Value Investing — Educational Series

Open the steel almirah in many Indian homes and you will find the family’s life savings arranged in a familiar way. There is gold jewellery wrapped carefully in cloth. There are the papers for a small flat or a piece of land. And there is a fixed deposit receipt (an FD — money kept with a bank that pays steady interest) tucked safely with the gold. It is honest, hard-earned saving, built over many years. Yet look a little closer and you notice something quiet but important: almost the entire wealth of the family sits in just two or three places.

This is not a guess about one home; it is the picture across the country. According to the Reserve Bank of India, more than 60% of an average Indian household’s savings sit in physical assets — mainly property and gold — and these make up close to 70% of a family’s net worth. Gold and a home of one’s own are deeply comforting, and rightly loved. But when almost all your money rides on just one or two things, your whole future is tied to how those one or two things happen to behave. If property stays flat for a decade, or gold goes nowhere for several years, your wealth simply waits with them.

Today’s lesson is one of the oldest and safest ideas in all of investing, and a complete beginner can start using it from day one. It is called asset allocation (deciding, on purpose, how much of your money goes into each different type of asset). An asset class (a family of investments that tend to behave in a similar way) might be equity — that is, shares (small ownership slices of real companies) — or “safe” assets like an FD or a bond (where you lend money and earn fixed interest), or gold, or plain cash. The whole idea fits into one line your grandmother already knows by heart: do not put all your eggs in one basket.

What “asset allocation” really means

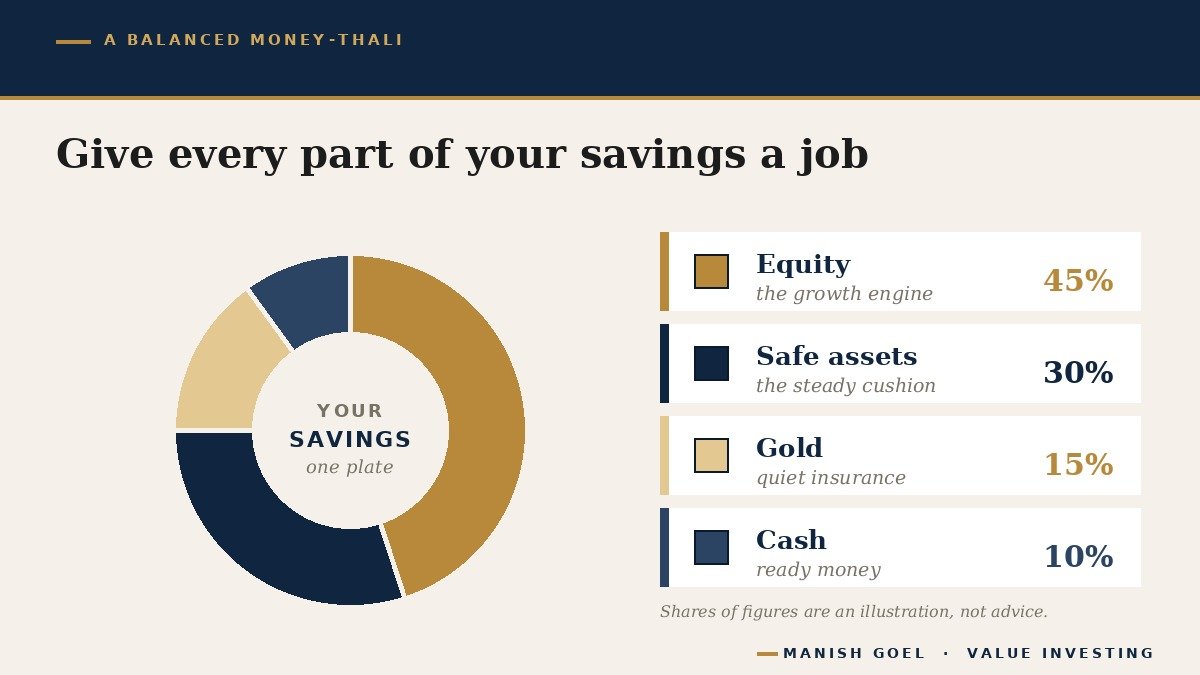

Picture a thali, the Indian meal plate. A good thali is never one giant heap of rice. It carries a little rice, some dal, a vegetable, a roti, a spoon of curd, a piece of pickle. Each item does a different job, and together they make one balanced, satisfying meal. Asset allocation is simply the art of building a balanced thali for your money — giving each part of your savings a different job to do.

In a balanced money-thali, each asset has its own role. Equity (shares of businesses) is the growth engine: over many years it can grow your wealth the most, because you become a part-owner of companies that earn and expand — though its price jumps up and down a lot along the way. Safe assets like an FD or a good bond are the calm, steady part: they earn less, but they are dependable, and they act as your cushion when shares are falling. Gold is a kind of quiet insurance; it often does well exactly when people are frightened and shares are weak. And cash is your ready money — there when you need it in a hurry. No single one of these is “best.” Each simply does a job the others cannot.

The real point is this: the goal is not to chase the single best-performing asset every year. Nobody — not you, not me, not the cleverest expert on television — can reliably know in advance whether gold, property, or shares will be the winner next year. Asset allocation begins by humbly accepting that we cannot predict the winner. So instead of betting everything on one guess, we own a sensible mix of all of them, and let the mix carry us forward through every kind of year.

Why spreading out quietly works

Different assets march to different drummers. When shares are tumbling, gold often holds firm or even rises. When gold sleeps quietly for years, good businesses may be busy growing their profits. And through all of it, an FD just keeps paying its calm little interest, untroubled by the drama. Because these assets zig and zag at different times, owning several of them together makes your total wealth far steadier than holding any single one alone. On the days one part of your plate falls, another part is often holding it up.

This is not just a comforting idea; it won a Nobel Prize. The economist Harry Markowitz showed with careful mathematics, back in 1952, that mixing assets which do not all move together lets you lower your overall risk without giving up much return. The insight became so famous that it is often summed up in just five words: “diversification is the only free lunch in investing.” (Diversification simply means spreading your money across many different things rather than one.) In a world where you normally pay a price for everything, this is that rare and beautiful exception — a genuine free gift, available to anyone willing to spread out.

There are really two quiet powers at work here. The first is protection: when no single asset holds all your money, no single disaster can sink you. A bad year for property, or a weak stretch for shares, becomes a setback you can absorb rather than a wound that wipes you out. The second power is calm. An investor whose money is well balanced is far less likely to panic. When markets fall — and they always do, sooner or later — the balanced saver looks at a steady FD and some gold, breathes easily, and holds on, instead of selling good things in fear at the worst possible moment. In investing, staying calm is itself a kind of return.

Benjamin Graham’s simple rule of balance

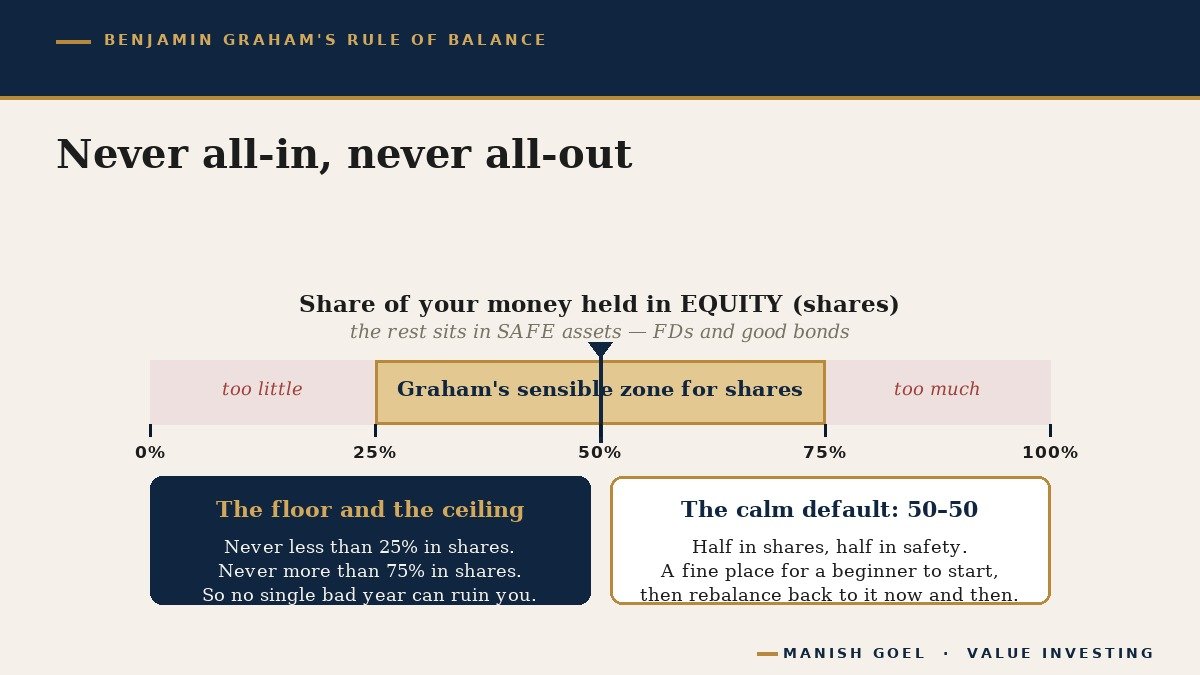

The father of value investing, Benjamin Graham — the teacher who later shaped Warren Buffett himself — gave ordinary people a wonderfully simple rule for all this. In his classic 1949 book The Intelligent Investor, Graham advised the everyday “defensive” investor (his name for a sensible person who does not want a second full-time job studying the market) to keep the balance between shares and safe assets within gentle limits: never less than 25%, and never more than 75%, of your money in shares — with the rest held in safe instruments like good bonds or deposits. The simplest version of all, he said, is a plain 50–50 split: half in shares, half in safety, adjusted only gently as your own needs change over the years.

Now comes the most useful part of Graham’s rule — what to do as prices move. Suppose you begin at a neat 50–50. A year later, shares have done well and now make up 60% of your money, while your safe part has slipped to 40%. Graham’s advice is calm and clear: gently bring it back to your chosen balance. You sell a little of what has grown too large (shares) and add to what has shrunk (safety). This simple habit is called rebalancing (resetting your mix back to its original target). Notice the quiet magic in it: without any prediction at all, rebalancing makes you do the single hardest thing in investing — trim a little after things rise, and add a little after they fall. The rule supplies the discipline so that you do not have to find it in the heat of the moment.

You may have heard what sounds like the opposite advice — that great investors such as Warren Buffett actually dislike too much spreading, and prefer to put serious money into just a few businesses they understand deeply. That is quite true. Buffett once said it plainly: “Diversification is protection against ignorance. It makes little sense if you know what you are doing.” But read his words with care, because they are kinder to the beginner than they first appear. He is speaking to the rare expert who can study a business inside-out and back his judgement with deep knowledge. For the rest of us — busy people with jobs and families, who cannot examine every company in fine detail — a sensible spread is exactly the right protection. Concentration is a sharp tool for the few who truly know; balance is the safe and steady path for everyone else.

The same idea, inside an Indian home

Let us bring this all the way home. The typical Indian family, as we saw at the start, keeps most of its wealth in gold and property. There is nothing wrong with either one — both have served families well for generations. But a household that owns only gold and a flat is, in Graham’s language, badly out of balance. Almost everything rides on two assets, and there is very little of the patient, growing engine that equity provides, and often too thin a cushion of ready safety for an emergency.

A more balanced home looks a little different. It keeps a few months’ expenses as an emergency fund in the bank, so a sudden hospital bill never forces a panicked sale. It holds a steady core in FDs or safe bonds. It keeps the family’s beloved gold. And — this is the part most often missing — it adds a growing slice of equity: shares of sound, well-run businesses, or a simple low-cost basket that holds many companies at once, bought patiently and held for the long run. The family does not abandon what it loves; it simply gives each part of its savings a proper job, so the whole plate is balanced.

The biggest temptation to resist is chasing whichever asset is hottest this year — rushing into gold after it has already jumped, or into shares after a thrilling rally, or into a plot of land because a cousin says he doubled his money on one. Asset allocation is the calm opposite of all that. Just as a wise farmer does not plant a single crop and then pray for exactly the right weather, a wise saver does not bet everything on one asset and pray for the right year. You decide your balance once, in a cool and unhurried moment, write it down, and then mostly leave it alone — rebalancing gently now and again, and letting the years do the rest.

How you can use this — three simple steps

You do not need a finance degree or a single complicated formula to put this to work. Three plain steps are enough for a lifetime.

One: decide your split on purpose. Choose a balance that suits your age, your goals, and how calmly you sleep when prices fall. A common idea taught for long-term goals is to hold a larger share in equity while you are young and have many years ahead of you, and to lean more on safe assets as a big goal draws near. Stay inside Graham’s sensible guardrails — roughly 25% to 75% in shares — so that you are never completely all-in nor completely all-out. There is no single “correct” number, and the best split is simply the one you can comfortably stick with through good years and bad. (This is general education to help you think, not personal advice for your exact situation.)

Two: rebalance about once a year. Mark one fixed date you will not forget — your birthday, perhaps, or every April when the financial year turns. On that day, glance at your mix. If one part has grown much larger than your target, trim a little of it and top up the part that has fallen behind. Once a year is plenty; you are not trying to time the market or catch its turns, only to walk your plate calmly back to the balance you chose.

Three: keep a cushion, automate, and do not chase. Before you invest a single rupee, set aside a few months’ living expenses as an emergency fund in the bank, so that a crisis never forces you to sell your investments at the wrong time. Then invest steadily and automatically wherever you can, so good habits run on their own. And gently ignore the endless noise about this year’s hottest asset. Balance, repeated patiently for many years, quietly does the heavy lifting that excitement and guessing never can.

Key takeaways

- Asset allocation means deciding, on purpose, how much of your money goes into each type of asset — shares, safe assets like FDs and bonds, gold, and cash. In one line: do not put all your eggs in one basket.

- Different assets rise and fall at different times, so owning a sensible mix makes your total wealth steadier than any single one alone. Nobel winner Harry Markowitz called diversification “the only free lunch in investing.”

- Benjamin Graham’s simple rule for ordinary investors: keep between 25% and 75% of your money in shares (a plain 50–50 is a fine place to start), and rebalance back to your target now and then.

- Rebalancing quietly forces good discipline — trimming a little after a rise and adding a little after a fall — without any need to predict the market.

- Most Indian families lean heavily on gold and property; adding a patient, growing slice of equity and keeping an emergency cushion brings the balance Graham taught a century ago.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.