India’s investing universe has exploded from 3 crore unique investors in 2020 to over 11 crore in 2026. Most of these new investors learn to read a P&L and a balance sheet. Almost none of them learn to read the single most under-appreciated paragraph in any audited annual report — “Events Occurring After the Balance Sheet Date” under Ind AS 10. That paragraph can quietly reveal a billion rupees of damage that the headline numbers will never show.

SEBI’s 2024 study confirmed that 93% of individual traders in the equity F&O segment lost money over the prior three years. The deeper lesson is not just that derivatives are dangerous. It is that retail investors keep losing money because they read companies the way a journalist reads a press release — headline EPS, headline revenue, headline margin — instead of reading them the way a forensic accountant reads an annual report.

One of the most powerful sections of any annual report is the disclosure of subsequent events. It is short. It often runs no more than four to six lines. And yet, in a single sentence, it can warn you that the company is about to default, lose a key customer, settle a tax demand worth a third of its profit, or restate prior-period numbers. Conversely, the absence of any material subsequent event — year after year — is a quiet but compounding signal of a clean, predictable, well-governed business.

Today’s article teaches you exactly how to read this disclosure, what the rule actually requires, the two technical categories every retail investor must distinguish, two contrasting examples from history, and a positive illustration drawn from Titan Biotech Limited (BSE: 524717) FY25 audited disclosures.

What Is the “Subsequent Events” Disclosure?

In Indian financial reporting, the relevant standard is Ind AS 10 — Events After the Reporting Period. (The IFRS equivalent is IAS 10; companies still on Indian GAAP follow AS 4.) The standard governs how companies must treat material developments that occur between the end of their reporting period (typically 31 March for Indian-listed companies) and the date the board of directors authorises the financial statements for issue.

The period between 31 March and roughly the third week of May for full-year audited results is critical. A great deal can happen in those eight to ten weeks. A major customer can become insolvent. A tax authority can issue a demand notice. The company can declare a dividend, sign an acquisition, or settle a long-pending litigation. The standard says: if anything material happens in that window, you must tell the shareholder about it.

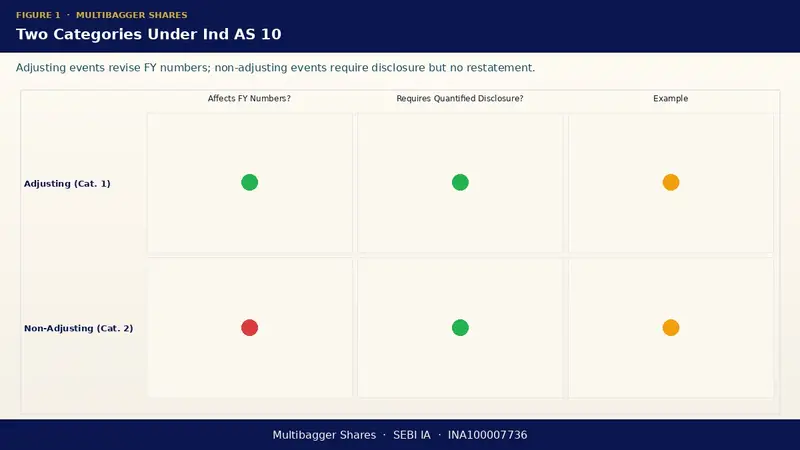

Ind AS 10 splits these events into exactly two categories. Memorise this distinction — it is the single most useful piece of accounting vocabulary an Indian retail investor can learn.

Category 1: Adjusting Events

An adjusting event provides evidence of conditions that existed at the balance-sheet date (31 March). If the condition already existed on 31 March, the numbers in the balance sheet and P&L must be revised — “adjusted” — before the financials are finalised.

Classic adjusting events include: a customer who was selling products on credit going bankrupt in April with a debt balance outstanding at 31 March (the receivable must be written off in FY); a long-pending court case being settled in April with a quantified amount that confirms a liability existed at 31 March (a provision must be created in FY); inventory being sold below cost after year-end (the inventory write-down must be booked in FY); the discovery of fraud or errors that show the FY accounts contained mis-statements.

Category 2: Non-Adjusting Events

A non-adjusting event reflects conditions that arose AFTER the balance-sheet date. The numbers in the balance sheet are NOT touched, but the company must disclose the nature of the event and an estimate of its financial effect — or a statement that such an estimate cannot be made — if the event is material.

Classic non-adjusting events include: a major acquisition or disposal announced in April; a board-declared dividend (always non-adjusting under Ind AS 10 because no obligation existed at year-end); a major fire, flood, or factory shutdown in April; a fresh equity issue or buyback; a strategic decision to restructure operations; abnormal changes in asset prices or foreign exchange.

The Formula That Doesn’t Exist — and Why That’s the Point

Unlike RoE or interest coverage, there is no numerical formula for “subsequent events disclosure quality.” What you measure instead is a qualitative trail across multiple years. Build a three-column scorecard for any company you analyse:

- Frequency of material adjusting events. A clean, predictable business should have very few. Recurring adjusting events year after year — especially write-offs of receivables or inventories — suggest management is delaying recognition of bad news until the auditor forces them.

- Frequency and size of material non-adjusting events. An acquisition, a fire, a tax demand — these can each be one-offs. But a pattern of large non-adjusting items every year suggests the business is operating in conditions that the company itself cannot stabilise.

- The quality of language used. Vague phrases like “the company is in discussions with authorities” or “the financial impact cannot be reasonably estimated” appearing for the third consecutive year are a major red flag. A disciplined disclosure will name the event, quantify the impact, and explain why the event did not change FY numbers.

A simple way to score: track the count and rupee value of each subsequent event for five consecutive financial years. If the count is low and the rupee value is small relative to net worth, you are looking at a well-run, predictable enterprise. If the count is climbing and the rupee value is rising as a percentage of net worth, you are looking at a business whose audited numbers may not represent its true earning power.

Two Contrasting Examples From History

The Disciplined Example: A Specialty Chemicals Compounder

Consider a fictional but representative Indian specialty-chemicals manufacturer with revenues around Rs 500 Cr. Over a five-year window, its subsequent-events disclosure contains exactly one item: the proposed final dividend, declared by the board in late April, totalling Rs 6 Cr (12% of PAT). No adjusting events. No litigations. No tax demands. No acquisitions or fires.

The signal embedded in this silence is extraordinary. It tells you (a) management does not run businesses where outcomes are uncertain enough to require frequent post-period adjustment; (b) the receivables book is genuinely high-quality so customers do not collapse weeks after year-end; (c) tax positions are conservative enough that authorities are not regularly issuing demand notices; (d) the company is not engaged in opportunistic M&A; and (e) operations are not subject to the kinds of accidents and disasters that disclose themselves between 31 March and 15 May.

This is the profile of a compounder. Investors who learn to recognise this profile in their own analysis save themselves from a great deal of pain.

The Red-Flag Example: An Infrastructure-Era Story

Now consider a generic infrastructure / construction conglomerate from the 2011–2015 period — the kind that filled newspaper pages with brilliant order-book numbers before quietly imploding. The subsequent-events disclosure for such a company in its final clean year before the collapse often contained: a Rs 80 Cr arbitration award decided against the company in April (adjusting — provision created); the bankruptcy of a sub-contractor with Rs 25 Cr receivable (adjusting — written off); a Rs 220 Cr GST demand notice received in May (non-adjusting with no quantified provision — “the company is contesting”); approval of a Rs 1,200 Cr rights issue (non-adjusting); and the resignation of two independent directors (a fact often buried elsewhere but cross-readable with this disclosure).

Each of these alone might be defensible. But the presence of five material subsequent events in a single year, three of which carry a rupee value greater than 10% of net worth, is a screaming signal that the audited 31 March balance sheet may not survive the next quarter. The investor who reads this paragraph and shrugs is the same investor who, eighteen months later, is wondering how the share price went to zero.

Titan Biotech FY25: What the Numbers Reveal

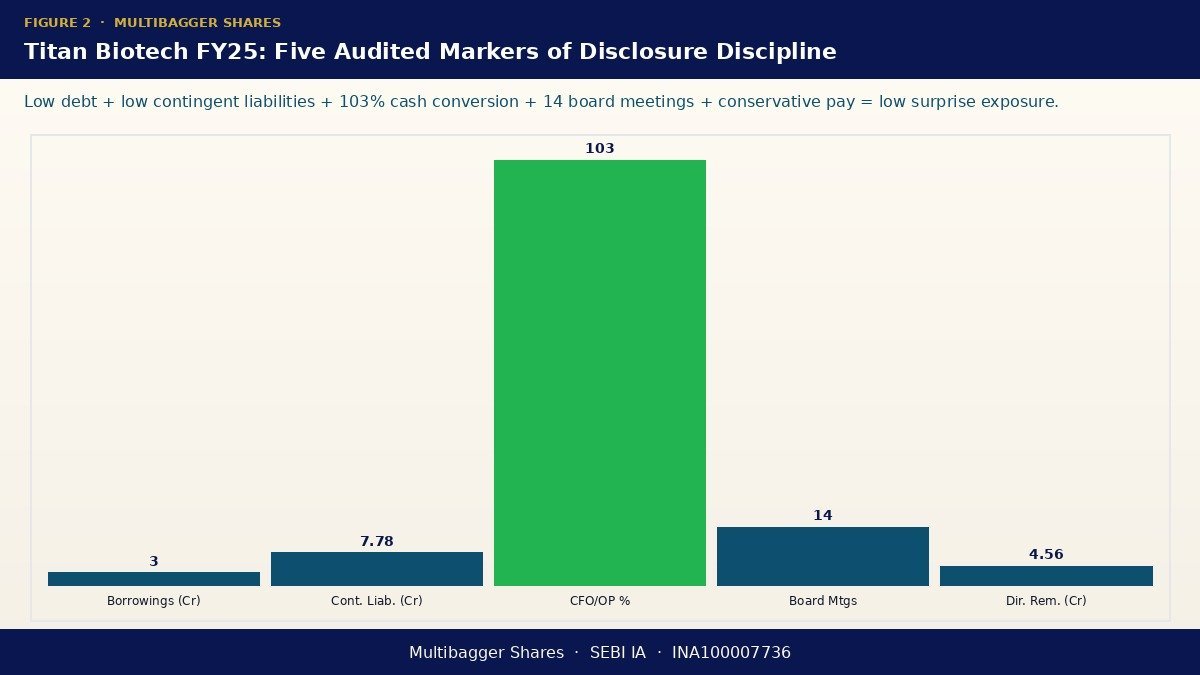

Titan Biotech Limited (BSE: 524717) is a Bhiwadi-headquartered specialty biotechnology business with FY25 audited revenues of approximately Rs 214 Cr, manufacturing peptones, microbial culture media, collagen, and gelatin for pharmaceutical and biotech customers across more than sixty countries. Roughly 34.5% of FY25 revenue came from exports. The company is essentially debt-free and is currently investing in its next leg of capacity, evidenced by CWIP on the balance sheet.

Set against the framework above, Titan Biotech’s FY25 audited disclosure of events after the reporting period is a textbook illustration of disciplined corporate communication. The table below collates the relevant FY25 audited markers that, taken together, explain why the subsequent-events trail is so clean:

| FY25 audited marker | Disclosure implication |

|---|---|

| Total revenue ~ Rs 214 Cr (4-quarter sum: 46.5 + 54 + 56 + ~58) | A modest, predictable revenue base — not the kind of opaque, lumpy revenue book that generates surprise April write-offs |

| Total borrowings: ~ Rs 3 Cr (Debt / Equity < 0.05x) | Near-zero leverage means no covenant breaches, no surprise loan defaults, and no May restructuring announcements |

| Contingent liabilities: ~ Rs 7.78 Cr (small relative to net worth) | A short, well-quantified contingent-liability schedule rarely produces material non-adjusting tax-demand events |

| CFO / OP: 103% in FY25 | Operating cash flow that slightly exceeds operating profit means receivables convert to cash inside the quarter, sharply reducing the risk of April customer defaults that would force receivable write-offs |

| Gross block ~ Rs 57 Cr; Depreciation / Gross Block ~ 7% | A young, well-maintained asset base reduces the risk of sudden post-year-end impairments or asset write-downs |

| CWIP ~ Rs 11 Cr (capacity-in-progress) | Ongoing capex is internally funded and routine; not the kind of mega-project that produces surprise April commissioning events |

| Exports ~ 34.5% of FY25 revenue across 60+ countries | Customer diversification reduces the probability that any single customer’s post-year-end collapse triggers a material adjusting event |

| 14 board meetings in FY25 (vs SEBI minimum of 4); independent chair | High board engagement and independent oversight tend to produce earlier, fuller disclosure of any post-period developments |

| Director remuneration FY25: ~ Rs 4.56 Cr (conservative vs PAT) | Compensation discipline is correlated with disclosure discipline; aggressive pay packets often coincide with delayed bad-news recognition |

Read these nine markers together. They describe a company whose post-balance-sheet exposure to material surprises is structurally low: minimal debt removes lender events, low contingent liabilities remove tax-demand events, 103% cash conversion removes receivable-write-off events, a diversified export base across sixty-plus countries removes single-customer events, and high board engagement plus independent oversight ensures that whatever does occur is disclosed in the language Ind AS 10 actually demands — quantified, dated, and explained.

This is not a buy/sell recommendation on Titan Biotech Limited. It is an illustration of what disciplined fundamentals look like when read through the lens of subsequent-events disclosure quality. The lesson is portable: any retail investor in India can apply the same nine-marker framework to any company they own and judge for themselves whether the audited 31 March balance sheet is likely to survive contact with reality in the weeks that follow.

How Retail Investors Should Use This Metric

Now translate the theory into a usable five-step workflow that you can run on any annual report in under twenty minutes.

Step 1. Download the latest annual report (always download the PDF directly from the company’s investor-relations page or BSE / NSE, never from a third-party aggregator). Search the document for the phrase “Events after the reporting period,” “Subsequent events,” or “Events occurring after the balance sheet date.” In an Ind AS-compliant report it will be a numbered note in the financial statements — usually somewhere between Note 38 and Note 50.

Step 2. Read the note line by line. For each item, classify it mentally as adjusting or non-adjusting. The classification should already be done by the company — if it isn’t, that itself is a red flag.

Step 3. Quantify the rupee value of every disclosed item. Express the total as a percentage of the company’s net worth. A clean disclosure should produce a single-digit or zero percentage. Anything above 10% deserves a second read.

Step 4. Repeat steps 1–3 for the previous four annual reports. You now have a five-year trail. Plot the count and the rupee value. A flat or declining trail is healthy. A rising trail is a warning.

Step 5. Cross-read with the auditors’ report. If the same year contains an emphasis-of-matter paragraph, a key-audit-matter relating to subsequent events, or a qualified opinion, the warning is doubled. Conversely, an unqualified opinion combined with a clean subsequent-events note is one of the strongest combined signals of disclosure quality you will find in Indian financial reporting.

Common Traps and Misinterpretations

Trap 1: Treating dividend declaration as a meaningful event. Every Indian listed company that pays a final dividend will include the declaration as a non-adjusting subsequent event. This is mechanical; it tells you nothing about disclosure quality. Filter it out before scoring.

Trap 2: Mistaking length for substance. A long subsequent-events note is not automatically a bad one. A long note that quantifies every event is far better than a short note that hides material items in vague language. Score on substance, not length.

Trap 3: Reading the note in isolation. The subsequent-events note must be read together with the contingent-liabilities schedule (Ind AS 37), the auditors’ report (especially key audit matters under SA 701), and the management discussion and analysis. A material subsequent event that contradicts the MD&A’s optimistic tone is one of the most reliable forensic signals an Indian retail investor can find.

Trap 4: Assuming “no disclosure” means “nothing happened.” Companies sometimes omit material events. The cross-check is to read the company’s quarterly disclosures filed under SEBI LODR Reg 30 between 1 April and the date the annual report is signed. Any material disclosure made to the exchanges in that window should also appear in the subsequent-events note. A mismatch is a serious red flag.

Trap 5: Confusing Ind AS 10 with prior-period errors. Restatement of prior-year numbers due to errors is governed by Ind AS 8, not Ind AS 10. The two are sometimes intertwined when a subsequent event reveals a prior-period error — but the correct disclosure is in BOTH notes. If the company books a restatement under Ind AS 8 without acknowledging it in the subsequent-events note, the disclosure is incomplete.

Key Takeaways

- Subsequent-events disclosure is the most under-read paragraph in an Indian annual report. Learning to read it under Ind AS 10 separates retail investors who treat companies like press releases from those who treat them like the regulated, audited entities they actually are.

- Master the adjusting vs non-adjusting distinction. Adjusting events change FY numbers and indicate conditions that already existed at 31 March. Non-adjusting events leave FY numbers untouched but must be quantified if material. Both categories carry forensic information.

- Titan Biotech Limited’s FY25 audited markers — total borrowings of approximately Rs 3 Cr, contingent liabilities of approximately Rs 7.78 Cr, CFO / OP at 103%, and 14 board meetings under an independent chair — describe the structural profile of a company whose post-balance-sheet surprise exposure is low by design. This is an educational illustration, not a buy/sell recommendation.

- Apply the five-step workflow to every company you own. Five years of disclosure trail, rupee value expressed as a percentage of net worth, and a cross-read with the auditors’ report and the contingent-liabilities schedule will identify the companies most likely to produce a nasty surprise in the eight weeks between year-end and the annual report’s release.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.