Value Investing — Educational Series

Picture a second-hand scooter parked outside a house. It will not start on the first kick. Some mornings the engine coughs and dies; other days it leaks oil onto the floor. The owner keeps spending on it — a new part this month, a fresh repair the next — because he is sure that one more fix will finally set it right. A year passes, then two. The scooter still sputters, the bills keep coming, and the promised day when it runs like new never quite arrives.

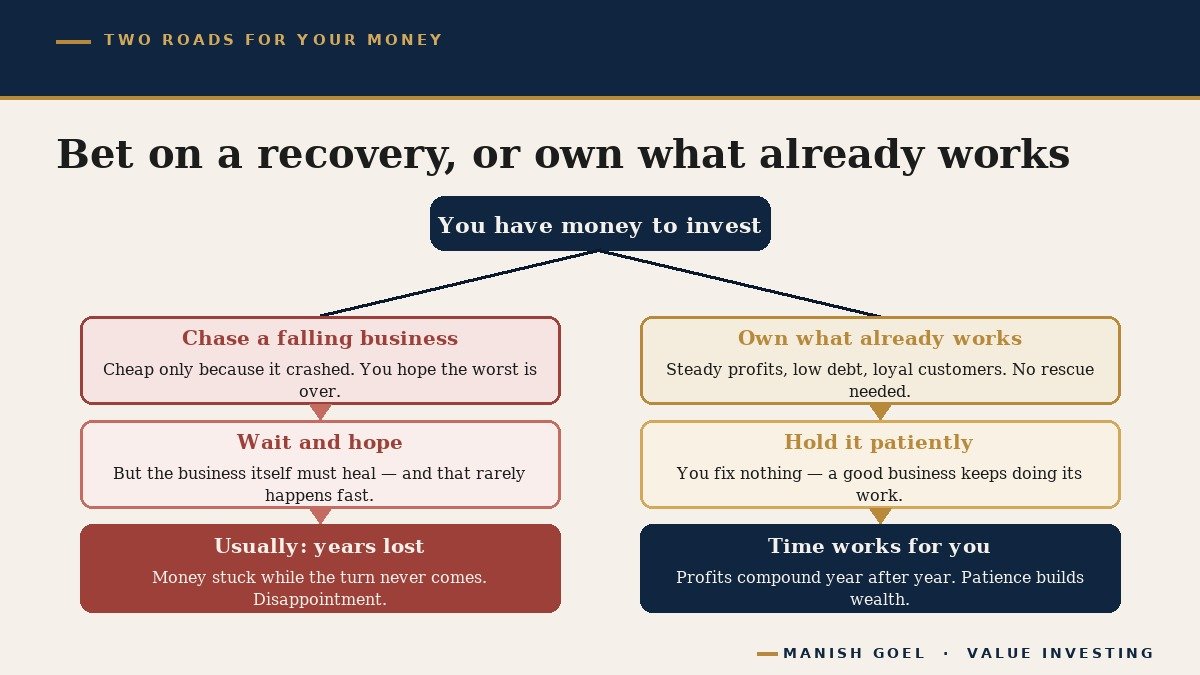

Many new investors in India buy shares the very same way. They are drawn to a company that is clearly struggling — falling profits, a sinking share price, a business in trouble — and they buy it anyway, gripped by a single hopeful thought: “It has fallen so much, surely it can only go up from here. The day it recovers, I will make a fortune.” In the stock market this hopeful bet has a name. It is called a turnaround — buying a weak, failing business in the hope that it will soon turn the corner and become strong again. (A share, remember, is simply a small ownership slice of a real company; when you buy one, you become a part-owner of that business, troubles and all.)

Today’s lesson is about one of the most expensive mistakes a beginner can make, and one of the simplest to avoid once you have seen it clearly. The greatest investors of all time learned it the hard way, with their own money, and then warned the rest of us in plain words. The lesson is this: turnarounds seldom turn. Let us understand why — and, far more usefully, what to do instead.

What a “turnaround” really means

A turnaround bet is, at heart, a bet on hope rather than on what is actually happening. You are not buying a business because it is doing well. You are buying it precisely because it is doing badly, while betting that the bad part is temporary and the good days lie just ahead. It is the financial version of adopting that troublesome scooter and trusting that the next repair will be the last one.

Warren Buffett — widely regarded as the greatest investor who has ever lived — put the warning as plainly as anyone could. Way back in his 1979 letter to the shareholders of his company, Berkshire Hathaway, he wrote: “Both our operating and investment experience cause us to conclude that ‘turnarounds’ seldom turn.” Notice the two words he leaned on — operating and investment. He had not only invested in struggling businesses; he had also rolled up his sleeves and tried to run one. From both sides of the table, he reached the same hard conclusion: a poor business almost never becomes a wonderful one just because a hopeful new owner wills it to.

This matters because a low price is so tempting. A share that once traded high and has now crashed feels like a bargain waiting to be grabbed. But a falling price is not, by itself, a reason to buy. The real question is never “How far has it dropped?” It is “What kind of business am I actually buying?” A great business going through a passing bad patch is one thing. A fundamentally weak business that is cheap because it deserves to be is something else entirely — and telling the two apart is the whole game.

Why a broken business so rarely heals

If turnarounds are so tempting, why do they so rarely work? The answer is that most struggling businesses are not struggling by accident. They are struggling for deep, stubborn reasons — a weak product nobody is loyal to, fierce competition that keeps prices low, a mountain of debt (money the company has borrowed and must repay with interest), or an industry where everyone fights hard and almost nobody earns well. These are not small dents you can hammer out in a weekend. They are built into the machine.

Buffett captured this with a beautiful, simple picture. When he finally shut down a failing business of his own, he wrote: “Should you find yourself in a chronically leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks.” Think about that. If your boat leaks from a hundred tiny holes, you can bail water all day and still sink. The wiser move is not to bail harder — it is to step into a boat that does not leak in the first place. He went further, adding that a good business record “is far more a function of what business boat you get into than it is of how effectively you row.” In other words: the boat matters more than the rower. Choose a sound boat, and even ordinary rowing carries you forward. Choose a leaking one, and the finest rowing in the world only delays the sinking.

A year earlier, in his 1980 letter, he had said the same thing about managers and businesses: “When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.” Read that twice. Even a brilliant manager usually loses to a bad business. And there is a second, quieter cost most beginners forget. While your money sits trapped in a turnaround that refuses to turn — for one year, three years, five — it is doing nothing. Every one of those years is a year it could have spent compounding inside a healthy business instead. (Compounding means earning a return on your past returns as well — like interest on interest, or a snowball growing heavier as it rolls downhill.) The loss you can see is the falling price. The far bigger loss you cannot see is all the growth you gave up while waiting.

Warren Buffett’s own ₹200-billion lesson

Here is the part that should reassure every beginner: Buffett did not learn this from a textbook. He learned it by making the mistake himself, in the most painful way possible. In fact, the company whose name is now famous around the world — Berkshire Hathaway — began life as exactly this kind of trap.

Back in 1965, Berkshire Hathaway was a tired old textile maker in America, its mills slowly losing to cheaper foreign cloth. Its shares looked cheap, and Buffett bought control of it as a classic turnaround bet — a struggling business he hoped to fix. He has since admitted that he even took control partly out of irritation, in a moment of stubbornness rather than cool judgement. Then he spent close to twenty years trying to make the textile business work. He poured in effort and money, patched leak after leak — and still the cheaper competition kept winning. Finally, in July 1985, he gave up and closed the textile operations for good. It was on that very occasion that he wrote the “leaking boat” line.

And the cost of that one stubborn turnaround bet? Buffett has called it the worst investment decision of his life. By his own later estimate, all the money and years he sank into a dying textile mill — instead of putting them straight into good businesses — may have cost him somewhere in the region of 200 billion dollars in growth he never collected. That is not a typo. The most successful investor in history was set back by a sum most countries would envy, all because a cheap, broken business tempted him into believing he could fix it. If it could happen to him, it can certainly happen to any of us — which is exactly why his warning is worth taking to heart.

The same trap, closer to home

You do not have to look across the ocean to see this lesson at work. It plays out on Indian screens every single day. A loss-making company’s share has fallen from ₹400 to ₹20, and a crowd rushes in, certain that such a low price must be a gift and that a grand recovery is around the corner. Sometimes the comeback is real. Far more often, the share drifts lower still, or simply sits like a dead weight for years, while the buyer keeps telling himself the turn is coming “next quarter.” The cheap price was not a hidden opportunity; it was the market’s honest verdict on a weak business.

India’s own seasoned investors learned to flip this thinking on its head. Raamdeo Agrawal, the well-known investor and co-founder of Motilal Oswal, built his entire approach around a simple checklist he calls QGLP — Quality, Growth, Longevity, and Price. Look closely at the order. Quality comes first. Price comes dead last; in his own words, “price comes last for me.” He insists on a genuinely good, well-run, growing business before he is willing to even think about what it costs. His motto for what follows is just as plain: “Buy right, sit tight.” Find a quality business, buy a piece of it, and then have the patience to simply hold it for years. That is the opposite of the turnaround gamble, which leads with a low price and merely hopes the quality will somehow show up later.

Notice what these masters, Indian and American alike, are quietly telling us. The skill that makes an investor wealthy is not the cleverness to rescue a sinking business. It is the patience and good sense to pick a sound one in the first place — and then to leave it alone and let it grow.

What to buy instead: three signs a business is already winning

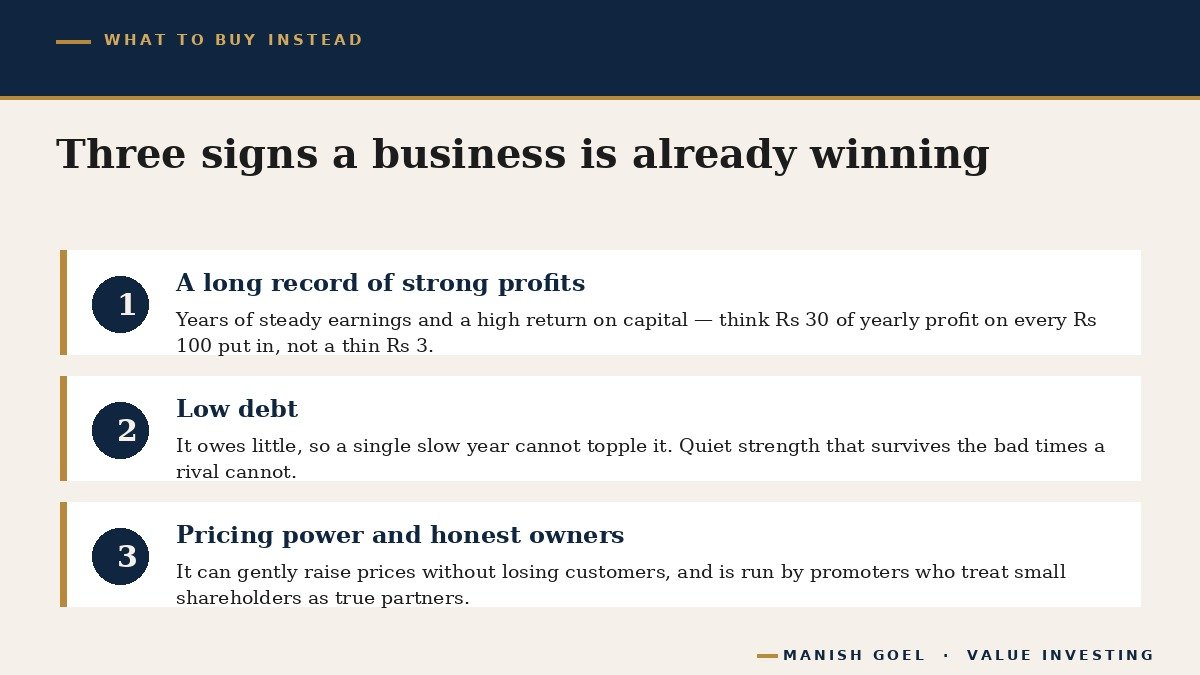

So if you should not chase the broken and the cheap, what should you look for? The happy answer is that spotting a business that is already doing well is far easier than predicting whether a sick one will recover. You are no longer playing fortune-teller; you are simply reading a track record that already exists. Here are three plain signs to look for — shown together below.

First, a long, steady record of real profits and a high return on capital. “Return on capital” simply means how much profit a business earns on the money put into it. Picture a kirana (neighbourhood grocery) shop that earns ₹30 a year on every ₹100 of goods on its shelves, against a struggling one that scrapes together only ₹2 or ₹3. The first is a money-making machine; the second is barely staying open. A business that has earned well, year after year, through good times and bad, is showing you in hard numbers that it is built to last — no hope or guesswork required.

Second, low debt. A company drowning in borrowed money is fragile: when business slows even a little, the loan repayments do not pause, and the whole thing can topple. A business that owes little can sail calmly through a bad year that would sink a heavily indebted rival. Low debt is not exciting, but it is the quiet strength that lets a good business survive long enough for compounding to do its work.

Third, pricing power and honest, capable management. Pricing power is the ability to raise prices a little each year without losing customers — the quiet strength of a trusted brand or a daily-need product people buy without checking the price tag. And behind every good business stand the promoters (the founding owners who control and run the company): you want them honest, capable, and treating small shareholders as true partners. A business with a loyal customer and a trustworthy owner does not need rescuing; it simply needs to be left alone to keep doing what it already does well.

How you can use this — three simple steps

First, change the question you ask. Before buying any share, stop asking “How much has this fallen?” and start asking “Is this a genuinely good business, doing well right now?” A low price is never a good enough reason on its own. If the only thing attractive about a company is that it has crashed, that is a warning, not an invitation.

Second, be deeply suspicious of the “story.” Turnaround bets always come wrapped in an exciting tale — a bold new boss, a clever new plan, a comeback that is always just one quarter away. Stories are cheap; track records are not. Trust the years of actual numbers a business has already put on the board far more than any promise about a future that has not arrived. As Buffett summed it up in his 1989 letter, after a lifetime of lessons: “Time is the friend of the wonderful business, the enemy of the mediocre.” Time heals the great business and quietly exposes the weak one.

Third, if you would not run it, do not rescue it. You do not have to pick individual companies at all to be a successful investor; many sensible beginners simply put a fixed sum every month into a low-cost index fund (a fund that quietly owns a whole basket of large, established companies for a very small fee) and let it compound for years. But if you do study a single business, hold it to the three signs above — strong profits, low debt, pricing power with honest owners — and then practise the hardest skill of all: patience. Pick a sound boat, and let it carry you.

Key takeaways

- A “turnaround” is a bet that a struggling business will recover and become strong again. As Buffett warned in 1979, turnarounds seldom turn — a poor business rarely becomes a great one just because a hopeful owner wishes it.

- A low or fallen share price is not a reason to buy. Most weak businesses are cheap because they deserve to be; the cheapness is the market’s honest verdict, not a hidden gift.

- Even Warren Buffett fell for it: his Berkshire Hathaway textile turnaround failed after twenty years, a mistake he reckons cost him in the region of $200 billion in growth he never earned. If it caught him, it can catch anyone.

- Spotting a business that is already winning is easier than predicting a recovery. Look for a long record of strong profits and high return on capital, low debt, and pricing power backed by honest, capable promoters.

- As India’s own Raamdeo Agrawal puts it, quality comes first and price comes last: “Buy right, sit tight.” Choose a sound boat and let time and compounding quietly do the work — no rescue required.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.