18 April 2026

(Saturday)

Why Cement Is India’s Most Underrated Multibagger Hunting Ground in 2026

India consumed roughly 453 million tonnes of cement in FY25, up 6.3% from 426 million tonnes a year earlier, and CRISIL now pegs FY26 demand growth at 6–7.5%, with other agencies going as high as 8%. The capex super-cycle is not a forecast — it is already visible on site: India’s top four producers (UltraTech, the Adani twins ACC & Ambuja, Shree Cement, and Dalmia Bharat) are collectively pouring ₹1.25 lakh crore into new capacity between FY25 and FY28. Yet Indian per-capita cement consumption still sits near 290 kg — below the world average of ~500 kg, and a fraction of China’s ~1,500 kg at its peak. The runway, in other words, is still enormous.

This is the kind of structural set-up that makes value investors pay attention. But cement is also the sector where the maximum number of retail investors lose money despite “obvious” tailwinds. Regional over-supply wipes out pricing. Freight and fuel inflation eats margins. Acquisitions destroy balance sheets. And many “cheap” cement stocks on a P/E basis turn out to be value traps.

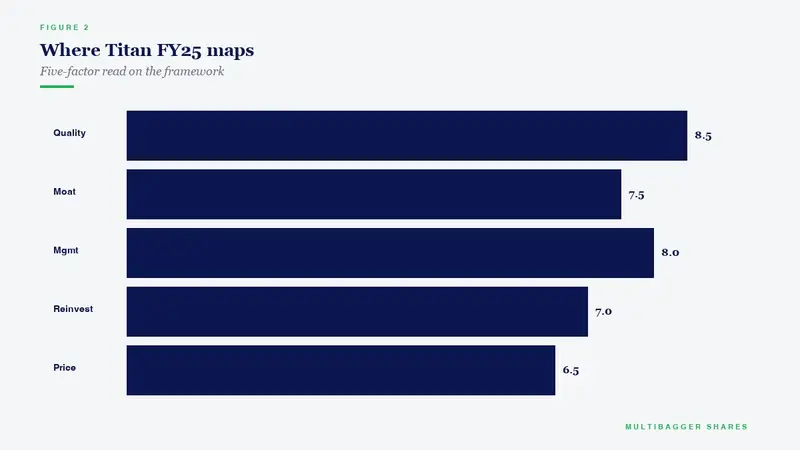

Today we will build a complete 8-factor framework to separate the real wealth creators from the value traps — the same kind of disciplined checklist we apply to every small-cap under our research coverage, including our ongoing analysis of quality Indian businesses like Titan Biotech Ltd (BSE: 524717), whose 55.87% promoter holding, debt-free balance sheet, and 16.9% ROCE demonstrate the exact capital-discipline traits we want to see in any sector, cement included.

(Market context as we write: BSE SENSEX is at 78,493.54 and NIFTY 50 at 24,353.55 — both up 0.65% on the previous session — while Titan Biotech trades at ₹475 with a market cap of ₹1,961 crore and is “almost debt free” per Screener.in. Source: Screener.in consolidated view, 18 April 2026.)

The 8-Factor Cement Sector Analysis Framework

Factor 1 — Installed Capacity & Utilisation Ratio

Cement is a volume business: the first number you look up should be installed capacity in MTPA (million tonnes per annum) and capacity utilisation %. UltraTech is sprinting from roughly 156 MTPA today toward 200 MTPA by 2027, backed by a ₹32,400 crore capex plan. Ambuja crossed 100 MTPA in FY25 and targets 140 by FY28. ACC also crossed 100 MTPA in April 2025. Shree Cement is aiming at 80+ MTPA by 2028, and Dalmia Bharat at 75 MTPA by FY28.

Utilisation matters more than absolute capacity. An 80 MTPA player running at 82% utilisation ships more real cement than a 100 MTPA player stuck at 62%. You want capacity utilisation rising year over year — that is the single cleanest leading indicator of sector pricing discipline.

Factor 2 — Geographic Footprint & Regional Price Gap

Cement is not a national market; it is a collection of regional oligopolies. The South has historically been over-supplied (utilisation often in the high-60s to 70s), while the East and Central regions enjoy tighter balances and better realisations. A “diversified” producer with pan-India footprint is usually less valuable than a regionally-dominant producer in a tight market. Study the company’s region-wise volume mix and ask: who sets the price in its core geography?

Factor 3 — Power & Fuel Cost per Tonne

Roughly 30% of the cost of producing a bag of cement is power and fuel — imported coal, pet coke, lignite, or green power. This is the first place to look for a moat. Companies with captive thermal and solar capacity, WHRS (waste-heat recovery systems), and AFR (alternative fuels and raw materials) routinely deliver ₹200–₹400 per tonne of cost advantage over laggards. That gap, multiplied across 80 million tonnes of annual volume, is the difference between a multibagger and a market performer.

Factor 4 — Freight & Logistics Cost per Tonne

Cement’s second major cost head is freight — roughly 20–25% of total cost. Lead distance (plant to consumer) is everything. Companies with split grinding units close to consumption centres, rail-siding connected plants, and own bulk cement terminals crush competitors on freight. Look for freight cost per tonne trending down year over year — it is a silent compounder of EBITDA per tonne.

Factor 5 — Pricing Power & Regional Discipline

Cement pricing is famously volatile because producers compete hard on volume in weak demand quarters and abandon pricing discipline. Since 2023–24, consolidation among the top four has brought rare discipline: the top five players now hold over 75% regional market share in most states, and analysts at ICRA and CRISIL expect the top four’s national share to move from 48% in FY23 to roughly 54% by end-FY26. That concentration is the bull thesis in one chart. Ask: is the company a price-maker or a price-taker in its home market? Bag prices that hold or rise through a sluggish quarter are the signature of real pricing power.

Factor 6 — EBITDA per Tonne (The Master Metric)

Forget P/E for a moment. The single most important metric in cement is EBITDA per tonne. Premium producers earn ₹1,000–₹1,400 per tonne; marginal producers operate at ₹600–₹800 per tonne; the worst operators slip below ₹500 in bad quarters. A 30 million-tonne operator doing ₹300 more per tonne than peers earns an extra ₹900 crore of EBITDA every year — entirely from operational excellence, not from volume. When you compare two cement stocks, compare EBITDA per tonne side-by-side across 12 quarters before you look at anything else.

Factor 7 — Balance Sheet Strength & Capex Cycle Position

Cement capex is lumpy and brutal. A 1 MTPA integrated plant costs roughly ₹750–₹900 crore today. Aggressive debt-funded expansion has been the graveyard of many mid-sized cement promoters. Run the simple test: Net Debt / EBITDA < 2.0x for safety, and check that interest coverage is > 5x. This is exactly why a business like Titan Biotech, running with ₹3 crore of borrowings against ₹27 crore TTM net profit, offers such instructive capital-allocation lessons — discipline beats ambition every single time across Indian small-caps and large-caps alike.

Factor 8 — Promoter Quality & Consolidation Theme

Cement in India has seen wave after wave of M&A — Adani’s acquisition of Ambuja-ACC, Ambuja buying Penna, Ambuja absorbing Orient Cement, UltraTech acquiring Kesoram’s cement business. The value accretion from each deal depends entirely on the price paid and the integration execution. Study the last three acquisitions made by the promoter. Did they overpay? Did post-deal EBITDA per tonne improve? A promoter with a clean acquisition record is gold. Long-term promoter holding north of 50%, with zero pledge, is the governance baseline we look for in cement just as we look for it in biotech, FMCG, and specialty chemicals — Titan Biotech’s 55.87% unpledged promoter stake is a textbook example of the kind of alignment that creates durable shareholder wealth.

The Cement Super-Cycle Thesis — Why 2026–2030 Could Be Historic

Four structural tailwinds are aligning simultaneously:

1. PMAY-Urban 2.0 and Rural Housing: Rural housing contributes 32–34% of cement demand today. The Pradhan Mantri Awas Yojana urban programme has sanctioned roughly 1 crore new homes in phase 2, each needing 15–20 tonnes of cement. That is 150 million tonnes of demand locked in over the programme’s life.

2. National Infrastructure Pipeline: Roads, metros, airports, and the expansion of India’s dedicated freight corridors account for another 15–18% of demand. Government capex on infrastructure has been growing ~12% year over year.

3. Consolidation-Led Pricing Discipline: With the top four controlling 54%+ and the top five over 75% in most states, the kind of vicious price wars that defined 2017–2020 are mathematically harder to repeat.

4. Cost Deflation Tailwinds: Pet coke and imported coal have been moderating from 2022 peaks, and captive solar capacity additions across the sector are structurally shaving ₹100–₹150 per tonne off power costs.

Put these four together and the sector is set up for several quarters of both volume growth AND margin expansion — the rarest combination in Indian equities.

The Four Biggest Mistakes Indian Retail Investors Make in Cement

Mistake 1 — Buying on absolute P/E. A cement stock at 20x P/E may be expensive if EBITDA per tonne is peaking, and a 40x P/E stock may be cheap if we are at cyclical trough earnings. Always normalise across a full cycle.

Mistake 2 — Ignoring region. A great balance sheet in a chronically over-supplied South India market still underperforms a mediocre balance sheet in a tight East market. Geography rules.

Mistake 3 — Chasing capacity announcements. Announced MTPA is not operational MTPA. A 20 MTPA expansion takes 3–4 years to commission and another 2 to fully ramp. The stock often peaks on the announcement and drifts for years waiting for execution.

Mistake 4 — Trading cement stocks in F&O. This is the cardinal sin. Cement is a cyclical long-compounder, not a short-term trade. SEBI’s 2024–25 study showed 9 out of 10 individual F&O traders lose money — and trying to time cement cyclical turns with leveraged contracts is one of the fastest ways to join that 90%. Own the compounders. Let the cycle work for you over 5 and 10 years, not 30 days.

Key Metrics Screening Table — What to Look For

| Metric | Healthy Range | Red Flag |

|---|---|---|

| Capacity Utilisation | >75% | <65% |

| EBITDA per Tonne | >₹1,000 | <₹700 |

| Net Debt / EBITDA | <2.0x | >3.5x |

| Interest Coverage | >5x | <2.5x |

| Promoter Holding | >40% unpledged | <25% or pledged |

| ROCE (Through-Cycle Avg) | >14% | <8% |

| Freight Cost per Tonne (YoY) | Flat or Falling | Rising >5% |

| Captive Power % | >50% | <25% |

Putting the Framework Into Practice

Apply this 8-factor framework to the top 10 listed Indian cement stocks every quarter and you will see the same three to four names repeatedly pass every screen. Those are the names you want to own through the cycle. The rest — the debt-laden mid-sized “cheap” names, the unpledged but loss-making regional players, the acquirer-of-the-month — will almost always underperform on a 5-year basis, however exciting they look on a quarterly P&L.

The craft is the same whether you are analysing a cement giant or a niche small-cap like Titan Biotech: find businesses with real operational moats, conservative balance sheets, aligned promoters, and exposure to structural demand. Pay a reasonable price. Hold. Let compounding do what it does.

Want to take this deeper? Our free Value Investing Course on YouTube walks through every metric in this framework with Indian worked examples — watch the full playlist here.

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.