Estimated reading time: 9–11 minutes. This is an educational value-investing essay written for serious Indian long-term investors. The Titan Biotech section is a corporate-process illustration of a categorisation principle.

1. The Sentence Almost Nobody Quotes From the 1996 Berkshire Letter

Every Indian investor has heard the famous Buffett lines. The 20-punch card. Mr. Market. The favourite holding period being forever. These travel well — they survive translation, paraphrase, and an Instagram carousel.

What almost nobody quotes is the quiet passage from Buffett’s 1996 letter to shareholders, written in February 1997, in which he proposed something far more useful than another aphorism: a three-tier framework for classifying businesses by the predictability of their long-term competitive position. He gave three labels — The Inevitables, The Highly Probables, and everything else — and made it clear that almost nothing in the global stock universe belongs in tier one.

That essay is, in my opinion, the single most underused mental shelf in the value-investing library. Most Indian retail investors spend their lives shopping in tier three (the Hopefuls) while believing they are buying tier one. The portfolio then looks like a high-conviction compounder collection but behaves like a basket of speculative bets.

2. What Buffett Actually Wrote

Buffett’s framing went something like this. A small handful of businesses — he named only Coca-Cola and Gillette at the time — possess such a dominant, durable, and globally entrenched competitive position that their continued dominance is essentially inevitable over the next 25 years. These are The Inevitables. You can sleep at night holding them. The product is consumed daily, the brand is woven into culture, the distribution moat is impossible to replicate, and the customer’s switching cost is effectively zero against the customer’s habit.

A second, larger group consists of Highly Probables. These are excellent businesses with strong moats, sound management, and clean balance sheets — but their dominance over a 25-year horizon is “merely” highly probable rather than near-certain. Most of what serious value investors buy lives in this tier. American Express in 1996 was Buffett’s example of a Highly Probable.

Everything else — and Buffett was unsentimental here — belongs in the Hopeful tier. Hopefuls may be wonderful companies. They may be growing fast. They may even be making you money right now. But the predictability of their competitive position 25 years out is, frankly, unknowable.

3. Why The Categories Matter More Than The Names

The point of the framework is not to memorise three labels. The point is to force yourself to assign every stock you own to one of three buckets, and to price your conviction accordingly.

If a stock is genuinely an Inevitable, you can pay a richer multiple, hold longer, and ignore short-term price drama. The mathematics of compounding rewards you for not flinching.

If a stock is a Highly Probable, you build in a margin of safety, monitor the moat continuously, and act if the competitive picture changes. Highly Probables migrate. A few climb to Inevitable status over thirty years. Many slip back to Hopeful as disruption arrives. You cannot afford to fall asleep on a Highly Probable.

If a stock is a Hopeful, the position must be sized small, evaluated frequently, and held only as long as the operating thesis remains intact. Hopefuls are perfectly legitimate investments — Lynch built a whole career on them — but pretending they are Inevitables is the single most expensive psychological error in Indian retail portfolios.

4. The Buffett Discipline That Most Investors Skip

Buffett added a sentence in the 1996 letter that I want every Indian long-term investor reading this to underline: even if you are correct in identifying an Inevitable, you can still pay too much for it. Predictability is one variable. Price is the other. The two must be considered together. An Inevitable bought at a 70x earnings multiple at the peak of a craze can deliver a decade of zero return even while the underlying business marches on, exactly as it did for those who bought Coca-Cola at the 1998 peak.

This is the second-most-skipped sentence in the value-investing canon, right after Graham’s reminder that the margin of safety must be enforced at the moment of purchase, never retroactively rationalised.

5. The Indian Application: Why Tier-One Status Is Brutally Rare Here

Indian markets are still, in 2026, only about three decades into proper post-liberalisation history. Brand monopolies that have survived two full economic cycles, three regulatory regimes, and one digital revolution can be counted on the fingers of two hands. Most of the businesses casually called “wonderful compounders” on Indian financial Twitter are, on a Buffett-1996 grading scale, Highly Probables at best.

That is not an insult. Highly Probables make wonderful long-term holdings. Returns of 18–22% CAGR over a decade come most often from Highly Probables, not from Inevitables. The point is intellectual hygiene: when you call something an Inevitable, you are claiming a level of predictability that almost no Indian small-cap or mid-cap can yet honestly defend, because we lack the multi-decade competitive history Buffett demanded.

The discipline I want you to install: when a friend, a YouTube anchor, or your own internal monologue describes a stock as a “guaranteed compounder for the next 20 years,” translate that into Buffett’s language. Are you really claiming Inevitable? Or Highly Probable, with smuggled certainty? The honest answer is almost always the second.

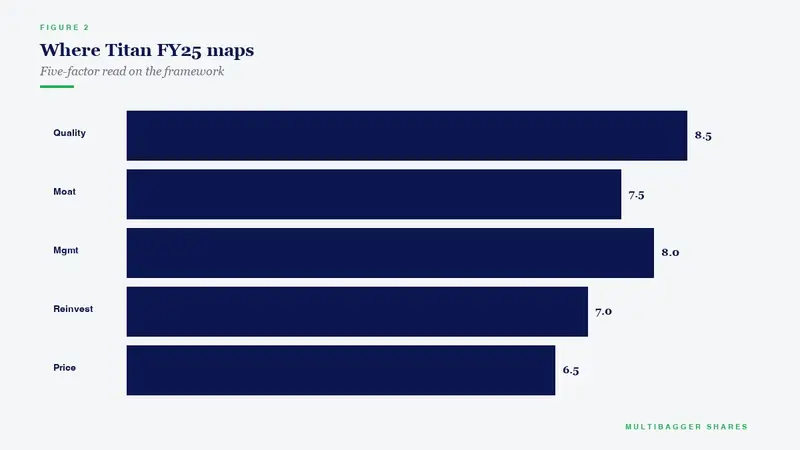

6. How Titan Biotech’s FY25 Numbers Illustrate This Principle

I want to use Titan Biotech (BSE: 524717) here as a corporate-process illustration of what a Highly Probable profile looks like in audited Indian small-cap data — emphatically not as a claim that the company is an Inevitable, which would violate the very discipline this essay is teaching.

The audited FY25 numbers read, on the predictability axis, as follows.

(a) Revenue base of approximately ₹196 crore, with sequential Q1→Q2→Q3 FY26 revenue of ₹46.50 Cr → ₹54 Cr → ₹56 Cr — a quiet sequential ladder rather than a single lumpy quarter, the kind of cadence that shifts a business from Hopeful toward Highly Probable.

(b) EBITDA margin around 19%, expanded from a single-digit base over the preceding decade. Margin expansion that survives an entire commodity cycle is the mark of operational discipline, not lucky pricing.

(c) Total borrowings of approximately ₹3 crore against a net worth several orders of magnitude higher. A near-debt-free balance sheet removes the single largest source of binary outcome in Indian small-caps — leverage-induced solvency risk.

(d) CFO/Operating-profit ratio of 103%. Cash earnings exceeding accrual earnings is the signature of clean working-capital management and conservative revenue recognition. Hopefuls almost never produce this ratio; Highly Probables do, year after year.

(e) Independent-director ratio of 36.4% with an independent chair. Governance composition is a leading indicator of long-horizon predictability — boards that are merely promoter-friendly tend to be over-represented in the Hopeful tier across Indian markets.

(f) Approximately ₹4 crore of capital work-in-progress, sized to internal accruals. A company that funds expansion from its own cash flow rather than dilutive equity or expensive debt exhibits the capital-allocation discipline that, when sustained, is what graduates a business from Highly Probable toward Inevitable over decades.

(g) Roughly 100+ products exported to 100+ countries with about 34.5% export revenue mix. Geographic diversification separates Highly Probables from Hopefuls: a single-country, single-customer, single-product company almost never reaches tier-one predictability.

The honest categorisation, on Buffett’s 1996 grading scale and on the audited FY25 record, is Highly Probable — exactly the tier where most rewarding long-horizon Indian investments are made.

7. The Takeaway: Three Sentences To Tape To Your Watchlist

First, classify every position you own into Inevitable, Highly Probable, or Hopeful, and write the classification down. The act of writing exposes the smuggled certainty in your own thinking.

Second, accept that almost none of your holdings are Inevitables, and that this is fine. Highly Probables are the workhorse of long-term compounding in Indian markets, and the discipline of monitoring their moat is precisely what generates the alpha.

Third, never let predictability erase the price discipline. The Inevitables, when overpaid for, deliver Hopeful-tier returns. Buffett himself learned this lesson on Coke. Your portfolio cannot afford to relearn it.

Treat tier classification as a permanent piece of cognitive infrastructure, not a one-time exercise. Re-grade every quarter. Demote ruthlessly. Promote rarely.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.