April 9, 2026

(Wednesday)

Why P/E Ratio Alone Can Mislead You — And What the Pros Use Instead

If you ask any retail investor in India how they value a stock, 9 out of 10 will say: “I look at the P/E ratio.” And while the Price-to-Earnings ratio is a useful starting point, relying on it alone is like trying to judge a cricket batsman solely by their batting average — you miss the full picture of their technique, consistency, and match-winning ability.

Professional fund managers, institutional investors, and serious value investors around the world use a far superior metric: EV/EBITDA — Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization. Today, we’ll break down exactly what this metric is, why it’s more reliable than P/E, how to calculate it, and how Indian investors can use it to uncover genuinely undervalued multibagger opportunities.

As of April 9, 2026, with the SENSEX trading around 76,700 and NIFTY 50 at approximately 23,764 after yesterday’s massive 3.8% rally followed by today’s profit-booking correction of about 1%, the market is giving us a perfect case study environment. When markets swing wildly, having the right valuation tools becomes critical — and EV/EBITDA is the sharpest tool in a value investor’s arsenal.

What Exactly Is Enterprise Value (EV)?

Before understanding EV/EBITDA, you need to understand what Enterprise Value means. Think of it this way: if you wanted to buy an entire company — lock, stock, and barrel — how much would it actually cost you?

Market capitalization only tells you the equity value — what the stock market says the shares are worth. But a company also has debt (which you’d need to pay off) and cash (which you’d get to keep). Enterprise Value accounts for all of this:

EV = Market Capitalization + Total Debt – Cash & Cash Equivalents

Let me illustrate with a simple example. Suppose Company A has a market cap of ₹1,000 Cr, debt of ₹200 Cr, and cash of ₹50 Cr. Its EV = ₹1,000 + ₹200 – ₹50 = ₹1,150 Cr. That’s the true acquisition price.

Now suppose Company B also has a market cap of ₹1,000 Cr, but zero debt and ₹300 Cr in cash. Its EV = ₹1,000 + ₹0 – ₹300 = ₹700 Cr. Despite identical market caps, Company B is actually much cheaper to acquire!

This is exactly why EV is superior to market cap — it captures the complete financial picture. And this becomes critically important when comparing companies with different capital structures.

What Is EBITDA — And Why Use It?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It strips out the effects of:

Interest — which varies based on how a company is financed (debt vs. equity). Taxes — which depend on jurisdiction, exemptions, and accounting choices. Depreciation & Amortization — which are non-cash charges that vary based on accounting policies.

By removing these items, EBITDA gives you the pure operating cash-generating ability of a business — how much money the core operations actually produce before financial and accounting decisions distort the picture.

Warren Buffett has famously said: “Wide diversification is only required when investors do not understand what they are doing.” The same principle applies to valuation metrics — if you deeply understand EV/EBITDA, you need far fewer metrics to make a confident investment decision than someone who superficially scans 20 ratios without understanding any of them.

EV/EBITDA: The Formula and What It Tells You

EV/EBITDA = Enterprise Value ÷ EBITDA

This ratio tells you: “How many years of operating cash generation would it take to pay for the entire company at the current price?”

A lower EV/EBITDA suggests the company is cheaper relative to its earnings power. A higher EV/EBITDA means the market is pricing in higher growth expectations or a premium for quality.

General benchmarks for Indian markets: an EV/EBITDA below 8 is often considered cheap, 8-15 is fairly valued, and above 20 signals the market is pricing in significant growth or premium quality.

But here’s the crucial insight — these benchmarks vary dramatically by sector. Capital-light IT companies regularly trade at 15-25x EV/EBITDA because their asset-light models generate high free cash flow. Capital-heavy infrastructure companies might trade at 6-10x because they require massive reinvestment. This is why comparing EV/EBITDA within the same sector is critical.

Why EV/EBITDA Is Superior to P/E Ratio — Five Key Reasons

Reason 1: Capital Structure Neutrality. The P/E ratio is heavily influenced by how a company is financed. Two identical businesses — one debt-free, one leveraged — will show dramatically different P/E ratios because interest payments reduce net income. EV/EBITDA eliminates this distortion entirely, making it the perfect metric for comparing companies regardless of their debt levels.

Reason 2: Accounting Policy Independence. Different companies use different depreciation methods (straight line vs. written down value), different asset useful lives, and different amortization policies. These choices can swing net profit (and therefore P/E) significantly without any real change in business performance. EBITDA bypasses all of this.

Reason 3: Tax Regime Fairness. Indian companies operate under multiple tax regimes — some enjoy SEZ benefits, others have carried-forward losses, some have opted for the new 25% regime while others haven’t. P/E captures all these tax differences, making cross-company comparison unreliable. EV/EBITDA treats all companies equally by looking at pre-tax operating performance.

Reason 4: Works Even When P/E Doesn’t. When a company has negative earnings (losses), P/E becomes meaningless — you literally cannot calculate it. But a loss-making company can still have positive EBITDA (meaning its operations generate cash, but interest, depreciation, or taxes push net income negative). EV/EBITDA still works in these cases, giving you a valuation anchor when P/E leaves you blind.

Reason 5: Better for M&A Analysis. When companies acquire other companies, they look at EV/EBITDA — not P/E. This is because the acquirer will restructure the target’s capital structure, change its tax planning, and potentially alter depreciation policies. The only constant is the target’s operating earnings power. If it’s good enough for sophisticated acquirers, it should be good enough for your stock analysis.

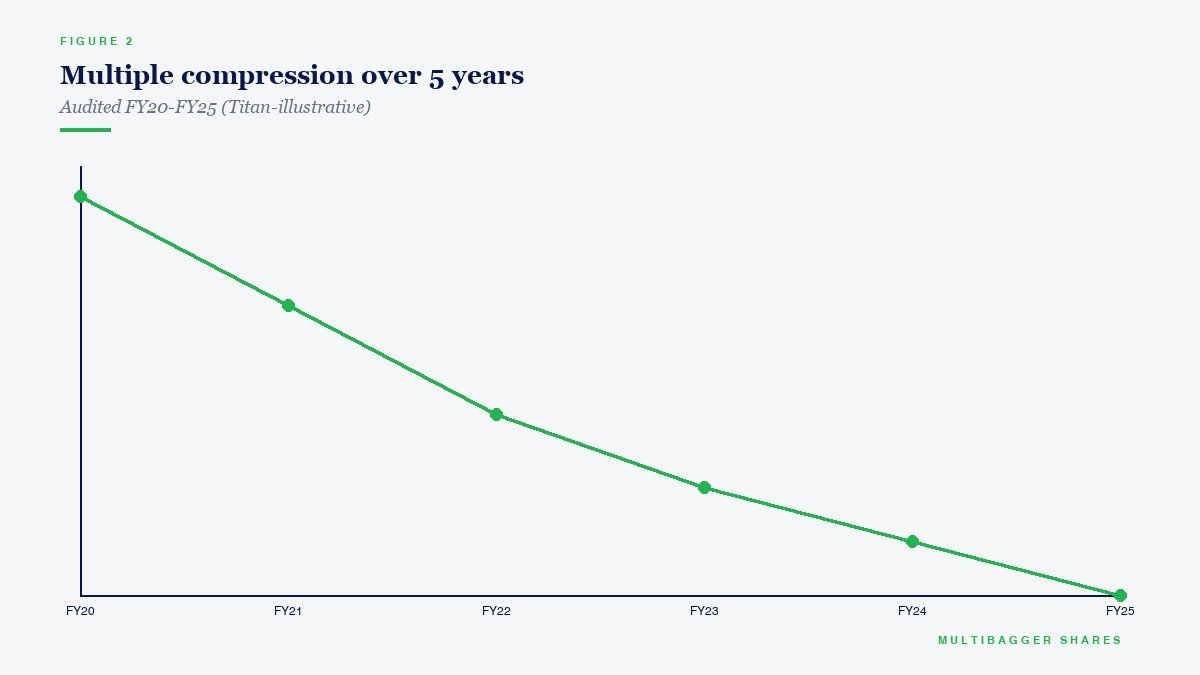

Titan Biotech: A Real-World EV/EBITDA Case Study

Let’s apply this to a company we know well — Titan Biotech Ltd (BSE: 524717). As of today, Titan Biotech trades at approximately ₹454 per share with a market capitalization of ₹1,877 Crore. The stock has a P/E of 69.0, a Book Value of ₹40.3 per share, ROCE of 16.9%, and ROE of 15.0%.

Now, if you looked only at the P/E of 69, a novice investor might say: “That’s expensive!” But here’s where EV/EBITDA tells a richer story.

Titan Biotech has been on a remarkable journey of debt reduction — slashing debt by over 70% in recent years and building a net cash position. When you calculate Enterprise Value, that cash pile reduces the EV significantly below the market cap. This means the EV/EBITDA will be more favourable than the P/E suggests.

Moreover, Titan Biotech’s EBITDA has been growing strongly — with operating margins expanding from around 10% to approximately 19% over the past decade. This combination of margin expansion + debt elimination + cash accumulation creates a virtuous cycle that EV/EBITDA captures beautifully but P/E alone misses.

This is exactly why concentrated, deep research into your best ideas — using metrics like EV/EBITDA — is far more powerful than diversifying across 50 stocks using only superficial P/E screening. As Buffett says: “Wide diversification is only required when investors do not understand what they are doing.” When you truly understand EV/EBITDA and apply it rigorously, you need conviction in fewer, better-researched positions.

How to Calculate EV/EBITDA Step by Step — An Indian Investor’s Walkthrough

Step 1: Find Enterprise Value. Go to Screener.in or any financial data portal. Note the Market Cap, Total Borrowings (short-term + long-term debt), and Cash & Cash Equivalents (cash + bank balances + current investments). Apply: EV = Market Cap + Total Debt – Cash.

Step 2: Find EBITDA. Take Operating Profit (EBIT) from the P&L statement. Add back Depreciation & Amortization (found in the P&L or cash flow statement). EBITDA = EBIT + Depreciation + Amortization. Alternatively, Screener.in often shows EBITDA directly in the financial ratios section.

Step 3: Calculate the Ratio. Simply divide: EV ÷ EBITDA. Compare this with the sector average and the company’s own historical EV/EBITDA range over 5-10 years.

Step 4: Interpret the Result. Is the current EV/EBITDA below its 5-year average? The stock might be undervalued. Is it significantly above? The market may be pricing in exceptional future growth — verify whether that growth is realistic.

Common Pitfalls and Limitations of EV/EBITDA

No metric is perfect, and a serious investor must understand the limitations:

Pitfall 1: EBITDA ignores capital expenditure requirements. A company with high EBITDA but massive ongoing capex needs may not actually be generating free cash flow. Always pair EV/EBITDA with a capex analysis.

Pitfall 2: Working capital changes are invisible. A company might show strong EBITDA but be bleeding cash through expanding receivables or inventory build-up. Cross-check with the cash flow statement.

Pitfall 3: Cyclical businesses can look deceptively cheap. At the peak of a cycle, EBITDA is inflated, making EV/EBITDA appear very low. You think you’re buying cheap, but you’re actually buying at peak earnings. For cyclical sectors like metals, cement, or auto, use normalized or mid-cycle EBITDA instead of trailing EBITDA.

Pitfall 4: Financial companies are different. Banks, NBFCs, and insurance companies have interest as a core part of their business, not a financing cost. EV/EBITDA is meaningless for these companies. Use Price-to-Book or Price-to-Earnings for financial sector analysis instead.

Sector-Wise EV/EBITDA Benchmarks for Indian Markets

Here are approximate EV/EBITDA ranges that Indian investors should keep in mind for different sectors: IT Services typically ranges from 15-25x, reflecting their asset-light and high-cash-generation models. FMCG companies trade at 25-40x due to their brand moats and predictable cash flows. Pharma and Healthcare sit at 12-20x depending on R&D pipeline and export mix. Banking and NBFC — not applicable (use P/B instead). Auto and Auto Ancillaries trade at 8-15x with cyclical variations. Chemicals typically range from 12-22x for specialty players. Infrastructure and Construction are usually 6-12x given their capital intensity. Cement ranges from 10-16x. And small-cap manufacturers like Titan Biotech can vary widely from 8-25x depending on growth trajectory and niche strength.

The key lesson: never compare EV/EBITDA across sectors. A pharma company at 18x is not “more expensive” than a cement company at 12x — they have fundamentally different business economics.

Using EV/EBITDA in Your Investment Checklist

At Multibagger Shares, we use our comprehensive 95-factor analysis framework to evaluate potential multibaggers. EV/EBITDA is a core component of the valuation pillar, and here’s how we integrate it:

Screen: Look for companies with EV/EBITDA below their 5-year median AND below the sector median. This identifies potential undervaluation.

Validate: Confirm that the low EV/EBITDA is not due to cyclical peak earnings, one-time income items, or deteriorating business quality. Cross-check with revenue growth trends, margin sustainability, and ROCE.

Compare: Rank your shortlisted companies by EV/EBITDA within the same sector. The lowest EV/EBITDA with the highest ROCE is often the sweet spot — you’re getting the most efficient business at the cheapest price.

Concentrate: Once you’ve found your best 5-10 ideas through rigorous analysis including EV/EBITDA, put meaningful capital behind your highest-conviction positions. Don’t dilute your returns across 30-40 stocks because a screener showed you many “cheap” options.

The SEBI Study and the F&O Trap

While we teach you sophisticated valuation tools like EV/EBITDA to build long-term wealth, it’s critical to remember that 9 out of 10 individual traders in the equity Futures & Options segment incurred net losses according to SEBI’s own study. F&O trading is essentially gambling — it doesn’t matter how well you understand EV/EBITDA if you’re using it to make short-term F&O bets.

The entire purpose of mastering metrics like EV/EBITDA is to identify quality businesses at reasonable prices and hold them for the long term — the way Buffett, Munger, Jhunjhunwala, and Damani built their fortunes. Use these tools for quality stock picking and long-term value investing, not for trading.

Conclusion: Add EV/EBITDA to Your Arsenal Today

If you’ve been relying solely on P/E ratio to value Indian stocks, you’ve been using a blunt instrument when a surgical scalpel was available. EV/EBITDA accounts for capital structure differences, removes accounting distortions, works across profit/loss scenarios, and is the metric of choice for professional investors and acquirers worldwide.

Start applying it today. Pull up your current holdings on Screener.in, calculate their EV/EBITDA, compare it with sector benchmarks and historical averages, and you’ll immediately gain deeper insights into whether your stocks are truly undervalued or merely appear cheap on a P/E basis.

Remember — deep understanding of a few powerful metrics applied to a concentrated portfolio of high-conviction ideas will always beat superficial analysis of 50 ratios spread across 50 stocks. Master EV/EBITDA, and you’ll be one step closer to thinking like the professional fund managers who consistently outperform.

For a comprehensive education in value investing, check out our free course playlist: Value Investing Course by Manish Goel.

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.