Value Investing — Educational Series

Imagine a farmer in a village waiting for the perfect day to sow his seeds. He worries the rain might come too early, or too late, or be too heavy. So he waits. He waits for a sign that the monsoon is “exactly right.” Meanwhile his neighbour simply sows on a normal day, trusts the season, and gets on with it. When the harvest comes, the neighbour’s field is full and green. The careful farmer, still waiting for the perfect moment, has an empty field. He was not lazy — he was just trying too hard to time something that cannot be timed.

This is one of the oldest and most expensive mistakes in the stock market. Beginners often believe the secret to wealth is to buy at the very bottom and sell at the very top — to jump in and out at clever moments. This is called market timing (trying to guess the best moments to buy and sell). The opposite habit — simply staying invested for many years through the ups and downs — is called time in the market. Today, in very simple words, let us understand why time in the market almost always beats timing the market, and why this single idea can quietly decide how wealthy you become.

None of this is about whether the market is “cheap” or “expensive” today. It is about a simple truth: the biggest gains tend to arrive in a tiny handful of days, nobody can predict which days those will be, and if you are sitting on the sidelines when they come, you miss most of the reward.

What “timing the market” really means

When people try to time the market, they are trying to predict its short-term direction. They sell because they feel a fall is coming, plan to buy back lower, and hope to skip the painful days. It sounds clever. Who would not want to step out before a crash and step back in at the bottom?

The problem is that to win at this game you must be right twice, and right by luck both times. First you must sell at the right moment, before the fall. Then you must buy back at the right moment, before the recovery. Get either one wrong — and almost everyone does — and you end up worse off than if you had simply done nothing. A correction (a fall of around 10% in prices) or a full crash (a much steeper fall) feels obvious only after it is over. While it is happening, nobody rings a bell to tell you the bottom has arrived.

Think of a batsman in a long cricket innings. The patient player who stays at the crease, ball after ball, slowly builds a big score. The restless player who keeps stepping out of his crease to play a fancy shot eventually misses one and is bowled. Staying in is boring, but staying in is how runs are made. The stock market rewards the same patience: the longer you stay properly invested, the more the game tilts in your favour.

Why timing almost never works

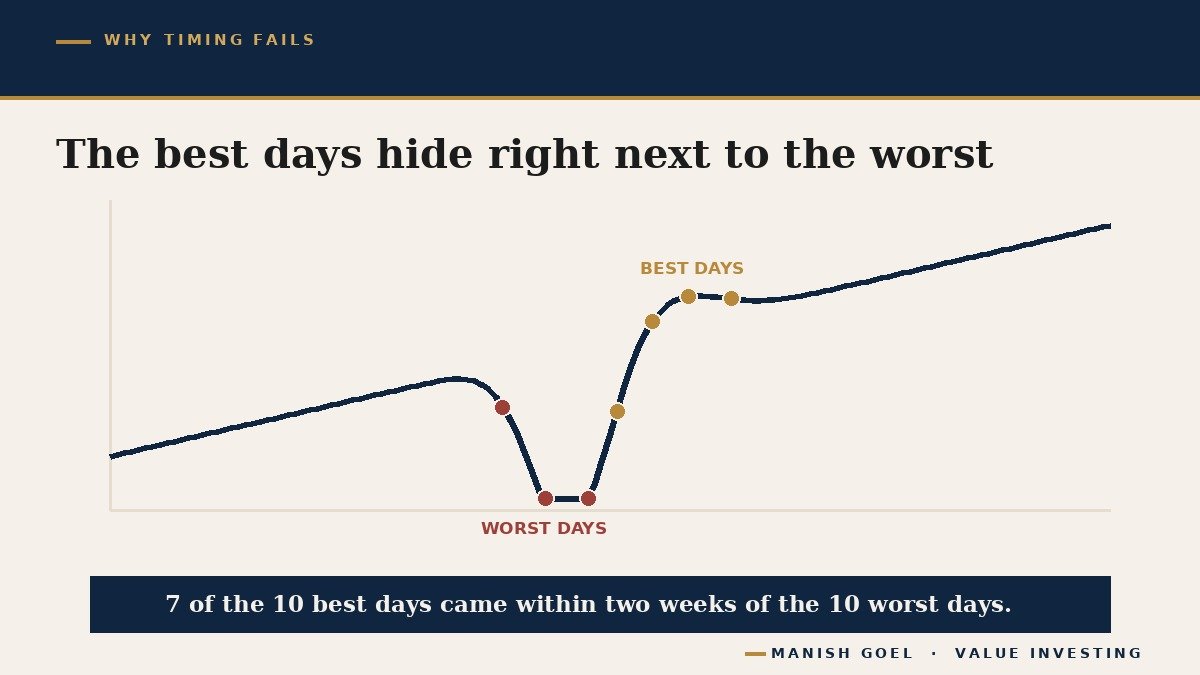

Here is the heart of the matter, and it surprises almost everyone the first time they hear it. The stock market does not rise smoothly, a little every day. Instead, a huge slice of its long-term gains comes from a very small number of explosive days — and those best days are tangled up right next to the worst days.

Studies of the American stock market over the twenty years from 2005 to 2024 found something remarkable: seven of the ten best single days happened within about two weeks of the ten worst days. In India it is much the same — over the last two decades, seven of the ten best days for the Nifty 50 (a basket, or index, that tracks 50 of India’s biggest companies) also came within two weeks of the ten worst days. The strongest up-days do not arrive on calm, sunny afternoons. They arrive in the middle of the storm, often the day after a frightening fall.

Now you can see the trap. The investor who panics and sells during a crash is trying to dodge the worst days. But because the best days sit right beside the worst days, he almost always ends up out of the market for the powerful rebound too. He locks in the pain and skips the recovery. The COVID-19 fall of March 2020 was a perfect example: Indian and global markets dropped sharply in a matter of weeks, terrifying everyone — and then staged one of the fastest recoveries in history. Many of that year’s best days came within days of its worst. Anyone who sold in fear at the bottom watched the rebound from the sidelines.

This is why the legendary fund manager Peter Lynch warned: “Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.” Read that twice. The fear of a fall — and all the selling and waiting it causes — has cost ordinary people more than the falls ever did.

The real cost of missing just a few days

Let us put real numbers on it, because the size of the difference is hard to believe until you see it. These are simple historical facts about whole markets — not a tip to buy or sell anything.

In the United States, J.P. Morgan studied what happened to $10,000 invested in the broad American market on the first trading day of 2005 and left completely untouched until the end of 2024. Staying fully invested through every crash and scare, that $10,000 grew to about $72,000 — a healthy return of roughly 10% a year (the steady yearly rate, called the annualised return). But an investor who missed just the ten best days over those twenty years ended with only about $33,000 — less than half. Miss a few dozen of the best days, and the gain very nearly vanishes altogether. Ten days out of roughly five thousand trading days decided whether the money doubled, tripled, or barely grew.

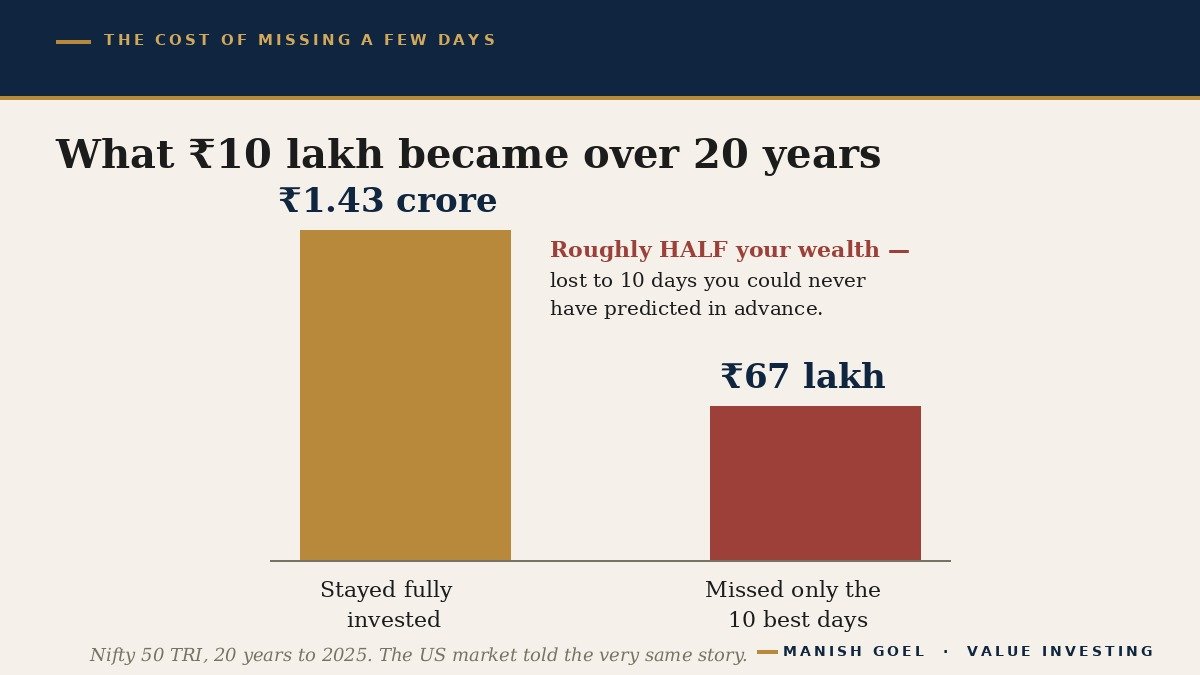

India’s story is just as striking. Studies of the Nifty 50 over the twenty years to 2025 found that ₹10 lakh, left fully invested through every panic, grew to around ₹1.43 crore. The very same ₹10 lakh, if the investor had missed only the ten best days, grew to just about ₹67 lakh — once again, roughly half. Half your lifetime’s wealth, lost not to a crash, but to being absent for ten good days you could never have predicted in advance.

This is the quiet power of compounding (earning returns on your past returns, so your money snowballs over time) — and the cruel cost of interrupting it. Compounding only works if you leave the snowball rolling. Every time you jump out, you stop the snowball, and you risk being out of the market on exactly the days that matter most. The market does not reward the clever or the busy; it rewards the present.

What the great investors actually do

The investors who have built lasting fortunes are almost unanimous on this point, and their honesty is refreshing. Jack Bogle, who founded one of the world’s largest investment firms, put it bluntly: “The idea that a bell rings to signal when investors should get into or out of the market is simply not credible. After nearly 50 years in this business, I do not know of anybody who has done it successfully and consistently.” Notice that he is not saying it is hard — he is saying that after a lifetime among the smartest professionals in the world, he never met a single person who could do it reliably.

India’s own market history teaches the same lesson. The late Rakesh Jhunjhunwala, often called India’s Warren Buffett, lived through the crashes of 1992, 2000, 2008 and 2020. He did not get rich by darting in and out around each of these falls. He grew his wealth by backing businesses he believed in and holding them, with conviction, for years and even decades, while staying invested through every storm. His real edge was not a magic sense of timing — it was patience and staying power.

For an ordinary investor, the simplest way to copy this discipline already exists: the SIP (Systematic Investment Plan — investing a fixed sum every month, no matter what the market is doing). When you invest the same amount every month, you stop trying to guess the right day entirely. You automatically buy a little when prices are high and a little more when prices are low, and — most importantly — you are always present for the good days, because you never left. The SIP turns the impossible job of timing into the easy habit of showing up.

How you can use this idea

You do not need any special skill to benefit from this. You only need to resist the urge to be clever. Here are three simple, practical habits any beginner can follow.

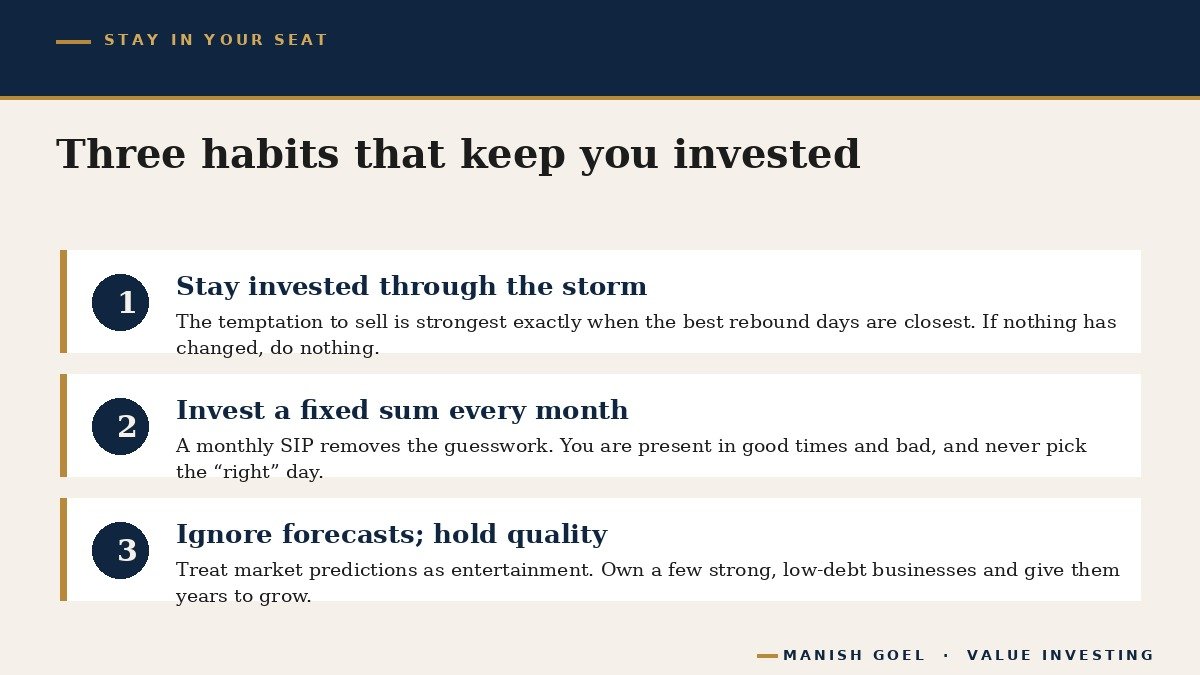

First, stay invested — especially when it feels scariest. The temptation to sell is strongest exactly when a crash is in full swing, which is precisely when the best rebound days are closest. If you own good businesses and your reason for owning them has not changed, doing nothing is usually the wisest action. Sitting still is hard, but the numbers above show it is richly rewarded.

Second, invest a fixed amount every month and automate it. A monthly SIP removes emotion and guesswork from the decision. You are no longer asking “is today a good day?” — you are simply present every single month, in good times and bad. Over the years, this steady presence quietly does what frantic timing never can.

Third, ignore short-term forecasts and own quality for the long run. Television and social media are full of confident predictions about where the market will go next week. Treat them as entertainment, not instructions. Your job is not to guess the next wobble; it is to own a few high-quality businesses — companies with low debt, real cash flows and honest managers — and then give them many years to grow. Time, not timing, is what turns good businesses into real wealth.

Notice that none of this asks you to predict anything. We are not trying to call the top or the bottom, and we are not judging whether prices are cheap or dear. We are simply choosing to be present — to let good businesses and the patient magic of compounding do the heavy lifting, over a span of years that is long enough for them to work. The farmer who sows on an ordinary day and trusts the season ends up with a full field. So does the investor who stays in his seat.

Key takeaways

- Trying to jump in and out at clever moments is called market timing; simply staying invested for years is called time in the market — and time in the market almost always wins.

- A huge share of all long-term gains comes from a tiny number of explosive days, and seven of the ten best days tend to arrive within two weeks of the ten worst days.

- Missing just the ten best days over twenty years roughly halved long-term wealth — both in the US market ($72,000 falling to about $33,000) and in India’s Nifty 50 (₹1.43 crore falling to about ₹67 lakh).

- Selling in fear during a crash usually means missing the powerful rebound, because the best days hide right next to the worst — as the COVID-19 fall and recovery of 2020 showed.

- A monthly SIP removes the guesswork: invest a fixed sum every month, stay present through every storm, and let compounding work on quality businesses over many years.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.