Value Investing — Educational Series

Every family has one. At a wedding dinner, a cousin leans across the table. He bought a share (a small piece of ownership in a company) that you have never heard of, and it has doubled in six months. Out comes the phone. Screenshots travel around the table. Uncles gather. And somewhere between the dal and the dessert, your own quiet plan — a SIP (a Systematic Investment Plan, where a fixed sum goes into the market every month), a fixed deposit, a few good companies you actually understand — begins to feel like failure.

Notice something strange. Nothing about your money changed at that dinner. Your companies earned the same profits at nine pm as they did at eight pm. Only the comparison changed. Warren Buffett, the most successful investor of our age, has a simple name for the force that attacked you between two courses of a wedding meal. He calls it the outer scorecard. And he credits much of his life to living by its opposite — the inner scorecard. Today’s lesson is that one idea, in plain words: whose report card are you filling when you invest?

The question Buffett asks about every person

In her 2008 book The Snowball, Buffett’s biographer Alice Schroeder records a question he likes to put to people. Would you rather be the world’s greatest lover, but have everyone believe you are the world’s worst? Or would you rather be the world’s worst lover, but have everyone believe you are the greatest?

It sounds like a joke. It is closer to a mirror. Your honest answer reveals which scorecard (which report card) you actually live by. Buffett says it plainly in the same book: “The big question about how people behave is whether they’ve got an Inner Scorecard or an Outer Scorecard. It helps if you can be satisfied with an Inner Scorecard.”

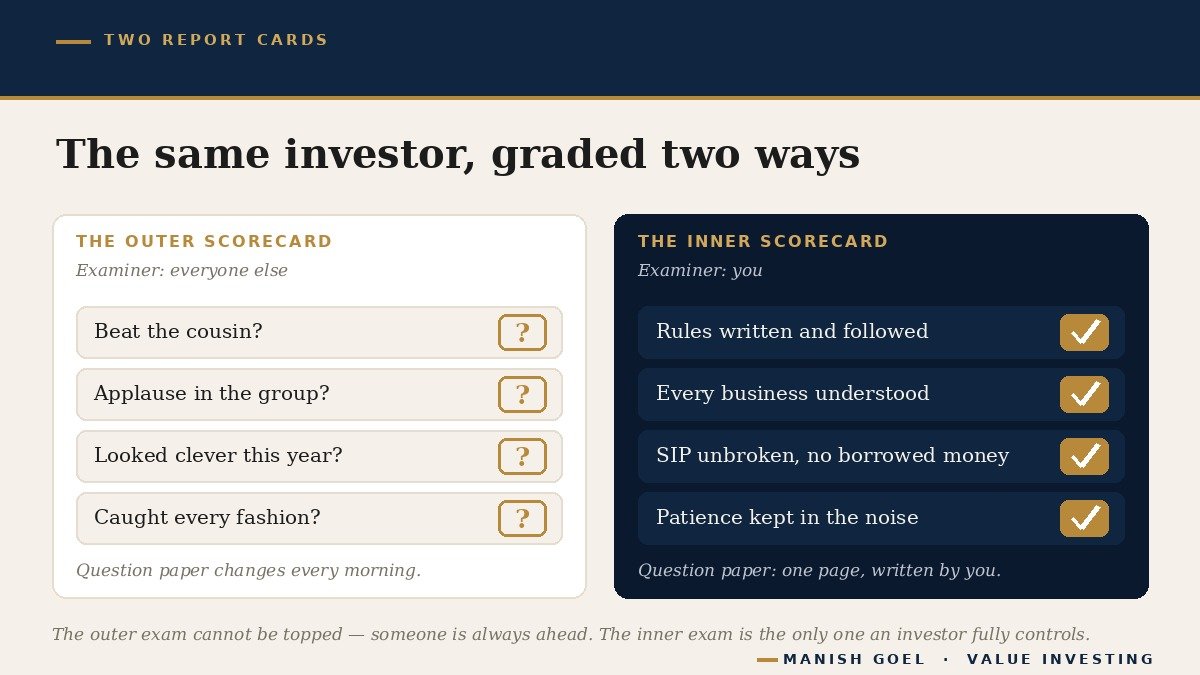

The outer scorecard measures your life by what other people think of it. Marks on a board result, likes on a post, applause at a party, the neighbour’s opinion of your car. The inner scorecard measures your life by standards you wrote for yourself. Did I do the work properly? Did I follow the rules I set on a calm day? Would I be at peace with this decision even if nobody ever praised it?

Buffett learned this at home. His father Howard, a stockbroker who was later elected to the American parliament, simply refused to shape himself to the crowd’s opinion. “Now, my dad,” Buffett told Schroeder, “he was a hundred per cent Inner Scorecard guy.” The son watched, and copied, and built one of the largest fortunes in history sitting far away from the noise of Wall Street, in the small city of Omaha.

Now bring the idea to investing. An outer-scorecard investor asks: how do my returns look this year next to my cousin’s, my colleague’s, my WhatsApp group’s? An inner-scorecard investor asks a different set of questions. Did I put my money only into businesses I understand? Did I avoid companies drowning in debt (borrowed money)? Did I invest at a pace my family budget can sustain, without borrowing, without panic? The first investor is writing an exam whose question paper changes every morning. The second is filling a report card that he himself printed.

Why the neighbour’s profit disturbs your peace

Charlie Munger, Buffett’s business partner for over half a century, spent his life studying the mistakes of clever people. He kept returning to one quiet culprit: envy. “Envy is a really stupid sin,” he said, “because it’s the only one you could never possibly have any fun at. There’s a lot of pain and no fun.” And he offered the sentence every investor should paste on the wardrobe: “Someone will always be getting richer faster than you. This is not a tragedy.”

Think about why that sentence must be true. The market has crores of participants. Every single year, somebody somewhere doubles their money — a lottery buyer also wins somewhere every week. If your scorecard is “beat everyone I hear about,” you have signed up for an exam in which coming first is impossible. There will always be a topper who is not you. A scorecard on which you can never score is not a scorecard. It is a punishment machine.

Envy does not stop at spoiling your mood. It gives instructions. It tells you to sell the sensible things you understand and buy the exciting thing that already doubled — which usually means entering at the peak of the excitement, after the easy gains have been collected by earlier arrivals. It pulls you out of your circle of competence (the small set of businesses you truly understand) and into stories you cannot judge. The kirana shop owner who quietly knows his own street suddenly wants to trade in chemicals he has never seen, because the man two lanes away did.

And switching games has a hidden cost: it breaks compounding (the process where money earns returns on its past returns, the way a snowball grows as it rolls). A fixed deposit broken every six months to chase a slightly better rate keeps paying penalties. A plant shifted to a new pot every month never grows deep roots. Wealth needs time sitting still in good soil, and the outer scorecard never lets you sit still.

There is one more problem with grading yourself by the crowd: the crowd shows you edited marksheets. People post their winners, not their losers. The cousin showed the share that doubled. He did not show the three earlier tips that went nowhere, or the loan he took to buy the fourth. Comparing your full, honest report card with everyone else’s highlights reel is a game designed to make you feel poor — and then to make you actually poorer, once you start acting on the feeling.

If this feels familiar, it is because India has just lived through the largest bragging season in its history. In the years after 2020, crores of new demat accounts (the accounts in which your shares are held) were opened, and for a while a rising market made every neighbour, colleague and college group sound like a genius. When prices rise together, the outer scorecard becomes deafening; every gathering has a topper waving a screenshot. That is precisely when the quiet page of rules earns its keep — because a scorecard you borrowed from the loudest voice in the room will be torn up by the same voice in the next fall.

The winter of 1999: the year the applause stopped

If the inner scorecard sounds easy, look at what it cost the man who preached it. In 1999, America was in the grip of the dot-com boom. Shares of internet companies (many with no profits at all) were doubling in weeks. Buffett refused to buy them. His reason was almost embarrassingly simple: he could not honestly say he understood which of these young companies would still be earning strong profits ten years later, so he stayed with businesses he did understand — paint, carpets, insurance, soft drinks.

The outer scorecard punished him brutally. That year, the American market rose strongly while Berkshire Hathaway, Buffett’s own company, fell by roughly a quarter. Television anchors called him a man of the old economy. On 27 December 1999, Barron’s, one of America’s best-known financial newspapers, put the question on its cover: “What’s Wrong, Warren?” The article suggested the sixty-nine-year-old might have lost his touch. Measured by applause, 1999 was the worst report card of Buffett’s life.

Measured by his own scorecard, he had passed every single day of it. He knew what he owned. He had followed rules written long before the party started. Then the party ended. Over the next three years the Nasdaq (the American market where most technology shares trade) lost roughly three-quarters of its value. In those same three years after the mocking cover, Berkshire’s share price rose by about thirty per cent while the broad American market fell by more than a third. Same man, same method, same office in Omaha. Only the direction of the applause changed.

India has its own quiet example. Radhakishan Damani, the investor who built the DMart chain of supermarkets and became one of the country’s wealthiest men, is famous for something unusual: silence. He almost never gives interviews. He avoids television studios, stages and cameras, and is often called the “silent billionaire.” Through the loudest years of Indian markets, when a new expert was born on every channel every evening, one of the most successful investors in the country simply kept working, far from the microphones. Whatever else one learns from his story — and it is told here only as history, not as a comment on any company or share — the habit itself is the lesson: the work mattered to him more than the applause for it.

How to build your own scorecard

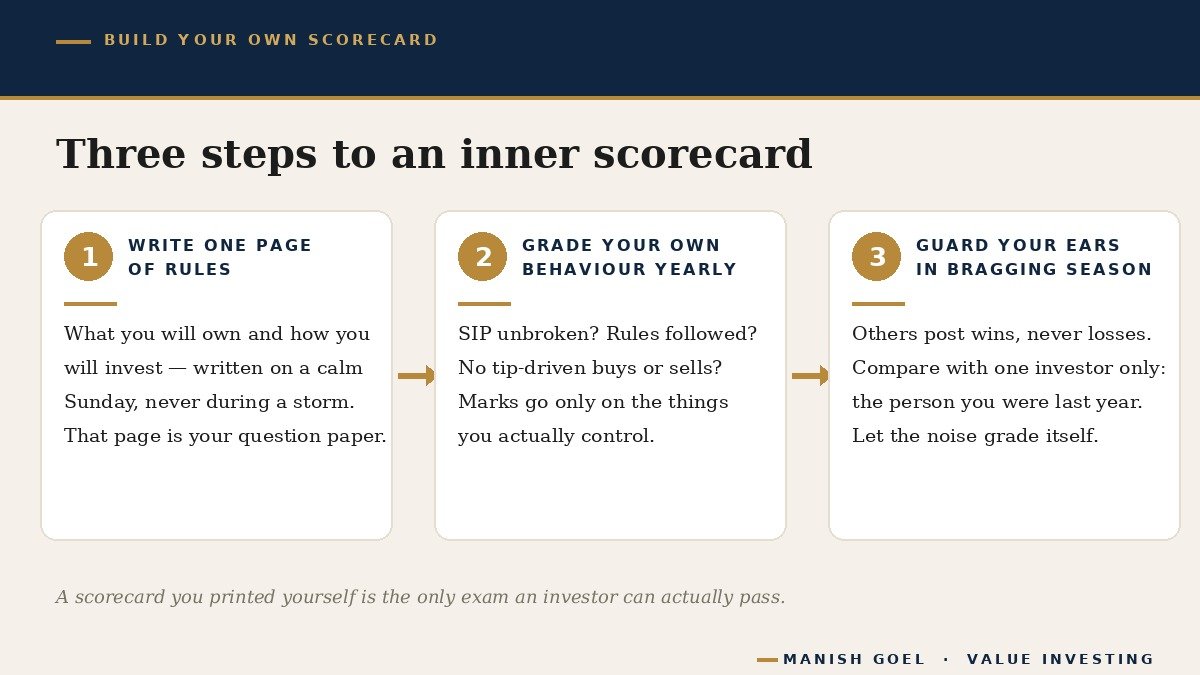

The inner scorecard is not a mood. It is a document. Here are three simple steps an ordinary investor can take this week.

First, write your rules on one page. On a calm Sunday, not during a market storm, write down what you will own and how you will invest. For example: I will own businesses I can explain to my family in two minutes. I will prefer companies with little debt, profits that arrive as real cash, and promoters (the main owners who run a company) with a clean record. I will invest through a monthly SIP, only with money I will not need for at least five to seven years, and never with borrowed money. Your list may differ. What matters is that it exists, on paper, written by you — because that page, and not the wedding dinner, is now your question paper.

Second, grade your behaviour, not your neighbour. Once a year, sit with that page and mark yourself on things you control. Did the SIP run all twelve months without a miss? Did every purchase follow my written rules? Did I buy or sell anything only because of a forward, a tip or a party conversation? Am I saving a little more than last year, and do I understand my companies a little better than last year? Notice that share prices barely appear on this report card. A single year’s price move is weather; your behaviour is the climate. Beginners who score well on behaviour for many years tend to find that the results take care of themselves.

Third, protect your ears in the bragging season. You do not have to leave the family WhatsApp group. You only have to refuse to let it grade you. When markets are euphoric and every gathering produces a new genius, remind yourself of Munger’s line — someone will always be getting richer faster than you, and it is not a tragedy. The only tragedy would be abandoning a sound plan, built for your family’s goals, to copy a stranger’s edited marksheet. If the noise gets loud, compare yourself with the only investor whose full record you truly know: the person you were last year.

One caution, so the idea is not misunderstood. An inner scorecard is not stubbornness, and it is not a licence to ignore facts. If a business you own starts taking on heavy debt, or its promoters begin behaving badly, your own written rules should be the very thing that makes you act. The difference is the reason for acting. The inner-scorecard investor changes course when the facts change; the outer-scorecard investor changes course when the applause changes. Buffett held his ground in 1999 not because he never listens, but because nobody criticising him could point to a fact about his businesses that had worsened — only to a crowd that had moved elsewhere.

Key takeaways

- The outer scorecard grades your investing by other people’s opinions and returns; the inner scorecard grades it by rules you wrote yourself. Buffett credits his life’s results to the inner one.

- In a market of crores of investors somebody will always be ahead of you this year, so “beat everyone” is an exam you can never top — envy is all pain and no fun, as Munger put it.

- Comparison gives bad instructions: it pushes you to buy excitement after it has already doubled, to leave businesses you understand, and to break the sitting-still that compounding requires.

- In 1999 the world’s press asked “What’s Wrong, Warren?” because he refused shares he did not understand; within three years the technology index had lost roughly three-quarters of its value and the applause reversed. Rules outlast opinions.

- Build your own scorecard this week: one page of written rules, a yearly grade on behaviour you control, and ears that stay closed in the bragging season.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.