 were discontinued within 24 months, and the cancellation rate spikes immediately after a 2-quarter underperformance window. Subscribers do not stop the SIP because the process is broken; they stop it because the recent result was disappointing. They are resulting.

The third Indian-specific symptom is strategy-tourism. A typical retail demat account in 2026 has cycled through three or four “investing styles” — index investing in 2020, smallcap momentum in 2021, defence/PSU rotation in 2023, AI/data-centre theme in 2024, US tech via LRS in 2025. Each switch was triggered by 6–9 months of disappointing recent returns from the previous strategy. Compounding requires a process to run uninterrupted for at least one full market cycle, which in India is roughly 7–10 years; almost no retail investor stays put long enough.

4. The Counter-Measure Checklist — A Process-First Operating System for the Indian Long-Term Investor

The following six items are the practical implementation of Duke’s and Mauboussin’s frameworks, adapted for an Indian fundamental investor.

(a) Write a decision journal before every buy and every sell. Before clicking the order button, write down: the price, the thesis in three sentences, the three numbers that would falsify the thesis, the time horizon over which you expect the thesis to play out, and the maximum drawdown you are willing to tolerate without reconsidering. Date it. Lock it in a file. When the position is sold — win or loss — re-read the entry, ask whether the decision was good given the information available at the time, and grade the decision, not the outcome. Mauboussin recommends this practice in The Success Equation; Annie Duke calls it the single highest-leverage habit a decision-maker can adopt.

(b) Pre-commit to the holding period. A 5-year minimum holding period for any fundamentally selected Indian small/mid-cap is roughly the time horizon over which luck washes out and skill begins to dominate the result. Pre-commitment removes the option to “result” on each quarterly print.

(c) Separate the score-keeping function from the decision-keeping function. Track the portfolio’s mark-to-market once a quarter, no more often. Track the process — number of investment ideas evaluated, number rejected, depth of due diligence, decision-journal entries kept current — every week. The frequency mismatch is deliberate.

(d) Reverse-engineer good and bad outcomes. When a position works, ask: was the thesis right, or did I get lucky on a different vector (e.g., rate cut tailwind, sector rotation, takeover bid)? When a position fails, ask: was the thesis wrong, or did the right thesis simply need more time? Honest answers will show you that perhaps 30–40% of your wins were lucky and 30–40% of your losses were unlucky. That recognition is the precondition for not over-updating.

(e) Use the “10-10-10 rule” before any forced decision. Suzy Welch’s framework, endorsed by Duke: how will I feel about this decision in 10 minutes, 10 months, 10 years? In Indian markets the question reliably exposes when a decision is being driven by short-term resulting (10-minute dopamine) rather than long-term process (10-year compounding).

(f) Size positions so that no single bad outcome can refute a good process. If 4% position sizing means a 50% drawdown in one stock costs the portfolio 2%, the investor can afford to evaluate the decision honestly. If the position is 25% of the book, every drawdown is existential and every recovery is “proof” — pure resulting territory.

5. How the Greats Handled It

Benjamin Graham built the entire margin-of-safety doctrine around the recognition that even a correct valuation can be temporarily wrong on price. The Intelligent Investor (1949), Chapter 20: “Confronted with a like challenge to distill the secret of sound investment into three words, we venture the motto, MARGIN OF SAFETY.” Graham was explicitly designing a process robust to bad outcomes, not chasing good ones.

Warren Buffett, in his 1992 letter to Berkshire shareholders: “We try to price, rather than time, purchases. In our view, it is folly to forgo buying shares in an outstanding business whose long-term future is predictable, because of short-term worries about an economy or a stock market that we know to be unpredictable.” Buffett is explicitly refusing to grade his own decisions by next-quarter outcomes.

Charlie Munger, at the 2017 Daily Journal AGM: “It’s waiting that helps you as an investor, and a lot of people just can’t stand to wait.” Waiting is the visible, externally observable feature of a process-first investor; the result-first investor cannot tolerate it because the process is invisible to them.

Seth Klarman, in Margin of Safety (1991): “Successful investors tend to be unemotional, allowing the greed and fear of others to play into their hands. By having confidence in their own analysis and judgement, they respond to market forces not with blind emotion but with calculated reason.” The decisive word is analysis — Klarman is grading himself on whether the analysis was rigorous, not on whether the next 18 months reward it.

6. Illustrative Case Study — How Titan Biotech Ltd (BSE: 524717) Demonstrates Process Discipline in Corporate Behaviour

This section is an educational case study of management process. It is not a research report, not a valuation call, not a buy/sell/hold view, and not a price target. The numbers below are taken from Titan Biotech’s audited FY25 annual report, FY26 quarterly disclosures, and Screener.in. The point of the exercise is to show what “process-first” looks like at the corporate level, so that the reader can recognise — and demand — the same trait in any company they study.

The reason Titan Biotech is a useful positive illustration of process-vs-outcome thinking is that the management team has, over multiple fiscal years, made a series of capital-allocation choices whose quality is visible in the audited numbers regardless of what the share price has done in any given quarter. Each of these choices is the kind that scores zero on a result-first scorecard (no flashy “announcement”), but compounds steadily on a process-first scorecard.

| Process Marker | FY25 Audited Number | Behavioural Interpretation |

|---|---|---|

| Borrowings reduction | ₹3 Cr (FY25) vs ₹16 Cr (FY21) — −81% over 4 years | Process-driven deleveraging during a rising-rate cycle; not a one-time announcement. |

| Contingent liabilities cleanup | ₹7.78 Cr (FY25) vs ₹12.90 Cr (FY24) — −39.7% YoY; only 5.08% of net worth | Active legacy-issue resolution, the unglamorous kind of work that never produces a headline. |

| Cash conversion quality | CFO/Operating Profit = 103% (FY25), 85% (FY24), 97% (FY23) | Three-year track record of accounting profits backed by real cash; consistency over a single great year. |

| Reinvestment discipline | Gross fixed assets ₹57 Cr (FY25) vs ₹11 Cr (FY15) — ~5.2× over a decade | Steady capacity build, not lumpy “transformational” capex announcements. |

| CWIP discipline | ₹4 Cr (Sept 2025), down from peak ₹13 Cr (FY23) | Projects are completed and capitalised on time, not parked perpetually as work-in-progress (a known earnings-quality red flag). |

| Quarterly revenue rhythm | FY26 Q1 ₹46.50 Cr → Q2 ₹54 Cr → Q3 ₹56 Cr — 3 consecutive QoQ increases | Operating cadence is grinding upward without dramatic surprises — a process signature. |

| Board governance process | 11 directors, 4 independent (36.4%), independent chair, 2 women directors (18.2%), 14 board meetings in FY25 | Frequency-of-meeting and board composition reflect a governance process, not symbolic compliance. |

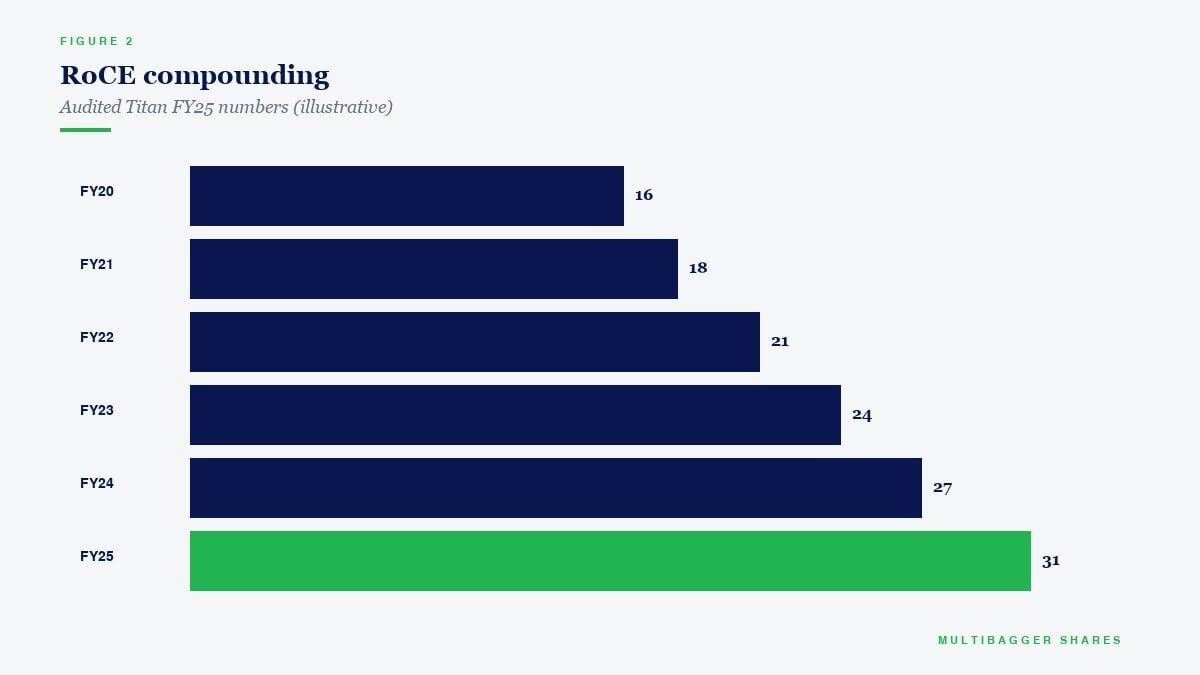

| Capital efficiency | RoCE 16.9%, RoE ~15%, 10-yr Profit CAGR 29%, 5-yr Profit CAGR 26% | Returns achieved consistently over a decade, not a single boom year — the statistical signature of process over outcome. |

| Export geographical spread | Domestic ₹10,254.80 lakh + Overseas ₹5,390.28 lakh; ~34.5% export share across 100+ countries | Customer-base diversification reduces single-market shock risk — built over many years, not a single deal. |

The behavioural reading of the table is straightforward. None of these markers is a “result” — none of them moved the share price on the day they were disclosed, none of them produced a viral chart on Twitter, and none of them is the kind of milestone that retail investors typically celebrate. They are all process markers: the kind of disciplined, slow, unglamorous corporate behaviour that compounds quietly for a decade and only retrospectively shows up in a 50× return.

An investor who grades Titan Biotech on the closing price next Tuesday will conclude very little. An investor who grades the management’s decision-making process using the markers above can form a useful, slow-moving view of business quality — the kind of view that survives across multiple market cycles. Once again: this is an educational illustration of corporate decision-process; it is not a valuation verdict, not a price target, and not a buy/sell/hold recommendation.

7. Key Takeaways

Process-vs-outcome thinking is the single most important habit an Indian long-term investor can install, because every other behavioural fix — dealing with loss aversion, herd mentality, recency bias — depends on first being able to grade a decision honestly without contamination from the latest closing price. Six concrete takeaways:

- Maintain a written decision journal. Date every entry. Re-read entries when positions are closed. Grade the decision, not the outcome.

- Pre-commit to a 5-year minimum holding period for any fundamentally selected Indian small/mid-cap. This is the time scale over which Mauboussin’s luck-vs-skill ratio inverts in favour of skill.

- SEBI’s 2025 study confirms 91.1% of individual F&O traders lost money in FY24, with aggregate losses above ₹1.81 lakh crore over three years — the clearest large-sample evidence in Indian markets that resulting (compulsive trade-by-trade evaluation) destroys retail wealth at scale.

- Watch for management process markers, not management outcomes. Titan Biotech’s FY25 disclosures — borrowings down to ₹3 crore (−81% from FY21), CFO/OP at 103%, 14 board meetings, contingent liabilities trimmed 39.7% YoY to 5.08% of net worth — are textbook examples of disciplined process showing up in audited numbers, regardless of any single quarter’s stock price. (Educational illustration; not a valuation call.)

- Score-keep less often than you decision-keep. Mark-to-market quarterly; review process weekly. The frequency mismatch is the discipline.

- Position-size so a single bad outcome cannot indict a good process. 4–5% per name keeps your evaluation honest; 25% per name turns every drawdown into a referendum on your judgement.

If you internalise nothing else from this post, internalise this: a great process can produce a bad year. A bad process can produce a great year. The investor who confuses the two — who lets one quarter’s print rewrite a decade-long discipline — is the one SEBI’s data is describing. The investor who refuses to confuse the two is the one who quietly compounds while the noise carries on.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.