Most Indian investors hear the word goodwill and instinctively reach for a forensic flashlight. Their training is correct, but it is incomplete. There are two goodwills in the investing universe — and the one that compounds your wealth is invisible on the balance sheet, written nowhere in the auditor’s report, and almost never discussed on Indian financial television. Warren Buffett devoted an entire appendix to this distinction in his 1983 Berkshire Hathaway shareholder letter, titled “Goodwill and its Amortization: The Rules and the Realities.” If you have read it, your investing changes permanently. If you have not, you are still flying half-blind. Today I want to translate that appendix into the language of an Indian small-cap investor in 2026, and then test the framework against Titan Biotech’s FY25 audited numbers.

The Two Goodwills

Accounting goodwill is the residual figure that lands on a balance sheet when one company pays more than fair book value to acquire another. It is mechanical, backward-looking, and cosmetic. It gets tested for impairment, occasionally written down, and contributes nothing to the operating economics of the business. When Indian investors say “watch the goodwill line in conglomerate acquisitions,” they are talking about this goodwill — and they are right to be cautious.

Economic goodwill is something altogether different. Buffett defines it, in essence, as the durable capacity of a business to earn returns on tangible operating capital that are far above the cost of replacing that capital. It does not appear on any balance sheet — not Indian GAAP, not Ind AS, not US GAAP. Yet it is the single most important driver of long-term equity returns. A business with deep economic goodwill can throw off cash year after year while reinvesting only a small fraction of it back into the operating base. A business without economic goodwill — the average commodity manufacturer, the average undifferentiated services firm — must keep feeding the machine just to stand still.

Buffett’s See’s Candies Lesson, Restated for India

Buffett’s 1983 appendix uses See’s Candies as the worked example. When Berkshire bought See’s in 1972 it had roughly $8 million of tangible operating capital and was earning about $2 million pre-tax — a 25 per cent pre-tax return on tangibles, exceptional even then. Over the next eleven years, See’s grew its pre-tax earnings to about $13 million, while requiring only modest incremental investment in physical assets. The accountants saw a stable, slightly growing tangible base. Buffett saw something else: a business sitting on enormous, unrecorded, inflation-resistant economic goodwill.

The Indian translation is straightforward. Visualise two hypothetical FY25 small-caps, each reporting ₹50 Cr of EBIT. Company X earns it on a tangible operating base of ₹100 Cr — a 50 per cent return on tangibles, signalling a brand, a process, a regulatory moat or a customer-stickiness advantage that the balance sheet cannot capture. Company Y earns the same ₹50 Cr on a tangible base of ₹400 Cr — a 12.5 per cent return on tangibles, signalling commodity economics. Both might trade at the same headline P/E. They are not the same business. Company X has economic goodwill the eye cannot see; Company Y has none.

Why Inflation Is the Decisive Test

Buffett’s most original insight in 1983 was about how the two goodwills behave under inflation. Pure inflation does not change real cash flows but does roughly double, over a long enough horizon, the rupee cost of replacing physical assets. For Company X above, doubling the replacement cost of its ₹100 Cr tangible base requires an extra ₹100 Cr over many years to keep real output constant — a real but manageable burden against ₹50 Cr of annual EBIT. For Company Y, doubling its ₹400 Cr base requires an extra ₹400 Cr — a number that absorbs the entire cash flow for the better part of a decade. Inflation is therefore not a uniform tax across the market. It is a progressive tax that punishes capital-heavy, low-return businesses and barely scratches the high-return franchise. Economic goodwill, in Buffett’s phrase, “floats with the price level” — it grows in nominal value at roughly the same pace as the surrounding economy, and it does so without demanding fresh shareholder capital. That is the entire game.

This is also why the popular Indian investor habit of looking only at headline RoE without normalising for the tangible operating base produces such bad reasoning. RoE flatters companies that have leveraged a small equity base; economic goodwill, in contrast, only respects the size and cleanliness of the tangible asset pool that the operating cash flow rests on. Buffett’s test is harsher and more honest.

How Indian Investors Should Use the Framework

Three working rules fall out of the 1983 appendix that I keep close at hand for Indian small-caps. First, never confuse acquired goodwill on the balance sheet with economic goodwill in the business — they are unrelated and frequently move in opposite directions. Second, the cleanest empirical signature of economic goodwill is a sustained pre-tax return on tangible capital that materially exceeds the long-term inflation rate plus the cost of capital, with no leverage doing the heavy lifting. Third, economic goodwill is destroyed silently — by undisciplined capital allocation, by acquisition mistakes, by reinvestment into low-return adjacencies — long before it shows up in reported numbers. Watching where management deploys retained earnings is therefore not optional; it is the goodwill audit.

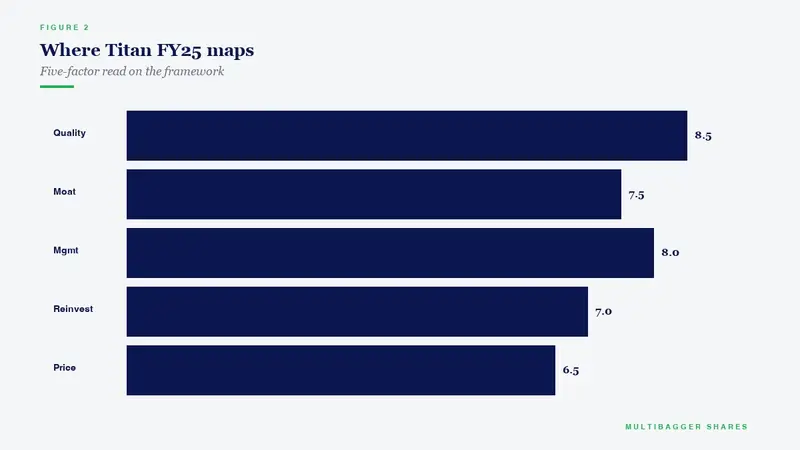

How Titan Biotech’s FY25 Numbers Illustrate Economic Goodwill

Now for the worked Indian case. Titan Biotech’s FY25 audited disclosures (BSE filing reference 524717) carry no acquired goodwill on the balance sheet — there has been no large acquisition that would have created an accounting-goodwill line. The interesting question, therefore, is whether the operating economics show evidence of economic goodwill of the See’s Candies variety. The audited markers tell that story with unusual clarity.

FY25 total revenue stands at approximately ₹214 Cr (the four quarterly print: ₹46.5 Cr → ₹54 Cr → ₹56 Cr → roughly ₹58 Cr), generated on a gross block of about ₹57 Cr — a tangible asset base extraordinarily small relative to the revenue it supports. The EBITDA margin band sits at ~18–22 per cent, which is the disciplined specialty-biotech range, well above any commodity-manufacturer template. CFO to Operating Profit conversion is ~103 per cent — cash generation actually exceeds reported operating profit, the gold-standard earnings-quality signal. Total borrowings are ~₹3 Cr against a strong net worth, putting debt-to-equity below 0.05x; this matters intensely in the goodwill conversation, because it removes financial leverage as an explanation for the high return on the tangible base. The depreciation-to-gross-block ratio of ~7 per cent is conservative, meaning the EBITDA is not being inflated by aggressive useful-life assumptions. CWIP of ~₹11 Cr indicates the next leg of capacity is being funded organically without a single rupee of fresh borrowing.

Layer on the qualitative quality markers. Exports were ~34.5 per cent of FY25 revenue across roughly 100 countries — a structurally diversified customer base that materially reduces single-customer concentration risk. Director remuneration of ~₹4.56 Cr is conservative against PAT. The board met 14 times in FY25 (against SEBI’s 4-meeting minimum), with an independent chairperson, indicating active oversight rather than ceremonial governance. Promoter holding has compounded over time without dilutive issuance.

Read through the Buffett 1983 lens, the picture is coherent: a small, clean tangible operating base; sustained returns on that base that are well above the long-term Indian cost of capital; cash conversion that exceeds book profit; no leverage doing the lifting; and management discipline in how retained earnings are being recycled. Those are the operating fingerprints — not balance-sheet entries — of a business that carries genuine economic goodwill. The accountants will never write it on the balance sheet. The compounding will write it on the share register, one financial year at a time.

The Takeaway

If you internalise only one Buffett framework this quarter, let it be this one. Stop reading the goodwill line on the balance sheet as the primary signal. Start reading the operating goodwill — the return on tangible capital, the inflation-resistance of the cash flow, the discipline in reinvestment — as the primary signal. Indian investors who learn to see economic goodwill where the balance sheet does not record it have access to the same edge that Buffett described in 1983, and the small-cap end of the Indian market is where that edge is most mispriced. The work is not glamorous. The reward, over a decade, is the difference between owning a business and owning a treadmill.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.