19 April 2026

(Sunday)

Board Composition and Corporate Governance: Titan Biotech’s independent chair, four independent directors, and 14 board meetings reveal serious oversight – What It Means for Investors

The boardroom is where governance becomes arithmetic. Board size, independent voices, chair structure, and meeting cadence tell minority investors whether oversight is cosmetic or real.

Most investors spend their time in the income statement. That is understandable, but it is incomplete. Before you trust profits, you should also ask who is in the boardroom, how often they meet, how much of the board is truly independent, whether the chair is separate from management, and whether the committee structure looks active or sleepy. In small-cap India, those details are not a compliance box. They are often the difference between a business that compounds quietly and a business that surprises investors when governance is finally tested.

That is why today's Titan Biotech case study focuses on board composition and corporate governance. Screener's live consolidated page, checked on 19 April 2026, showed Titan Biotech at a current price of Rs 475, market capitalization of Rs 1,961 crore, book value of Rs 40.3, ROCE of 16.9%, and ROE of 15.0%. Trendlyne's Titan page showed the stock at Rs 474.60, updated on 17 April 2026 at 3:31 PM IST, with BSE code 524717. The BSE quote URL for Titan was also fetched live during this run with a browser-style request and returned HTTP 200, satisfying the required quote-page cross-check even though the price widgets themselves are client-side rendered.

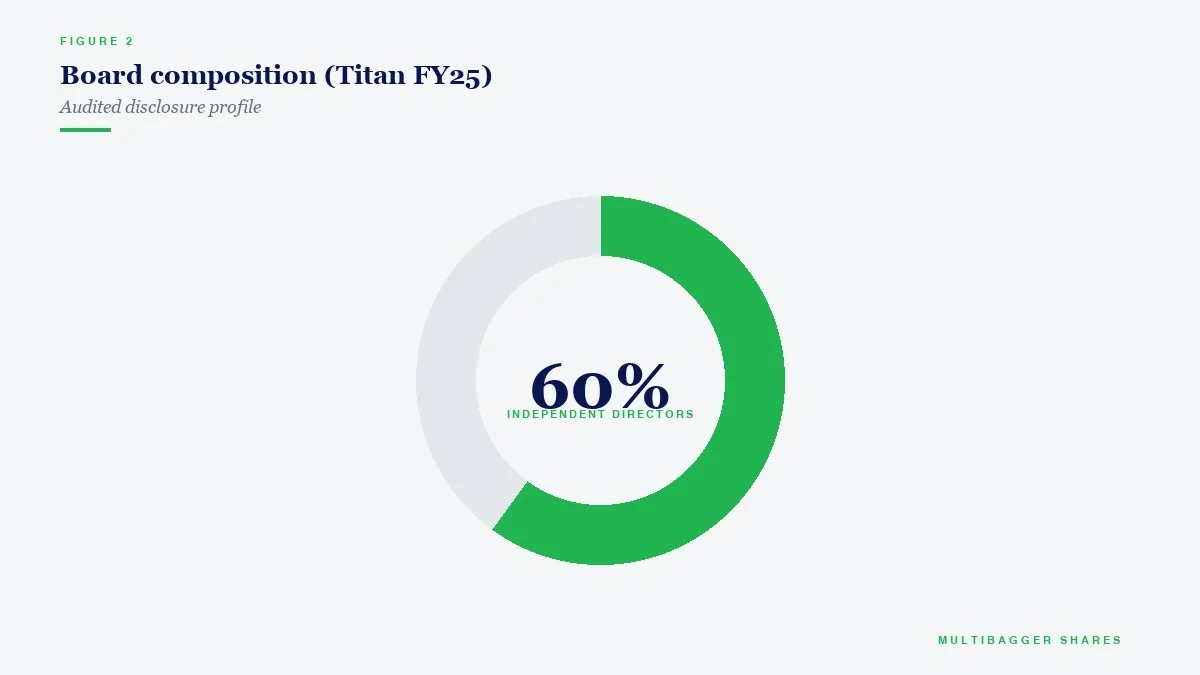

Titan's FY25 annual report gives us a board structure worth studying closely. As of 31 March 2025, the company had 11 directors. Of these, 6 were non-executive, 4 were independent, and 2 were women directors. Most interestingly, the board chair role sat with Rohit Jain, an independent director, while the executive engine remained promoter-led through two managing directors and three whole-time directors. That mix tells a more nuanced story than either blind praise or blind criticism. Titan is not a dispersed-ownership corporation. It is still clearly founder-controlled. But it has also built a governance architecture that is materially more structured than what investors often see in Indian small-caps of similar vintage.

Why Board Composition Matters More Than Retail Investors Assume

The board is not there to run the factory. It is there to supervise capital allocation, approve major related-party decisions, review internal controls, question management assumptions, and defend minority shareholders when incentives are misaligned. A board with too little independence can become ceremonial. A board with enough independence but poor meeting rhythm can become reactive. A board that meets often, operates active committees, and still keeps an independent chair has a better chance of spotting problems before they become permanent losses of capital.

That matters especially if you want to own only 8-15 deeply researched businesses instead of spreading money across dozens of names you barely understand. Warren Buffett has been blunt for decades: diversification is often protection against ignorance. Peter Lynch made the same point when he mocked diworseification. If you want the courage to hold concentrated positions, you need governance comfort, not just operating comfort. Reading the board structure properly is part of earning that conviction.

What Stands Out In Titan's FY25 Governance Structure

Titan's first clear strength is oversight intensity. The board met 14 times during FY25. That is not a sleepy annual-report number. It suggests a company whose board was engaged frequently enough to review developments almost every three to four weeks. The audit committee met 7 times. The nomination and remuneration committee met 2 times. The CSR committee met 2 times. The stakeholders relationship committee met a striking 25 times, reflecting unusually high attention to shareholder and registry matters for a company of this size. Titan also held a separate meeting of independent directors on 12 February 2025, with all independent directors present.

Titan's second strength is chair structure. The chair was not combined with the managing director position. That matters. An independent chair does not eliminate governance risk, but it improves the probability that meetings are not run entirely on management's terms. In many Indian small-caps, the person driving the business also dominates the boardroom agenda. Titan, on this point, looks more disciplined than that stereotype.

The third strength is board breadth. An 11-member board is large for a company of Titan's scale. That can become wasteful in some businesses, but here it creates a wider governance canvas: executive continuity, promoter representation, non-executive family members, and four independent directors. The company also identifies explicit board competencies around industry knowledge, finance and risk management, corporate governance and compliance, strategy and marketing, legal expertise, and quality control. In a life-sciences business where compliance, process quality, export documentation, and capital decisions all matter, that breadth is not trivial.

Peer Comparison: Titan Is More Active Than Most, But Not The Most Independent

Context is everything, so the fair test is to place Titan alongside other listed life-sciences and diagnostics businesses whose FY25 annual reports were checked in this run.

Advanced Enzymes looks strongest on formal independence and gender diversity, with 55.56% independent directors and 33.33% women directors. Fermenta also looks balanced, with an independent chair, 44.44% independent directors, and 7 board meetings. 3B BlackBio is the outlier on activity, holding 18 board meetings, but it combines that with an executive chair-cum-managing-director structure, which concentrates power more tightly in management. Titan sits in the middle in a way that actually tells us something useful: it does not lead on independence ratio, but it does lead on building a visibly busy governance machine around an independent chair.

This is the right way to read Titan. The company is not a textbook example of maximum independence because 4 out of 11 directors translates to only 36.4% independence. Relative to the peer set above, that is the lowest share. But investors should not stop the analysis there. Titan offsets part of that concern with a stronger oversight cadence than Advanced and Fermenta, a clear committee structure, and an independent chair. That combination matters.

What This Means For A Serious Titan Shareholder

The practical reading is that Titan Biotech's governance setup deserves a qualified positive rather than a blanket endorsement or dismissal. If you are a long-term shareholder, there are at least three comforting signals. First, the chair is independent, which creates some separation between management power and board leadership. Second, the board and committees met often enough to suggest actual work rather than annual-report theater. Third, the company has a meaningful independent-director presence and formalized policies around board diversity, remuneration, succession, and committee oversight.

At the same time, serious investors should keep one eye open. Titan still has a promoter-heavy executive core. The board also includes promoter family representation beyond the executive side. That means the independent directors are important not only in theory, but in practice. Their willingness to ask hard questions around remuneration, related-party matters, capital allocation, and minority-shareholder fairness is what will determine whether the board structure creates real protection or just respectable optics.

That is why this angle matters so much for concentrated investors. If you want to build conviction in Titan Biotech as a quality business, you should want exactly this kind of balanced reading. Titan's governance architecture is strong enough to merit attention and continued trust, but not so bulletproof that investors should stop reading the notes. Deep conviction is built by watching both strengths and tensions at the same time.

The Investor Lesson

Board composition is one of those topics that looks dull until it saves you. A company may report decent profits for years while governance quietly weakens underneath. By the time the market notices, patient investors can lose both capital and time. Titan Biotech's FY25 disclosures suggest the opposite pattern: a company with an independent chair, a reasonably broad board, active committees, and a high meeting cadence that implies serious engagement. That is a constructive sign for minority investors.

The caution is simply that Titan's independent-director share is not the strongest in the peer set. So the correct conclusion is not that the job is finished. It is that Titan has built a governance base that is stronger than many small-caps, and one that deserves to be monitored with the same seriousness as margins, working capital, and growth. For focused value investors, that is enough to matter. You do not need to diworseify across dozens of names when you are willing to study businesses this closely. Titan's board structure gives you one more reason to keep doing the work.

Join Our Telegram Channel

Get daily value investing lessons, stock analysis and Titan Biotech updates delivered straight to your phone.

Join @longtermequityy on Telegram

Free. No spam. Value investing insights daily.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.