One of the most useful sentences ever written about equity investing is buried in a 1977 Fortune essay titled “How Inflation Swindles the Equity Investor”. Warren Buffett, then 47, made an argument almost no Indian retail investor has internalised half a century later: a share of stock is, in economic substance, a disguised bond. The coupon happens to vary, but it is a coupon all the same.

That single reframing — viewing every share certificate as a variable-coupon, perpetual instrument rather than as a lottery ticket — is what separates long-term compounders from screen-watchers on Dalal Street. It is not a metric. It is a mental discipline. And once you absorb it, every other value-investing tool — earnings yield, owner earnings, ROE, retention ratio, payout — slots into one coherent picture.

Today’s post unpacks that 1977 framework, why it still travels well to the Indian market in 2026, and how the audited FY25 numbers of Titan Biotech Limited (BSE: 524717) illustrate what an “equity bond” with disciplined economics actually looks like on the page.

The Buffett Reframing: A Stock Is a Bond With a Floating Coupon

Bonds are simple. You pay a price today, you receive a fixed coupon every year, and at maturity you get your principal back. The yield to maturity is the discount rate equating those cash flows with today’s price.

Buffett’s 1977 insight was that equities are structurally identical — only the coupon is not fixed by contract. It is set every year by the underlying business through its earnings, and by management’s decision to either pay it out as dividend or retain it to grow next year’s coupon. There is no maturity date, so the instrument is perpetual. The “principal” is the per-share equity value, which accretes when retained earnings are reinvested at a positive return on equity.

From that single substitution, three numbers appear that any Indian investor can compute in thirty seconds for any listed business:

Initial coupon = EPS ÷ Market price = the inverse of the P/E. At P/E 20, the coupon is 5%. At 12.5, it is 8%. At 50, just 2%.

Coupon growth rate = Return on equity × Retention ratio. A business earning 20% on retained equity and reinvesting 70% grows its coupon at roughly 14% per year — provided each incremental rupee continues to earn 20%.

Sustainable long-term return ≈ Initial coupon + Coupon growth, assuming the multiple does not collapse and the business does not decay. This is Buffett’s “first principles” return: the rupees that actually accrue to you as a part-owner, before any speculation about whether Mr. Market will hand you a higher P/E next year.

Notice what this framing does. It strips out two illusions that haunt retail investors: that next-quarter earnings surprises matter (they do not, for a ten-year holding) and that P/E multiples are an independent variable to predict (they are a residual the market hands you, and over very long horizons they wash out, leaving the coupon and coupon growth as the dominant drivers of return).

Why the 1977 Argument Still Bites in India in 2026

Buffett’s 1977 essay was provocative because the conventional wisdom held that equities were the natural “inflation hedge”. His counter-argument was unsentimental: most businesses cannot keep ROE rising as nominal interest rates rise, so the “equity coupon” of an average company stays stuck around 12% for very long stretches, regardless of whether bond yields are at 4% or 14%.

Translate that to India in 2026. The 10-year G-sec is in the high-6% range. A representative Nifty 50 P/E sits around 22, implying an equity coupon of roughly 4.5% — apparently less than risk-free debt. The bond-equivalence framing tells you why long-term investors still buy: the second number, the coupon growth rate, does the heavy lifting. A high-quality Indian business retaining most of its earnings at 18–25% incremental ROE compounds the coupon at double-digit nominal rates. The framework also forces scepticism toward richly priced “growth stories” — a stock at P/E 80 has a 1.25% starting coupon; to beat a plain G-sec by a meaningful margin the coupon must grow ~20% forever, a heroic ask of any business.

The Three Levers Every Long-Term Investor Should Track

Lever 1 — Starting coupon (E/P). Set by the price you pay. Pay a P/E of 50 and the starting coupon is locked at 2%. This is the lever the value investor controls by being patient and only swinging at the fat pitches.

Lever 2 — Reinvestment ROE. The marginal return earned on every retained rupee determines how fast the coupon grows. A business that pretends to grow but does so by issuing equity, taking on leverage, or making acquisitions at high multiples is silently lowering its incremental ROE. The forensic discipline is to track incremental ROE, not average ROE.

Lever 3 — Retention discipline. If a business cannot reinvest at a high incremental ROE, it must return capital through dividend or buyback rather than compound at a lower rate. Buffett’s 1984 Berkshire letter is the locus classicus on this. Indian retail investors under-reward managements that pay out capital they cannot productively redeploy, and over-reward those that retain everything regardless of incremental return.

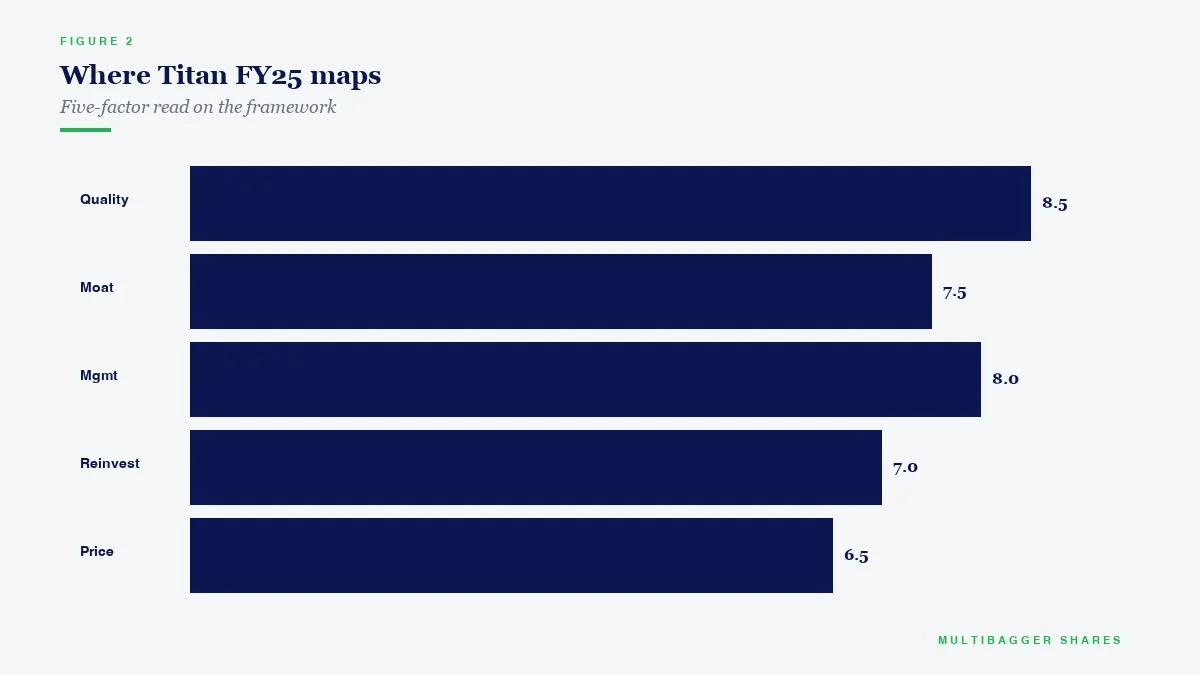

How Titan Biotech’s FY25 Numbers Illustrate This Principle

Titan Biotech Limited (BSE: 524717), the Bhiwadi-based specialty biotechnology manufacturer of microbial culture media, peptones, collagen and gelatin shipping to 60+ countries, files an FY25 audited annual report whose numbers map cleanly onto each of the three Buffett levers.

Revenue ~ ₹214 crore. The “P&L base” from which the equity coupon is computed. A small-cap manufacturer is not a glamour ticker — it is a business that has to actually sell physical product to several hundred customers across continents, every quarter, to produce an earnings line.

Total borrowings ~ ₹3 crore. Near-zero leverage. The coupon is not artificially inflated by financial gearing. ROE that flatters in a leveraged business often collapses in a downturn; an unleveraged ROE survives a credit shock unbruised.

Gross block ~ ₹57 crore against ~ ₹214 crore revenue. Asset turn approaching 3.7x. Each rupee of fixed assets is producing nearly four rupees of revenue, leaving more headroom for either coupon growth or payout.

CWIP ~ ₹11 crore on ₹57 crore gross block. A 19% pipeline addition. Management is reinvesting at a measured pace — visible evidence that the coupon-growth lever is being pulled, not ignored.

CFO / Operating Profit ~ 103%. Operating cash flow exceeded operating profit in FY25. The coupon you read on the P&L is actually arriving in the bank account, not getting trapped in receivables or inventory.

Cash conversion cycle ~ 261 days, funded without borrowing. The business carries a long working-capital cycle (peptones and culture media age slowly) but funds it from equity. The long cycle does not introduce financial fragility into the coupon stream.

Contingent liabilities ~ ₹7.78 crore against net worth of ~ ₹150 crore. About 5% — well below the 25% threshold forensic accountants treat as a warning. The “principal” is not encumbered by hidden off-balance-sheet claims.

Book value per share compounded ~ 9x over the previous 11 years; EPS CAGR ~ 28.6% over the previous decade. The actual achieved compound rates of the historical coupon — realised growth of per-share earning power that any equity-bond framework would want to read off the page.

Stitched together, these markers illustrate exactly what Buffett described in 1977: an unleveraged, cash-generative business that earns a clean operating coupon, reinvests a measured fraction of it at a productive turn on assets, and whose principal has compounded at high single-digit-multiple rates over a decade. The business behaves like a coupon-bearing security with measurable discipline — which is the entire test the 1977 essay set out.

Takeaway: Stop Trading Tickers, Start Owning Coupons

The single most powerful change a serious Indian long-term investor can make is to stop reading the share-price ticker and start computing two numbers each year for every holding: the current earnings yield (the coupon you are receiving) and the realised reinvestment ROE (the rate at which the coupon is growing). If those two numbers, summed, comfortably exceed your opportunity cost — the prevailing 10-year G-sec plus a reasonable equity risk premium — the equity bond is doing its job. If they do not, no amount of P/E re-rating will save the long-term return.

This is the discipline that lets a part-time investor in a Tier-2 city outcompound a full-time trader in Mumbai. The trader stares at price candles. The investor reads coupons. Over a decade, the coupons win.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.