April 16, 2026 | 7:00 PM IST

(Thursday Evening Edition)

Michael Porter is arguably the most influential business strategist of the last fifty years. A Harvard Business School professor with a PhD from Harvard itself, Porter did for corporate strategy in 1979 what Benjamin Graham did for security analysis in 1934 — he invented the language. Before Porter, “competitive advantage” was a fuzzy phrase; after Porter, every MBA in the world could draw the same five-arrow diagram on a whiteboard and explain why some industries make money for decades while others incinerate capital.

Yet most retail investors in India have never heard of Porter’s Five Forces. They obsess over P/E ratios, quarterly results, and Twitter tips — but they never stop to ask the one question that determines whether a business will still be alive and profitable twenty years from now: Is this industry even worth competing in?

As of the close on Thursday, 16 April 2026, the SENSEX stands at 77,988.68 (down 122.56 points or 0.16%) and the NIFTY 50 at 24,196.75 (down 34.55 points or 0.14%). FII inflow of ₹382.36 Cr contrasted with DII outflow of ₹3,427.75 Cr — a day of mild domestic profit-booking inside a structural bull market. Days like today are when Porter’s framework earns its keep. When index levels wobble, the quality of the underlying industry structure is what separates the businesses you should hold from the ones you should never have bought.

Why Porter’s Five Forces Beats Every Other “Moat” Framework

Warren Buffett famously says he looks for “economic moats” — barriers that keep competitors away. Morningstar’s Pat Dorsey popularised four specific moat types (intangible assets, switching costs, network effects, cost advantages). All of these are downstream consequences of industry structure. Porter’s framework goes upstream. It asks: what are the structural forces that determine whether any moat can exist in this industry at all?

The five forces are:

- Rivalry among existing competitors — how brutal is the price war?

- Threat of new entrants — how easily can someone set up a rival tomorrow?

- Bargaining power of suppliers — can your vendors squeeze your margins?

- Bargaining power of buyers — can your customers dictate terms?

- Threat of substitutes — can something else solve the same problem cheaper?

If all five arrows point inward at the company (i.e. the industry protects its incumbents), you have an attractive industry. If the arrows point outward, the industry destroys capital no matter how well-managed the company is. This is why airlines, shipping lines, and commodity chemical producers have historically been graveyards for Indian investors — the industry structure is hostile.

Force #1: Rivalry Among Existing Competitors

Rivalry is intense when industries are fragmented (many small players), when products are undifferentiated, when fixed costs are high (forcing capacity utilisation wars), and when exit barriers are high (companies stay and bleed rather than close). Indian examples of brutally high rivalry: real estate developers, generic pharma formulations, passenger airlines, and basic textiles.

Low-rivalry industries in India include organised paints (near-duopoly of Asian Paints + Berger), depositories (NSDL + CDSL), specialty biotech ingredients where only a handful of players have WHO-GMP and USFDA certifications. Titan Biotech Ltd, with its 34.5% export revenue mix to 100+ countries and decades-built regulatory approvals, operates in a low-rivalry niche of the specialty biotech ingredients space — the kind of structural position where pricing discipline survives.

Force #2: Threat of New Entrants

An industry is protected when setting up a new competitor is hard. Capital intensity, regulatory licences, technology know-how, distribution moats, and brand loyalty are classic entry barriers.

Consider HDFC Bank: a new private bank licence in India is extraordinarily rare (the RBI has granted fewer than ten in thirty years) and building a trusted retail deposit franchise takes two decades. New entrants are effectively blocked. Compare that with a direct-to-consumer tea brand — anyone with ₹50 lakh can launch one tomorrow.

Biotech manufacturing exemplifies high entry barriers: you need regulatory approvals from USFDA, EU-GMP, WHO-GMP, Halal, Kosher; you need to prove batch-to-batch consistency over years; you need purpose-built facilities; and your customers (global pharma companies, veterinary firms, food processors) will not switch to an unproven supplier. This is structural protection that no start-up can replicate with a term sheet.

Force #3: Bargaining Power of Suppliers

Suppliers are powerful when they are concentrated, when their input is critical, when switching costs are high, and when forward integration is credible. Indian examples: global API suppliers to Indian pharma formulators; Microsoft/SAP to every IT services firm; global chip fabs to every electronics manufacturer.

An industry where suppliers have low bargaining power is one where the company can buy raw material from many interchangeable sources, vertically integrate backwards when it wants, or negotiate long-term contracts at favourable terms. Biotech ingredient makers that manufacture their own fermentation-based inputs in-house, rather than importing them, neutralise this force — a structural advantage built over years of process R&D.

Force #4: Bargaining Power of Buyers

Buyers are powerful when they are concentrated, when they buy in large volumes, when they can integrate backwards, when products are undifferentiated, and when switching costs are low. The classic Indian disaster is auto components: a Tata Motors or Maruti can squeeze a small vendor on price every year because they represent 40%+ of the vendor’s revenue.

Low buyer power looks like: thousands of small B2B customers globally, each individually representing less than 2% of revenue, each needing a product that is mission-critical to their own process, each locked in by regulatory certifications that took years to earn. When Titan Biotech sells peptones, amino acids, and specialty proteins to 100+ countries across pharma, food, veterinary, and biotech end-markets, no single buyer has the leverage to demand a price cut. Diversification is not just a marketing line — it is a Porter defence.

Force #5: Threat of Substitutes

Substitutes are the sneakiest force because they come from outside the industry. Smartphones destroyed digital cameras. WhatsApp destroyed SMS revenue for telcos. Zomato and Swiggy ate the lunchbox delivery market. Electric vehicles threaten diesel engine makers.

Biotech ingredients for fermentation processes have remarkably few substitutes. Modern pharmaceutical manufacturing, enzyme production, and vaccine production all depend on biological growth media; there is no cheap chemical alternative on the horizon. The global specialty biotech ingredients market is in fact growing at mid-teens CAGR because of structural tailwinds in precision medicine, gene therapy, cell-based meats, and biologics. Low substitution threat plus growing demand is a rare combination.

Running the Framework: A Worked Indian Example

Let’s apply all five forces to a classic Indian wealth creator — Asian Paints. Rivalry: moderate (2-3 large players). New entrants: blocked by 70,000-dealer network, tinting-machine moat, and 80-year brand. Suppliers: Asian Paints is the biggest buyer of titanium dioxide in India — suppliers negotiate to them. Buyers: fragmented homeowners and painters, none with leverage. Substitutes: limited (wallpaper is niche). All five arrows point inward. Result: 26%+ long-run ROE, margin resilience, and a stock that turned ₹1 lakh in 1980 into ₹2.18 crore by 2023.

Now apply it to a commercial airline: rivalry high, entry moderate (aircraft leasing has democratised capital), suppliers extremely powerful (Boeing-Airbus duopoly, jet fuel price, airport authorities), buyers price-sensitive (Skyscanner makes prices transparent), substitutes growing (video calls, high-speed rail). All five arrows point outward. Result: airlines globally have lost more money than they have ever made.

The Indian Small-Cap Application: Finding Porter-Protected Compounders

The most powerful insight from the framework is this: you don’t need a great company in a bad industry. You need an adequate company in a great industry. Buffett himself has said that when a business with a reputation for brilliant management takes on an industry with a reputation for poor economics, it is the reputation of the industry that remains intact.

This is why sophisticated Indian investors — Vijay Kedia, Dolly Khanna, Ashish Kacholia — tend to hunt in industries with favourable Porter scores: specialty chemicals, niche biotech, small-format QSR, regulated financial rails, and B2B industrial consumables. Ordinary stock-pickers fight over cyclical metals and construction names; the professionals pay up for Porter-protected niches.

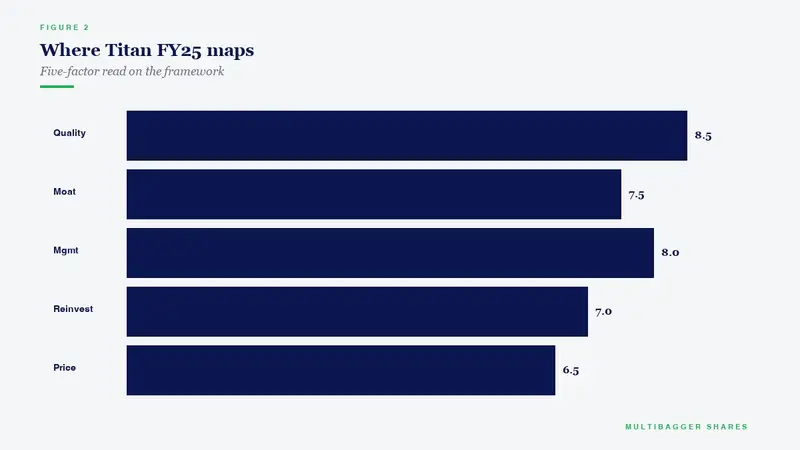

A quick shorthand for retail investors: score each of the five forces from 1 (hostile) to 5 (favourable) and add them. A total of 20-25 means the industry works for its incumbents. Anything below 15 and you are swimming against the tide. This scorecard takes ten minutes and will save you from at least half of India’s value traps. Titan Biotech‘s regulatory-moated, export-diversified, fermentation-ingredient business scores highly on this scorecard — not because Titan Biotech is magical, but because the industry is structurally favourable, which is the entire point of Porter.

The Live Market Context — 16 April 2026

Today’s -0.16% SENSEX close and the DII outflow of ₹3,427.75 Cr are the kind of headlines that distract investors into tactical decisions. The Porter framework gives you the discipline to ignore them. When you own businesses in Porter-protected industries, a single day’s 100-point nick on the index is meaningless — the five forces that make those businesses durable are still exactly as they were yesterday. By contrast, when you own airlines or commodity steel, every day’s noise becomes existential because the industry provides no shock absorber.

This is also why the SEBI study showing 9 out of 10 individual F&O traders lose money is not just a statistic — it is an industry-structure verdict. The derivatives trading “industry” for retail participants has maximum rivalry (a zero-sum game against algorithmic professionals), zero entry barriers (₹10,000 opens an account), maximum buyer power (brokers compete on price), and perfect substitutes (equity investing). All five arrows point outward at the retail F&O trader. The structural house edge is why the industry is a wealth destroyer.

How to Use the Framework This Weekend

Take your top five holdings. For each, answer the five questions honestly: How many competitors are there? How hard is it for a new one to start? Are your suppliers dominant or diffuse? Do your customers have leverage? Is something cheaper coming? If you cannot score four of the five forces favourably, you probably own a stock that is fighting industry gravity — and industry gravity always wins in the long run.

The goal is not to find a company that has all five forces perfect (almost none do); it is to find companies where the structural score is high enough that even mediocre management cannot destroy it. That is the true definition of a quality compounder. Michael Porter gave us the language, Buffett applied it to investing, and Indian small-cap history keeps proving it right — from Asian Paints and Page Industries to specialty-biotech compounders like Titan Biotech.

Choose your industry before you choose your stock. The industry’s Porter score is your permanent tailwind or headwind. Everything else is noise.

Key Takeaways:

- Porter’s Five Forces (rivalry, new entrants, supplier power, buyer power, substitutes) determines whether an industry creates or destroys capital.

- Moats (switching costs, network effects, pricing power) are consequences of favourable Porter structure — not alternatives to it.

- Score each of the five forces 1-5; a total above 20 means the industry works for incumbents.

- Great Indian compounders — Asian Paints, HDFC Bank, specialty-biotech names like Titan Biotech — win on structure first, execution second.

- Retail F&O trading scores catastrophically on Porter, which is why 90% of participants lose money. Long-term quality investing is the Porter-favourable alternative.

Course Playlist: Free Value Investing Course for Indian Investors on YouTube

📢 Join Our Telegram Channel

Get daily value investing lessons, stock analysis & Titan Biotech updates — delivered straight to your phone!

✈️ Join @longtermequityy on Telegram

🔔 Free • No spam • Value investing insights daily

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.