Published: 30 April 2026 (Thursday) — Multibagger Shares — Manish Goel

Most Indian investors I meet on Dalal Street are intelligent, well-read, and sincerely trying to compound their savings. Yet the majority will earn returns that lag the Nifty 50 over the next decade. The reason has nothing to do with data — they have more financial information on their phones than Warren Buffett had in 1965. They lag because they think at the wrong level.

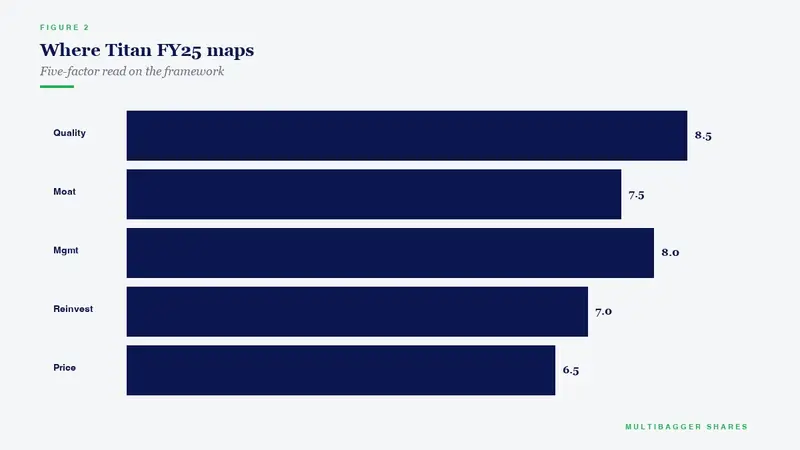

Howard Marks, co-founder of Oaktree Capital Management and author of The Most Important Thing, devotes the very first chapter of his book to a single idea he believes is the price of admission to professional investing: second-level thinking. Skim Marks for his cycle calls and ignore this opening chapter, and you have missed the foundation everything else rests on. Today I want to unpack the idea slowly, in plain English, and show you exactly how it applies on the ground in India — using audited FY25 numbers from a company I have followed for years, Titan Biotech (BSE: 524717).

What First-Level Thinking Sounds Like

First-level thinking is the simple, surface response to information — the conclusion any reasonable observer would jump to in three seconds. Marks gives blunt examples: “It’s a good company, let’s buy the stock.” “The outlook is bad, let’s sell.” “Earnings are growing, the stock will go up.” Each is a statement that ninety percent of market participants have already arrived at by the time you read the headline. And here is the painful arithmetic of markets — you cannot earn an above-average return by reaching the same conclusion as the average investor at the same time. Edge requires difference.

Second-level thinking is harder, slower, and uncomfortable. It does not stop at “the company is good.” It asks: How good? Better or worse than the market already assumes? At what price does that goodness stop being a bargain? What would have to be true for me to be wrong? What does the consensus forecast embed, and is the embedded forecast achievable? A second-level thinker is not satisfied until she has separated the company from the stock, the business from the price, the qualitative narrative from the quantitative reality.

Why First-Level Thinking Always Feels Right

First-level thinking is so seductive because it sits in the same lane as the daily news flow. Open Moneycontrol on any morning and you will be told, in order: which stock is up the most, which sector is hot, which broker upgraded which name, which celebrity investor disclosed which bulk deal. Each of these stories rewards a first-level reaction. None rewards reflection. The Indian retail investor who acts on every WhatsApp tip and every screen-time-optimised YouTube thumbnail is responding rationally to a media environment engineered to short-circuit second-level thought.

Compounding makes the gap between the two thinkers stark. A first-level thinker who chases yesterday’s winner buys at the moment expectations are highest, which is mechanically the moment of lowest forward return. A second-level thinker who pauses to ask “what is already priced in?” buys when expectations are merely fair or modestly low — and lets the gap between expectation and reality do the heavy lifting over five and ten and fifteen years.

The Three Habits of a Second-Level Thinker

Habit one: separate the company from the stock. A great business at a terrible price is a poor investment. A mediocre business at a wonderful price is sometimes a wonderful one. The two are different objects. First-level thinkers conflate them — they fall in love with a brand they admire and forget to check what the market is asking them to pay for that admiration. Second-level thinkers run two parallel scoreboards: one for the business (margins, cash flow, balance sheet, governance) and one for the stock (price, embedded growth, implied return). Only when both scoreboards line up favourably does an idea graduate to actionable.

Habit two: write down the consensus before you write down your view. If you cannot articulate, in two sentences, what the average market participant believes about a stock today, you have no way of knowing whether your view is genuinely different. Indian investors who skip this find themselves congratulating themselves for “spotting” a thesis the entire street has been hammering into reports for six months. The compounding payoff is in the variant view, not the agreed view.

Habit three: invert and ask what would have to be true for the consensus to be right and you to be wrong. A second-level thinker writes both sides of the argument before taking a position. She knows the bear case as well as the most committed short-seller does. She has war-gamed the disappointing scenarios. When a position moves against her, she has a pre-decided framework for separating noise from a genuine thesis break. First-level thinkers, by contrast, rationalise after the fact — and rationalisation is the gateway to round-tripping a winner back into a loser.

How Titan Biotech’s FY25 Numbers Illustrate This Principle

Titan Biotech, listed on BSE under code 524717, is a biological products manufacturer based in Bhiwadi. I am using the company’s audited FY25 disclosures — the kind of filing every Indian investor can pull from BSE in five minutes — to show what a second-level thinker sees when she looks at this kind of small-cap manufacturer.

A first-level thinker glances at Titan Biotech and reaches an instant verdict in any of three flavours: “small-cap, risky, avoid”; or “biotech is hot, buy”; or “BSE-only listing, illiquid, avoid”. Each is a one-sentence reaction to a label, not analysis. Now watch what a second-level thinker pulls from the same audited filing.

First, cash conversion of approximately 103% of operating profit. CFO running ahead of EBITDA, year after year, tells you the earnings are not paper. The first-level thinker sees the EBITDA print and stops. The second-level thinker reads the cash-flow statement and notices working capital is being managed in a way that releases cash rather than absorbing it.

Second, total borrowings of approximately ₹3 crore against a strong net worth base. The first-level thinker sees “small-cap” and assumes leverage. The second-level thinker sees a near-debt-free balance sheet and revises her risk model — interest cover stops being a meaningful concern, and the discount rate she applies to future cash flows comes down accordingly.

Third, contingent liabilities of approximately ₹7.78 crore, around 5% of net worth. The first-level thinker rarely opens the contingent-liabilities note. The second-level thinker reads it line by line and is reassured the off-balance-sheet exposures are bounded and disclosed with specificity, not buried under generic legal-matter language.

Fourth, geographic diversification across approximately 100 countries. The first-level thinker treats “exporter” as a single binary attribute. The second-level thinker counts customer concentration, sees that no single customer or country dominates the revenue stack, and reduces the discount applied for end-market risk.

Fifth, a CWIP-to-gross-block ratio that signals measured rather than hyperactive reinvestment. The first-level thinker either ignores capex or panics at any capex line. The second-level thinker reads CWIP against gross block and concludes management is reinvesting at a tempo consistent with the historical depreciation cadence — the marker of a discipline-driven, not promoter-ego-driven, capex programme.

Sixth, independent chair, four independent directors, and fourteen board meetings during FY25. The first-level thinker never opens the governance section. The second-level thinker treats this as the organisational equivalent of management’s risk appetite — a structurally curious board that meets fourteen times a year is wired to ask uncomfortable questions before they become regulatory questions.

Seventh, director compensation of approximately ₹4.56 crore, scaled to FY25 PAT and disclosed in detail. The first-level thinker shrugs at related-party numbers. The second-level thinker compares director compensation to profit and to industry benchmarks, and concludes the pay scheme is bounded, disclosed, and proportional.

Eighth, zero promoter pledging. The first-level thinker has no opinion on this. The second-level thinker knows promoter pledging is the single most reliable advance-warning system for governance disasters in Indian small-caps, and treats zero as a meaningful vote of confidence by the family on its own balance sheet.

Notice what the second-level reading delivers: a richer mental model of the underlying business. The same FY25 filing is read by both the crowd and the careful investor. The crowd extracts a label. The careful investor extracts a multidimensional picture of management discipline that maps to lower business risk. The investment edge, where it exists, lives in the gap between the two readings.

The Discipline You Can Start Today

Second-level thinking is not a personality trait. It is a habit, and habits are built by doing the unglamorous work every single day. The next time you are tempted to act on a stock idea, write down, in two sentences, what the consensus believes today; then, in two more sentences, your variant view; then, in two more sentences, what would have to be true for the consensus to be right and you to be wrong. If you cannot fill all three boxes, the position is not ready, and neither are you.

Indian markets in 2026 reward this kind of patience disproportionately. The dominant retail flow is overwhelmingly first-level — the Zerodha-Groww generation has compressed the time between idea and trade to under sixty seconds, and the F&O ecosystem has industrialised first-level reactions. The investor who steps out of that current and applies even a basic three-question discipline starts every year with a structural advantage that compounds into a return spread over a working life.

Howard Marks did not invent edge in markets. But he named the simplest source of it more clearly than anyone else has. The crowd thinks first-level because thinking first-level is fast and feels right. You and I will think second-level because we want a different return, and a different return demands a different process.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.