Value Investing — Educational Series

Imagine your grandfather slipped a ₹100 note into a steel almirah (cupboard) back in 1995 and then forgot all about it. Today you open that almirah and there it is — the same note, crisp and untouched, still ₹100. Nothing has been stolen. The lock was never broken. And yet that ₹100 will buy you only a small fraction of what it bought him thirty years ago. A simple meal, a few litres of milk, a child’s set of school books — things ₹100 once paid for now cost five or six times as much. The note did not shrink. Its power to buy shrank.

Something quietly walked away with most of that note’s value, and it has a name. It is called inflation — the slow, steady rise in the price of almost everything we buy. Inflation is the silent thief of the saver. It never breaks a lock and never makes a sound, and that is exactly what makes it so dangerous: most people never notice it taking from them, a little every year, until decades have slipped past and the damage is done.

This is one of the most important ideas a new investor in India can learn, because it quietly changes the whole question. The question is not only, “How do I keep my money safe?” The deeper question is, “How do I keep my money’s power to buy safe?” Cash locked in an almirah is perfectly safe — and a little poorer every single day. Let us understand why this happens, and what the great investors did about it.

What inflation really is

Inflation simply means that, taken together, prices climb over time. The plate of pav bhaji that cost ₹20 a few years ago is ₹40 today. The auto fare, the cooking-gas cylinder, the school fee, the morning cup of chai — they all creep upward. When prices rise, each rupee in your pocket buys a little less than it did before. Economists call this loss your falling purchasing power (purchasing power simply means how much your money can actually buy in real goods, not the number printed on the note). Prices rise for ordinary reasons — wages go up, raw materials cost more, and over time there is more money chasing the same goods — but the effect on you is always the same: the same rupee does less work each year.

How quickly does this bite? In India, prices have climbed by roughly 5 to 6 out of every 100 rupees each year, on average, over the long run — and everyday food prices often rise even faster, which is why the monthly vegetable and grocery bill seems to grow no matter how carefully you shop. The Reserve Bank of India (the RBI, our central bank, which is given the job of keeping prices steady) aims for inflation of about 4%, and tries to hold it between 2% and 6%. In May 2026, official retail inflation was about 3.9%, sitting comfortably inside that band. A few percent a year sounds small and harmless. Who would even notice? That is precisely the trap.

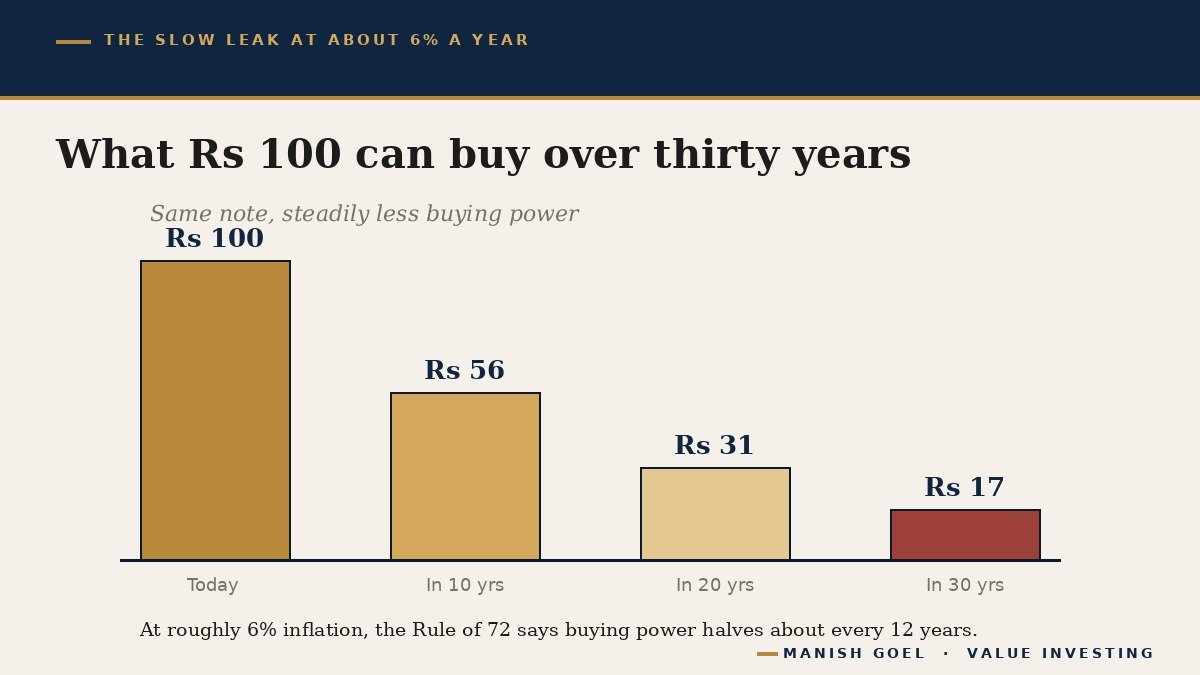

There is a simple piece of mental arithmetic that reveals the danger, called the Rule of 72 (a quick trick: divide 72 by the yearly rate, and you get the rough number of years for something to double — or, here, to halve). At 6% inflation, 72 divided by 6 is 12 — so prices double, and your money’s buying power halves, in about twelve years. Even at the RBI’s gentle 4% target, it takes only about eighteen years. Either way, within a single working life the rupee in your hand quietly loses half its strength — and then half again. That ₹100 note from thirty years ago now buys only about ₹15 to ₹20 worth of goods. The note never changed; the world around it simply grew more expensive.

Why your “safe” savings may not be as safe as they feel

Most Indian families keep their savings in places that feel completely safe: a savings bank account, a fixed deposit (an FD — money locked with a bank for a fixed period in return for a fixed rate of interest), gold in the locker, or simply cash at home. Safety genuinely matters, and an emergency cushion should always sit in exactly such places. But for money you are setting aside for many years — a child’s education, your own retirement — the word “safe” can be quietly misleading.

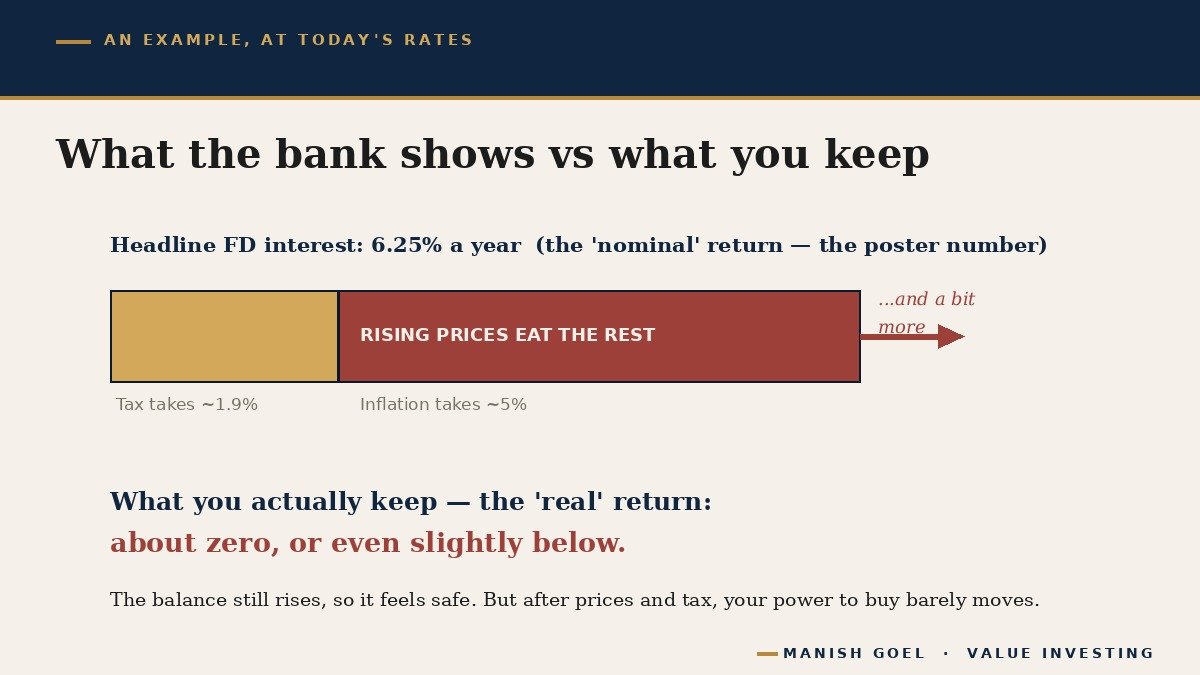

Here is the idea that changes everything. When a bank offers you, say, 6.25% on a one-year FD, that 6.25% is the nominal return — the headline figure, the number on the poster. But the number that actually decides whether you grew richer is the real return — what is left after you subtract inflation. If your FD pays about 6% while prices rise about 5%, your money’s true growth in buying power is only about 1%. And the story is not over, because the interest on an FD is taxed. For someone in a higher tax slab, a 6% FD can shrink to roughly 4% after tax. Subtract 5% inflation from that, and the real return slips below zero. Your bank balance went up; your power to buy went quietly down.

Put a number on it. Park ₹1 lakh in that FD for a year and the statement proudly shows about ₹1,06,000. It feels like a gain. But if the same basket of groceries, fees and fuel that cost ₹1 lakh last year now costs ₹1,05,000, your extra ₹6,000 has bought you almost nothing — and after tax on the interest, you may actually be able to buy less than before. Cash sitting at home is worse still: it earns nothing at all, so inflation eats it at full speed. Even gold, which Indians love and trust, earns no income while it lies in the locker, and its price can sit still for years at a time. This is the uncomfortable truth the silent thief hides: money that merely “feels safe” is often losing the slow race against rising prices. It never feels like a loss, because the number never drops — but a number that grows slower than prices is a loss wearing the costume of safety.

The real cure: owning a slice of good businesses

If idle money loses to inflation, what beats it? Over long stretches of history, the answer has been owning a small piece of a real, growing business. When you buy a share (also called equity — a share is literally a tiny ownership slice of a company), you are no longer holding still, silent money. You own a part of a living business that sells things, earns profits, and can grow — much like owning a corner of a busy kirana shop and taking your portion of what it earns.

Why should this beat inflation? Because the very same rising prices that hurt the saver can actually help the right business. When the cost of everything goes up, a good business simply charges its customers a little more — and its sales and profits rise right along with prices. The clearest proof is India’s own stock-market index, the Sensex (a basket that tracks the share prices of 30 large, well-known Indian companies, used as a thermometer for the whole market). It began at a value of just 100 back in 1979. Over the four decades since, it has compounded at roughly 15% a year — multiplying many hundreds of times over — leaving the 5 to 6% taken by inflation far, far behind. (Compounding means earning returns on your past returns too — like interest on interest, or a snowball that grows heavier as it rolls downhill.)

But — and this is the very heart of the lesson — not every business beats inflation. Warren Buffett, widely regarded as the greatest investor of all time, warned about this in two famous places: a 1977 article titled “How Inflation Swindles the Equity Investor,” and his 1981 letter to shareholders, in which he called inflation a “gigantic corporate tapeworm.” A tapeworm is a parasite that eats its host’s food no matter how much the host manages to eat. In just the same way, Buffett explained, inflation forces a weak business to keep pouring more and more money into the same machines, the same stock on the shelf, and the same unpaid customer bills, merely to stand in the same place. Think of an airline or a plain steel maker that must keep buying ever-costlier fuel and metal just to sell the same amount next year — rising prices swallow its cash and leave nothing for the owner. A poor business is eaten alive by inflation. A great one is not.

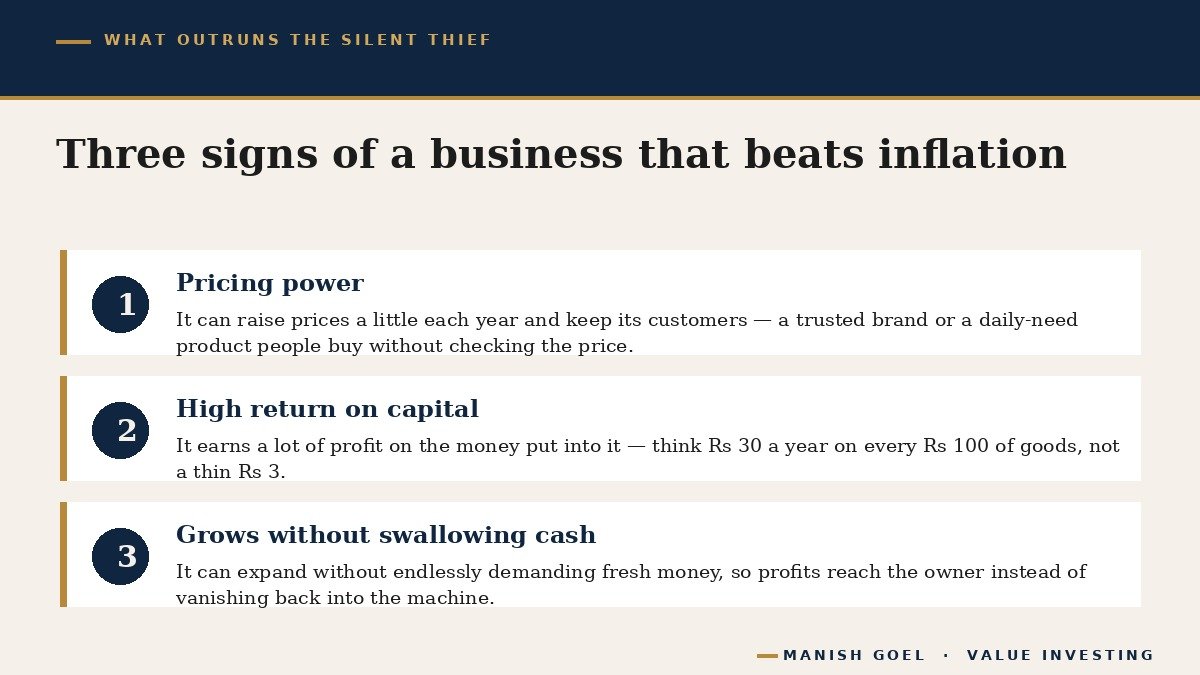

So inflation is not an argument against owning businesses — it is the strongest possible argument for owning quality businesses. And what does a quality business, the kind that beats inflation, actually look like? Three plain signs, shown below.

First, pricing power — the ability to raise prices without losing customers (pricing power is the quiet strength of a trusted brand or a daily-need product; people grumble for a moment, then buy it anyway). Second, a high return on capital — meaning the business earns a lot of profit on the money put into it; picture a shop that earns ₹30 a year on every ₹100 of goods on its shelves, against a struggling one that earns only ₹3. Third, low extra capital needed to grow — the business can expand without endlessly demanding fresh cash, so its profits actually reach the owner instead of disappearing back into the machinery. A business that has all three can pass rising costs on to its customers and still keep plenty for itself. That is what outruns the silent thief.

What the masters and the market show us

Take the simplest everyday example. Think of a soap, a biscuit, or a tube of toothpaste you have trusted since childhood. Each year its price ticks up by a rupee or two, and yet you drop it into your basket without a second thought. That quiet, almost invisible price rise — multiplied across millions of loyal buyers — is precisely how a strong business turns inflation from an enemy into a tailwind. The customer hardly notices; the owner of the business collects, year after year. That is pricing power doing its silent work.

India’s own market history makes the point vividly. Rakesh Jhunjhunwala, so successful that he was often called India’s Warren Buffett, famously began with only a few thousand rupees in the mid-1980s and, by patiently owning shares of growing Indian businesses for decades, built one of the country’s great fortunes. Across those very same decades the rupee steadily lost value to inflation — the price of that cup of tea multiplied many times over. The person who left money idle watched it weaken. The person who owned good businesses watched wealth outgrow rising prices. Same country, same inflation, opposite endings.

None of this is a tip to buy or sell any particular share, and it is certainly not about guessing whether a stock is cheap or dear today. It is about a direction of travel: over long periods, idle money quietly drifts down in real worth, while a slice of good businesses tends to drift up faster than prices. Buffett liked to point out that over his own fifty years the US dollar lost the great majority of its purchasing power, even as ownership of fine businesses multiplied wealth many times over. The Sensex’s long climb tells the same story his tapeworm warned about — quality survives inflation, and weakness is consumed by it.

How you can use this — three simple steps

First, separate your “sleep-at-night” money from your “long-term” money. Keep an emergency cushion — a few months of expenses — in a savings account or short FD, where being available matters more than growing. That money is meant to be reached for in a hurry, not to win a race against inflation. It is the rest — the money you will not need to touch for many years — that must be put to work.

Second, for that long-term money, own a slice of good businesses rather than letting it lie idle. A beginner does not have to pick individual shares to do this; many simply use a low-cost index fund (a fund that quietly owns a whole basket of companies, such as the Sensex or Nifty, for a very small fee) and add a fixed sum to it every month. The aim is steady ownership of real businesses over many years — not clever guessing about next week’s price.

Third, when you do study individual companies, hunt patiently for the three signs of quality above: pricing power, a high return on the capital they use, and the ability to grow without swallowing endless cash. Then wait. Inflation works slowly against you; compounding inside a good business works slowly — and then powerfully — for you. Time is the loyal friend of the patient owner of quality, and the quiet enemy of the idle saver.

Key takeaways

- Inflation is the silent, steady rise in prices; it shrinks what your money can buy even when the number in your account never falls.

- At about 6% inflation your money’s buying power halves roughly every twelve years (the Rule of 72) — a ₹100 note from thirty years ago buys only about ₹15 to ₹20 of goods today.

- “Safe” savings can quietly lose: after subtracting inflation and tax, the real return on a fixed deposit can fall close to zero, and cash at home loses the fastest of all.

- Owning a slice of good businesses has, over long periods, grown faster than prices — India’s Sensex compounded around 15% a year since 1979, far ahead of inflation.

- But inflation spares only quality. Look for pricing power, high returns on capital, and growth that does not constantly demand fresh cash — then let patience and compounding do the rest.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.