Value Investing — Educational Series

One afternoon in March 2020

On the afternoon of 23 March 2020, the Sensex closed near 26,000. The Sensex is simply a list of thirty large Indian companies whose combined movement tells us, roughly, which way the whole share market went. In the middle of January that same year, it had stood near 42,000. In about nine weeks, as the Covid lockdowns began, roughly forty percent of its value had disappeared. Newspapers called it a crash — a very fast, very deep fall in prices.

Now here is the part worth studying. That afternoon, lakhs of people owned shares in the very same good companies. A share is a small piece of ownership in a business — own a share, and a slice of that business is yours. The companies had not changed between January and March. Their factories stood where they always stood. Yet two very different things happened to their owners.

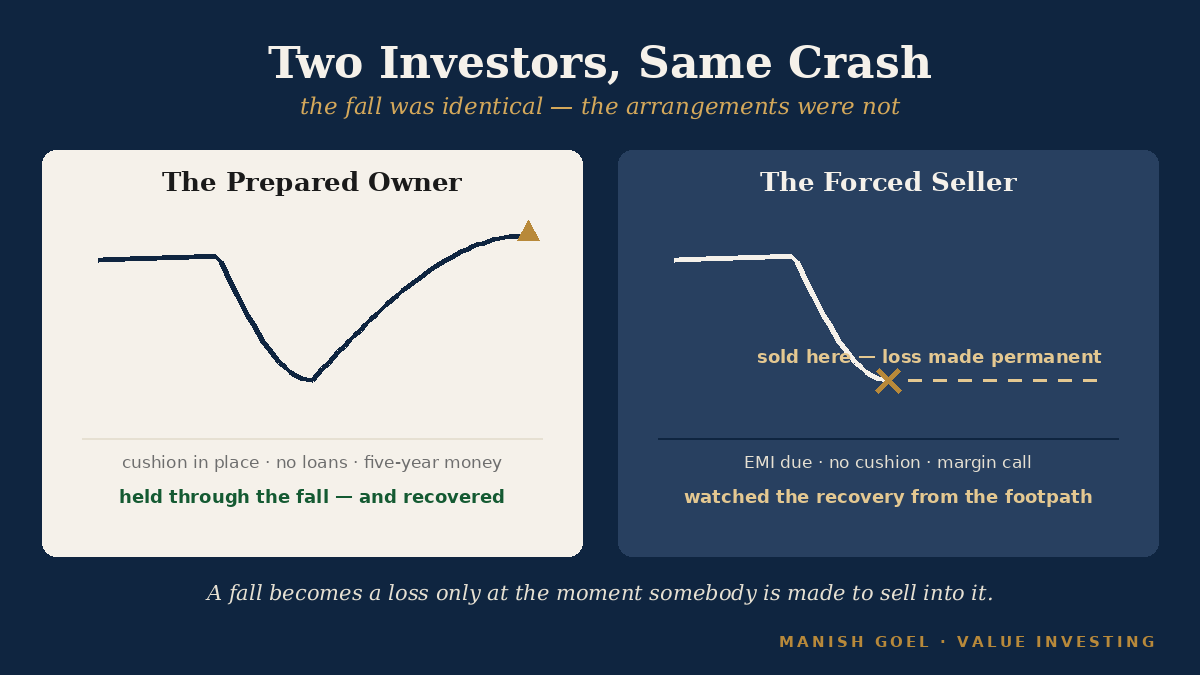

One group did not need to touch their shares. Their household expenses were safe in the bank, no loan was standing on their shoulders, and the money they had put into shares was money they would not need for years. They switched off the television and carried on with life. The other group needed money right then — a job had gone, an EMI (the fixed monthly instalment on a loan) was due, or a broker was demanding extra cash against borrowed positions. They had to sell, at whatever price the panic offered. By December 2020, the Sensex was not just back — it was setting new records. The first group rode home. The second group had already been thrown off the bus, at the bottom of the valley.

The difference between the two groups was never their intelligence, and never the shares they picked. It was the arrangement of their own pockets. That arrangement is today’s lesson.

What it really means

Benjamin Graham was Warren Buffett’s teacher, and his 1949 book The Intelligent Investor is still the most respected book ever written on sensible investing. In its famous eighth chapter, Graham wrote: “The true investor scarcely ever is forced to sell his shares, and at all other times he is free to disregard the current price quotation.”

Let us unpack that in plain words. A price quotation is just the number the market shouts at you each day — what someone is willing to pay for your share right now. Graham’s point is that this number is an offer, not an order. Think of a property dealer who walks past your house every single morning shouting a price for it. Some days his price is silly-high, some days it is insultingly low. Does his shouting force you to sell your house? Not at all. You sell only if you choose to. Shares work the same way. The market can only quote a price; it cannot make you accept it.

Graham then added a warning in the very next breath. The investor who lets himself be “stampeded or unduly worried by unjustified market declines”, he wrote, “is perversely transforming his basic advantage into a basic disadvantage”. Stampeded is exactly the right word — it is what a herd of cattle does when it panics and runs without looking. The small investor’s basic advantage is that he is allowed to stand still. Give that up, and you have volunteered for the herd.

Only one thing can turn the market’s daily shouting into a real command: your own need. If the school fee is due and there is no other money, the shouted price becomes your selling price, however unfair it is. So Graham’s rule quietly points the torch away from the market and towards us. The small investor’s greatest advantage is freedom — no boss, no deadline, no one who can force a sale. But that freedom is not automatic. It has to be arranged in advance, the way an umbrella has to be bought before the monsoon, not during the first downpour.

Notice something else about this rule. It never asks whether the market is high or low, or whether any share is cheap or costly. It asks only about your own pocket. Get the pocket right, and you can own good businesses calmly through any weather.

Why it works — and the three things that secretly break it

Long-term investing runs on compounding — the process where your returns start earning their own returns, the way interest earns interest in a bank deposit, or a small snowball rolling downhill keeps adding layer upon layer. Compounding has one strict demand: unbroken time. Every forced sale is a hand that stops the rolling snowball and melts a part of it permanently.

Here is the heart of the logic. When a strong, well-run business sees its share price fall in a general panic, that fall is usually temporary — the business keeps earning, and sooner or later the price follows the business. A fall becomes a permanent loss only at the moment somebody sells into it. Think of two farmers. One grows tomatoes; whatever the mandi offers on harvest day, he must accept, because tomatoes rot by tomorrow. The other grows wheat and owns a small warehouse; if today’s price is poor, he can lock the warehouse and wait for a fair one. Same market, same season — but the warehouse turns a forced seller into a patient one. Your financial arrangements are that warehouse.

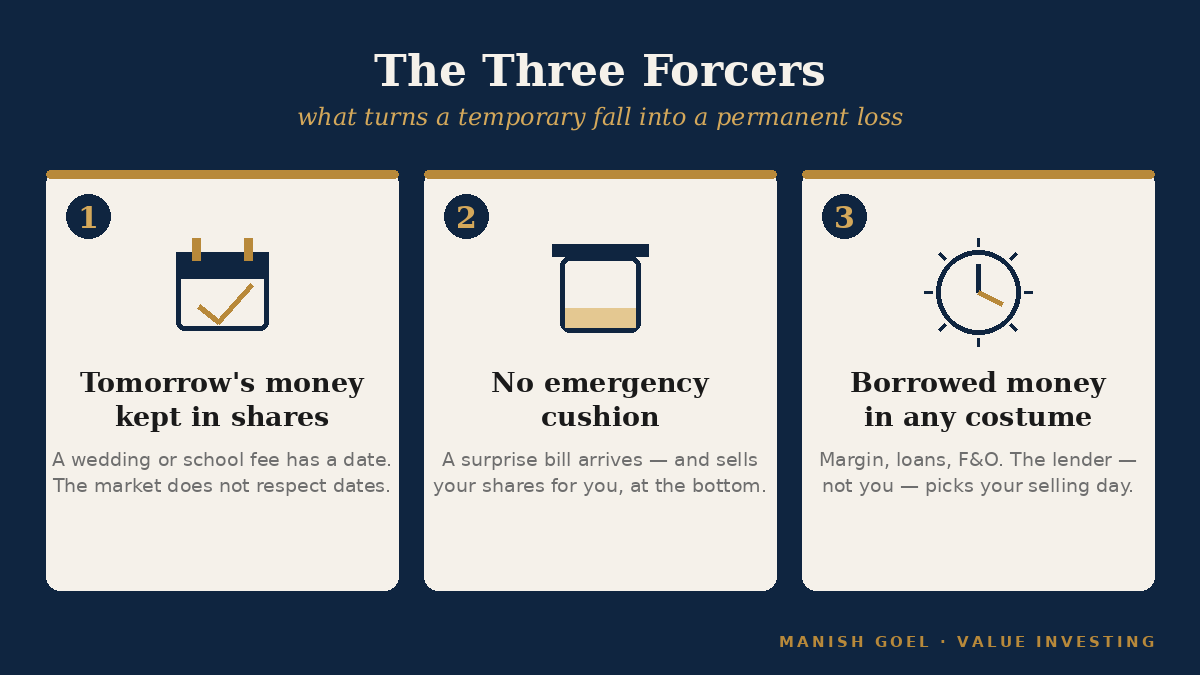

Three habits quietly demolish this warehouse, and almost every ruined investor you will ever meet was standing on at least one of them.

First, putting tomorrow’s money into shares. Money needed within the next few years — a wedding in the family, school admission, the down payment on a flat — has a fixed date. The market does not respect dates. It may be in one of its dark moods in exactly that month, and you will have to sell into the gloom.

Second, having no emergency cushion. Life sends surprise bills — a hospital stay, a job loss, an urgent repair. An emergency fund is simply six months or so of your household expenses kept where it is safe and instantly reachable, such as a bank fixed deposit (FD) or a liquid fund (a type of mutual fund meant for parking money safely for short periods). Without this cushion, your shares themselves become the emergency fund — and emergencies have a cruel habit of arriving in the same season as market crashes.

Third, borrowed money. This includes margin funding (a loan from the broker against your shares), personal loans taken to buy shares, and the heavy hidden borrowing inside F&O — futures and options, which are contracts that bet on price movements using many times your own money. Borrowed money carries a clock: the interest meter runs, and the lender can demand repayment at the worst hour. Good investing carries a calendar, not a clock. The two cannot live together.

Warren Buffett gave the strongest warning on this in his 2017 letter to shareholders. He showed that the share price of his own company, Berkshire Hathaway — run by the most admired investor alive — had fallen between 37 and 59 percent four separate times over about fifty years. His conclusion: “There is simply no telling how far stocks can fall in a short period.” Even if a borrower is not immediately in danger, he warned, the mind becomes “rattled by scary headlines and breathless commentary” — and, in his words, an unsettled mind will not make good decisions.

A real example or two

Return to India, March 2020. The fall from about 42,000 to about 26,000 felt endless while it was happening. Yet within roughly eight months the Sensex had climbed back above its January level, and by December it was making new all-time highs. Investors who owned good businesses and were not forced to sell ended that frightening year ahead. Investors who had to sell in March — because the EMI was due, the cushion was missing, or the broker’s margin call came — took the whole loss and then watched the recovery from the footpath. The crash did not punish the owners of good businesses. It punished the unprepared wallet.

Second story. In the darkest months of the 2008 global banking crisis, Buffett wrote to his shareholders: “We never want to count on the kindness of strangers in order to meet tomorrow’s obligations. When forced to choose, I will not trade even a night’s sleep for the chance of extra profits.” Berkshire, sitting on one of the largest piles of ready cash in the corporate world, still refuses to depend on anyone’s mercy. Read that again slowly. The most successful investor in history keeps an umbrella big enough that he never has to knock on a stranger’s door in the rain. If he needs that discipline, a beginner with one salary and one portfolio needs it many times more.

And a sobering piece of Indian evidence from the other side of the road. In September 2024, SEBI — the government body that regulates our share markets — published a study of individual F&O traders, the crowd chasing quick profits with borrowed speed. Between FY22 and FY24, 93 percent of more than one crore such traders lost money, an average of about two lakh rupees each, and more than 1.8 lakh crore rupees in total went up in smoke. Nine out of ten borrowed the market’s clock; the clock collected its fee. The patient owner and the leveraged trader stand in the same market — but only one of them can be ordered to sell.

How you can use it

The whole rule turns into three simple habits. None of them needs any skill in picking shares; they only need to be done in the right order.

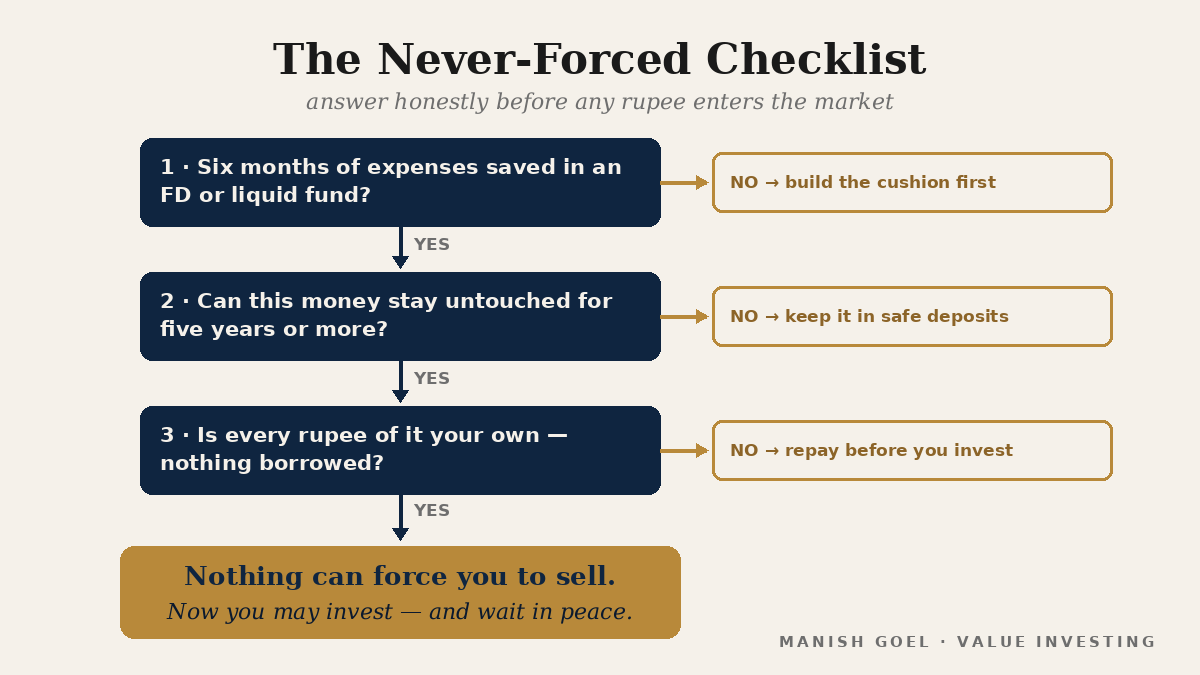

One — build the cushion before the castle. Before your first serious rupee enters the share market, keep about six months of household expenses in an FD or liquid fund. This money will look lazy. It is not. It is the fee you pay for the right to wait — the warehouse that lets every other rupee stay invested through the worst season. A family emergency should meet your savings, never your shares.

Two — give the market only your five-year money. Before investing any amount, give the rupee a name and a date: this is for retirement in 2050, this is for the child’s education in 2032. Anything whose date falls within about five years — the wedding, the admission, the house registration — stays in safe deposits, whatever excitement the market is offering. Shares reward time generously and punish deadlines brutally.

Three — never own shares with borrowed money. No margin funding, no personal loan routed into the market, no F&O shortcuts dressed up as strategy. A simple test: if a plan works only because borrowed money makes it bigger, it is not investing; it is hoping, with a deadline attached. The kirana shopkeeper who keeps his cash tin full never has to sell his shop cheap in a bad month. Be that shopkeeper.

And one small habit that ties all three together. Before every purchase, write a single line in your notebook: “If this price halves next year, nothing in my life will force me to sell.” If you cannot write that sentence truthfully, the problem is not the share — it is the pocket. Fix the pocket first.

Key takeaways

- A market price is an offer, not an order. Nobody on earth can force you to sell a good business at a bad price — except your own arrangements.

- Three things create forced sellers: short-date money kept in shares, a missing emergency cushion, and borrowed money in any costume.

- Order of operations: six months of expenses in an FD or liquid fund first; only five-year-plus money into equity; zero borrowed rupees in the market.

- Falls in good businesses are usually temporary; selling into the fall is what makes them permanent. The 2020 crash recovered within months — for those still seated.

- Arrange your money so that every crash becomes just a season to sit through, never an emergency to sell into. That is Graham’s quiet gift to the small investor.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.