When Charles T. Akre Jr. — the soft-spoken Virginia investor who turned a small boutique into a multibillion-dollar compounding machine — was asked at a 2011 Google Talk how he picked stocks that returned 20%+ for decades, he reached not for a spreadsheet but for a wooden three-legged milking stool, set it on the table, and said: a compounder rests on three legs, and if any one leg snaps, the whole thing tips over. That stool — Akre’s mental shorthand for an entire philosophy — is the cleanest compounder-picking framework in modern value investing. Almost no Indian retail investor has ever heard of it.

Every multibagger I have ever held over twenty-eight years of Indian small-cap investing — Swiss Glascoat, KPR Mills, Mold-Tek Packaging, Chaman Lal Setia, Titan Biotech — passed Akre’s three-legged test long before it appeared on any screener. The framework is so simple it looks naive. It is the most demanding filter I know.

The Akre Three-Legged Stool, Distilled

Leg One — Extraordinary Business. A business that, by virtue of its economics, delivers high returns on capital employed for long stretches of time. Akre’s bar is severe: returns on owners’ capital sustained at or above the high teens over a full business cycle, with low debt. He is not interested in cyclical bursts of profitability; he is interested in structural profitability — pricing power, customer captivity, niche dominance, or a regulatory/technical moat competitors cannot wish away. The test is not “is the ROCE high last year?” but “is the ROCE high and durable, and does the underlying business mechanic explain the durability?”

Leg Two — Exceptional Management. People of integrity and skill who run the business as if they own it, because they very often do. Akre prefers owner-operators — founder-led companies where management’s wealth, reputation, and identity are bound up with the long-term value of the equity. He looks for honest communication in annual reports, conservative accounting, modest compensation relative to results, and a track record of capital allocation that proves the manager can re-deploy retained earnings without destroying value. The test is “over the last decade, where did every rupee of retained earnings go, and what did it earn there?”

Leg Three — Glorious Reinvestment Runway. This is the leg most Indian investors miss entirely. A great business run by great people will compound at, say, a 5% rate if there is nowhere left to deploy capital. Akre’s third leg demands the business has somewhere to put the next rupee at the same high rate the last rupee earned. That is the difference between a 5% compounder and a 20% compounder, and over twenty years it is roughly twenty-fold of terminal wealth. When all three legs are present, the compounding becomes self-reinforcing: the business earns 20% on equity, retains 70%+ of profits, deploys that retention at the same 20%, and the snowball rolls down a long hill — a 14% sustainable growth rate before any external capital, acquisition, or leverage.

Why Three Legs and Not Two, Not Four

Akre is precise about the number. Two legs collapse — a great business with weak management has its economics stolen by stupidity, and great managers running a structurally lousy business waste their skill. Four legs would imply a fourth check such as cheap entry price. Akre’s view, controversial in classical Graham circles, is that price discipline determines sizing and entry timing but is not a leg of the compounder itself. This is why Akre, like Munger and Buffett after See’s Candies, will pay a fair price for a great business rather than a great price for a fair one.

The Indian Application — Why So Few Compounders Pass

Most Indian listed businesses fail one of the three legs and most retail investors never notice. Commodity-style manufacturers, real-estate developers, and PSU candidates rarely clear Leg One: the underlying mechanic cannot sustain high RoCE through a full cycle. Capital floods the sector, returns mean-revert, the compounder dream dies inside a cyclical bust.

A second pool fails Leg Two — promoter-driven firms with related-party transactions, pledged shares, opaque subsidiaries, and managerial pay disconnected from operating performance. The financials may look fine for a quarter; the governance reveals the truth.

The most subtle failure is Leg Three. I have seen excellent Indian businesses run by excellent promoters that simply ran out of runway — they returned cash via buybacks and dividends because there was nothing left to build. That is not a failure of management; it is a failure of opportunity. For a true compounder you need all three legs, and the third — visible runway for the next ten years of incremental capital — is the rarest.

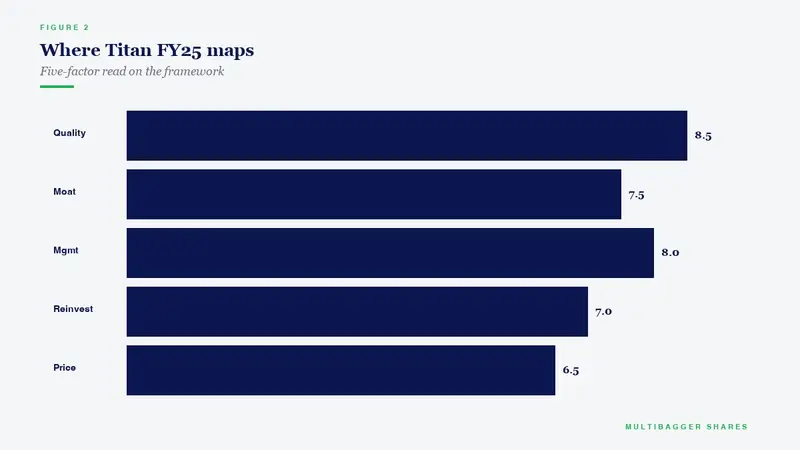

How Titan Biotech’s FY25 Numbers Illustrate the Three-Legged Stool

Titan Biotech Limited (BSE: 524717) is a 35-year-old Indian specialty-biotech manufacturer producing peptones, gelatin, microbial nutrients, and pharmaceutical inputs from its Bhiwadi plant, exporting into ~60 countries. Walk it through Akre’s three legs using the company’s audited FY25 numbers.

Leg One — Extraordinary Business. FY25 audited operating margin sits in the ~18–22% band, RoCE in the mid-twenties, RoE in the high teens. None of this is a single windfall year — the ten-year revenue CAGR is ~15%, the PAT CAGR ~29%, and BVPS has compounded ~9x in eleven years. The economics are structural: indigenous fermentation technology, ~34.5% export revenue across sixty-plus countries, and a niche product mix bulk Indian commodity players cannot replicate at the same purity grades. Leg One — clearly present.

Leg Two — Exceptional Management. The promoter family has held and increased its stake (latest shareholding ~63% with incremental purchases visible on BSE filings), the company has paid an unbroken dividend for fourteen consecutive years, director remuneration sits at ~₹4.56 crore — a conservative ratio well inside Section 197 limits — and audited related-party transactions are limited and disclosed. The vigil mechanism is filed under SEBI LODR Regulation 22, board meetings ran fourteen in FY25 (well above the four-meeting LODR minimum), chairperson independence structure is in place. Leg Two — clearly present.

Leg Three — Glorious Reinvestment Runway. Audited gross block stands at ~₹57 crore, CWIP at ~₹11 crore — a CWIP-to-gross-block ratio of ~19%, signalling an active, self-funded forward-capex pipeline rather than a stagnant asset base. Net debt-to-EBITDA is ~−0.75x (net cash, not net debt), borrowings cut by ~70% over the multi-year period, and the cash and investments war chest sits in the high-thirty-crore range. Cash conversion (CFO over EBITDA) prints ~103% — every rupee of operating profit converts to operating cash, the prerequisite for self-funded reinvestment. Asset productivity (sales-to-gross-block) ~3.76x. Leg Three — present, and arguably the most distinctive.

Pull the three legs together: an extraordinary specialty-manufacturing business compounding at structural high-teens RoCE, run by an owner-operator promoter family with fourteen-year governance hygiene, with a visible CWIP-funded reinvestment runway and a net-cash balance sheet to fund it. That is what Akre’s stool looks like when every leg is present in an Indian small-cap.

The Investor’s Takeaway

Akre’s three-legged stool is not a screener you can run on Screener.in. It is a habit of thought. When you study any Indian listed business, ask only the three questions in order:

One. Does the underlying business mechanic produce structural high returns on capital, durable across a full cycle? If no, stop reading. The stool tips on Leg One.

Two. Are the people running this business operators of integrity who behave as owners, with a documented track record of converting retained earnings into incremental value? If no, stop reading. The stool tips on Leg Two.

Three. Does the company have somewhere to deploy the next ten years of retained earnings at roughly the same high rate? If no, you may still own a fine dividend-yielding business, but you do not own a compounder. The stool tips on Leg Three.

The Indian market has perhaps three hundred listed equities that clear Leg One on the audited numbers. Of those, maybe a hundred clear Leg Two. Of those, perhaps thirty have a visible Leg Three runway. Your watchlist, if you are honest, should be no longer than thirty names. Mine is shorter.

Akre’s discipline is the antidote to the most common retail failure mode — falling in love with one quarter’s numbers, one management interview, or one thematic story. The stool forces you to test all three legs before buying, and to keep testing them after buying. The day any leg breaks, you sell. That is the entire compounder game, distilled into one wooden stool sitting on a desk in Virginia.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.