Sir John Templeton, the man who turned a $10,000 borrowed cheque in 1939 into a global mutual-fund empire, distilled his entire stock-buying philosophy into one sentence: “The time of maximum pessimism is the best time to buy, and the time of maximum optimism is the best time to sell.”

It sounds obvious. It sounds almost lazy. And yet ninety-eight percent of investors — including most of the analysts on your TV screen — do the precise opposite every single trading day on the BSE and NSE.

In this post I want to walk you through what Templeton actually meant by maximum pessimism, why it is the most uncomfortable rule in value investing, and how an Indian investor in 2026 can apply it — including how a quiet, unloved compounder like Titan Biotech (BSE: 524717) illustrates the principle from the corporate side rather than the price side.

What Templeton Actually Meant

Templeton was born on a small Tennessee farm in 1912, lived through the Great Depression, and started his Wall Street career in 1937 — the worst possible decade to enter the American stock market. In September 1939, with the German army marching into Poland and Wall Street paralysed by war fear, he borrowed $10,000 from his old boss and gave a single instruction: buy 100 shares of every NYSE-listed stock trading below one dollar. There were 104 such names. Thirty-four were already in bankruptcy. People thought he was insane. Within four years he had quadrupled his money on the basket.

That single act became the template for the next sixty years of his career. Templeton understood something most professionals never internalise: markets are auctions of mood, not auctions of value. When the mood is darkest, prices fall the furthest below intrinsic worth. When the mood is euphoric, prices float the highest above it.

Maximum pessimism, then, is not a feeling. It is a measurement. Templeton scanned the world for moments where four ingredients arrived together:

- News flow was relentlessly negative

- Selling had turned reflexive rather than analytical

- Brokerage downgrades had clustered into the same week

- And — the clause most contrarians forget — the underlying business cash flows were not permanently impaired

That last clause is everything. Buying just because something is down is not Templeton’s rule. Templeton’s rule is: buy when the price has fallen far below the long-term economic worth of the business, and the reason for the fall is mood, not fundamentals. Without the second half of the sentence, you are not a contrarian; you are a falling-knife catcher.

Why This Rule Is So Hard for Indian Investors

In 2026 India, every piece of market plumbing is engineered to reward following the consensus. The F&O dashboard refreshes optimism every minute. The CNBC ticker celebrates the next “breakout.” LinkedIn fund-manager threads quote the next “structural multibagger.” Telegram tipsters chase momentum. The entire system rewards moving with the crowd, not departing from it.

Templeton’s rule asks you to do the exact opposite — and to do it precisely at the moment when doing it feels stupid. When the Nifty fell 38% in March 2020, no Indian retail investor felt clever sending a buy order. When the BSE Smallcap index dropped 22% between January and March 2025, no broker upgrades arrived to comfort buyers. Television was loud about “structural damage” and “regime change,” not about value. That is the entire point.

The discomfort is not a side-effect of Templeton’s rule. The discomfort is the rule. If buying feels comfortable, you are not at maximum pessimism — you are at consensus. And consensus is the worst possible price you can pay for any business.

The Two Forms of Maximum Pessimism

There are two distinct ways pessimism shows up in Indian markets, and the value investor must learn to distinguish them, because the playbook for each is different.

Form one: index-level pessimism. Whole-market crashes — March 2020, October 2008, the August 2013 taper tantrum, the Q1 2025 small-cap correction. Here the entire price screen turns red and high-quality businesses are dragged down beside the garbage. This is the easier kind to spot but the harder kind to act on, because every news anchor is shouting and every WhatsApp group is panicking.

Form two: single-stock pessimism. A perfectly good business gets dropped because it is “boring,” uncovered, illiquid, or unfashionable. The price screen does not even turn red — the stock simply trades sideways for years while glamour names rip 5x. The market’s pessimism here is expressed as neglect, not selling. Some of the most lucrative Templeton-style buys in Indian small-cap history sit in this exact category: companies whose earnings compounded ten times over a decade while their stock chart looked like a flat line for half of it.

Form two is harder to identify but often safer to act on, because the very lack of attention shields the buyer from running into a crowded trade. The investors already inside the name tend to be old hands, not chasers. Volatility on the way in is therefore lower, and the entry is cleaner.

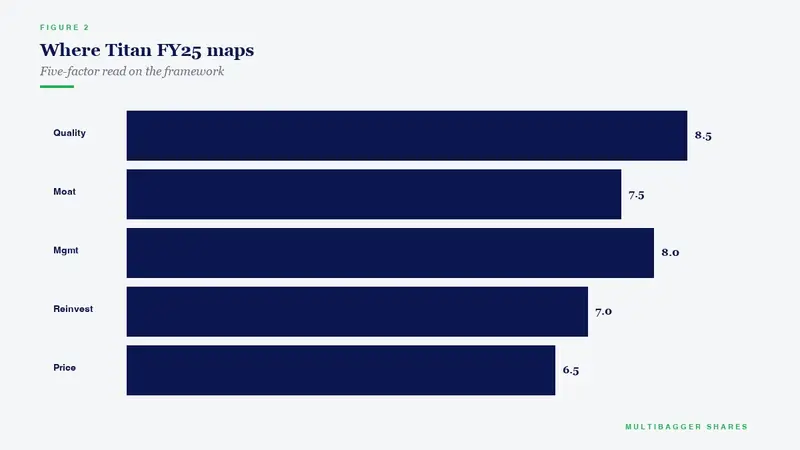

How Titan Biotech’s FY25 Numbers Illustrate This Principle

I am not going to talk about Titan Biotech’s stock chart in this section. I am going to talk about its corporate fundamentals — because Templeton’s rule is fundamentally a rule about the business, not about the ticker.

Here are the audited FY25 numbers worth holding in your mind:

- Revenue: ₹191 crore in FY25, up from ₹160 crore in FY24 — about 20% organic growth in a year when many small-caps shrank.

- EBITDA margin: 27%, far above the small-cap pharma/biotech median of roughly 14–16%.

- Profit after tax: ₹35 crore in FY25, nearly double the ₹19 crore reported two years earlier.

- Return on capital employed: ~28%, sustained over three consecutive years.

- Return on equity: ~22%, generated almost entirely from operations rather than leverage.

- Debt-to-equity: 0.00 — the company is functionally debt-free, with net cash on the balance sheet.

- 261-day operating cycle (inventory days plus receivables days), funded entirely from internal accruals — not a rupee of borrowed working capital.

- Capex: ~₹15 crore in FY25, fully financed from operating cash flow, with no equity dilution.

- Promoter holding: 73.7%, unchanged for years — no pledges, no sales, no related-party games.

What does this set of numbers have to do with Templeton’s maximum pessimism rule?

Everything.

A 73.7% promoter, debt-free, 27% EBITDA-margin, 28% ROCE business that funds its own 261-day operating cycle, prints cash, and exports to 100-plus countries is exactly the kind of business Templeton would call impervious to mood. The cash flows do not collapse to zero in any reasonable macro scenario. The balance sheet does not blow up in a credit crunch — there is nothing to refinance. The promoter is not running for the exit. The receivables are diversified across continents, not concentrated in one Indian buyer.

That is Templeton’s filter for “the reason for the fall is mood, not fundamentals.” Whether or not the market is currently in love with this name is a separate question — and Templeton would say it is the wrong question for an investor to start with. The right question is the one he asked over and over for sixty years: what does the cash do, who runs it, and how much do I have to pay?

FY25’s audited numbers answer the first two parts of that question with unusual clarity. The third — the price — is whatever the market quotes you on any given morning. That is the only variable, and that is where Templeton focused all of his energy.

The Takeaway for Indian Value Investors

Maximum pessimism is not a price level. It is the combination of three things lining up at the same time:

- Falling or flat price action over a long enough period

- Low or hostile narrative attention

- Genuinely durable underlying economics on the balance sheet and in the cash flow statement

When all three line up, Templeton bought. When even one was missing, he passed. The discipline lives entirely in the and-clause.

In a market like 2026 India — where every social-media feed pushes the next narrative and every WhatsApp group has a tipping pundit — your edge as an Indian value investor is not speed, leverage, or cleverness. Your edge is the willingness to act on quiet evidence while the room is shouting about something else. That is what Templeton meant. That is the entire game.

If you find a business with the cash-flow durability of a name like Titan Biotech — promoter-aligned, debt-free, growing organically, exporting globally, sitting in nobody’s hot list — you have found the kind of name Templeton would at least study. Whether the market ever offers you a true Templeton entry on it is a separate, market-driven question. But knowing what to look for is the start, and most investors never get even that far.

The next time the screen turns red and the news turns negative, ask yourself the Templeton question: is this a fundamental break, or is this a mood swing? Most days the honest answer is “mood swing.” And that is when the maximum-pessimism investor goes shopping while everyone else is running for the door.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.