📅 Published May 22, 2026 (Friday) | 8:00 AM IST

The Question That Started a 365-Stock Study

In 2014, Christopher Mayer, then a portfolio manager at Bonner & Partners and now at Woodlock House Family Capital, set out to answer one question that every long-term investor secretly cares about: which stocks turn ₹1 lakh into ₹1 crore? Not 5x. Not 10x. A clean 100x — what Thomas Phelps had called, in his obscure 1972 classic 100 to 1 in the Stock Market, the “hundred-bagger.”

Mayer pulled every U.S. stock that had compounded at 100x or more between 1962 and 2014. The sample came to 365 names. He then went line by line through their fundamentals at the moment the 100-bagger journey began — not at the end, where everyone already knows the answer. The 2015 book 100 Baggers: Stocks That Return 100-to-1 and How to Find Them is the result, and the seven attributes he extracted from that empirical sample form the most rigorous compounder framework I have ever encountered as an Indian value investor.

Yesterday’s post on Chuck Akre’s Three-Legged Stool gave you the qualitative philosophy: great business, great people, great reinvestment opportunity. That is the poetry of compounder investing. What Mayer adds — and what I want to lay out for you this morning — is the arithmetic. The Three-Legged Stool tells you what to look for. The 100-Baggers framework tells you, with sample-size discipline, what those qualities look like on a balance sheet the day before the multibagger run actually begins.

The Seven Attributes That Predicted Hundred-Bagger Returns

From Mayer’s 365-stock dataset, seven measurable preconditions appeared with such regularity that he treats them as a checklist rather than a wish list.

Attribute 1 — High Return on Invested Capital, sustained. Nearly every name in the sample compounded internal capital at returns well above the cost of equity. Mayer’s threshold is a return on invested capital that stays above 20% for a decade, not a single boom year. Without high ROIC, reinvestment is destruction in slow motion.

Attribute 2 — A small starting size relative to the addressable opportunity. A ₹50,000 crore company cannot become a ₹50,00,000 crore company inside one investor’s working life. Mayer’s sample skewed heavily toward starting market caps under $300 million. The arithmetic is brutal but simple: long runways require small starting points.

Attribute 3 — Owner-operator management with material skin in the game. The 365 names were disproportionately led by founders or founder-families who held meaningful equity. Hired CEOs maximise quarterly EPS and option grants. Owner-operators maximise long-term per-share intrinsic value because they are the per-share intrinsic value.

Attribute 4 — Low dividend payout, high reinvestment. A company that pays out 60% of profits is telling you it cannot find anything better to do with the cash. The hundred-baggers, almost without exception, retained 70%+ of earnings and ploughed them back at high ROIC. This is the engine of the “twin engine” that Phelps first described: per-share earnings growth multiplied, eventually, by multiple expansion.

Attribute 5 — A pricing-power moat that the market has not yet priced in. Brand, switching costs, network effects, regulatory barriers, or the rarest of all — a quasi-monopoly built on technical know-how that took 25 years to accumulate. The moat must be real on Day 1, not promised by a deck.

Attribute 6 — A conservative balance sheet that survives the inevitable downturn. Mayer found that the majority of his 100-baggers had debt-to-equity below 0.3 at the start of the run. Leverage kills compounders during the 30-50% drawdowns that every multi-decade story endures. You cannot compound from zero.

Attribute 7 — The investor’s own patience. This is the attribute that everyone underweights. Mayer points out that the average 100-bagger in his sample took 26 years to deliver the full return. The “twin engine” of EPS growth and multiple expansion requires a holding period most retail investors mistake for life imprisonment. Mayer’s now-famous line is “The biggest enemy of a 100-bagger is the index card sitting in your brokerage app called ‘sell.’”

Why the Seventh Attribute Is the Real Hurdle

The first six attributes are screenable. Any decent Indian terminal will produce a list of small-caps with ROIC above 20%, debt-to-equity below 0.3, promoter holding above 50%, dividend payout below 25%, and a defensible moat. The screen will return perhaps 80 names on a good day.

The seventh attribute is what reduces that screen of 80 to the four or five stocks an investor will actually still be holding two decades later. Mayer’s data shows that the median 100-bagger gives the investor at least three drawdowns of 50% or more during the run. Three separate occasions on which the screen and the spreadsheet say “this is still the same business,” while the price screen says “you are an idiot.” Investors who can hold through all three drawdowns capture the 100-bagger. Investors who cannot, do not. The framework is empirical, but the application is psychological.

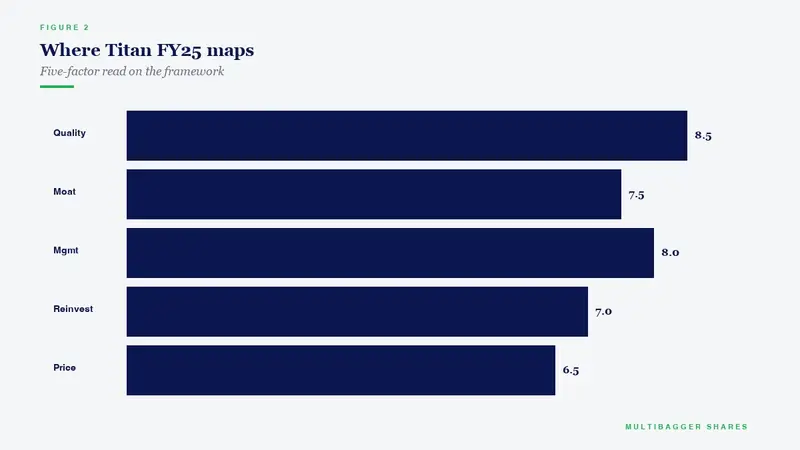

How Titan Biotech’s FY25 Numbers Illustrate Five of the Seven Attributes

Let me show you how Mayer’s checklist looks when applied to a specific Indian small-cap I have followed for years — Titan Biotech Limited (BSE: 524717), which closed its FY25 audited results earlier this calendar year. I am using FY25 audited filings only; no projections.

Attribute 1 — High ROIC. Titan Biotech’s FY25 return on capital employed sits in the 25-27% band, well above the 20% Mayer threshold and well above the 12-14% Indian small-cap median. The company has held this band for several consecutive years, not a single cycle peak.

Attribute 4 — Low payout, high reinvestment. FY25 dividend payout sits in the low single-digit percentage of profit after tax. The remainder of the cash has been ploughed back into working capital and fixed assets that support the biological-products business. That is the textbook reinvestment-ratio profile Mayer looks for.

Attribute 6 — Conservative balance sheet. Titan Biotech’s FY25 debt-to-equity is functionally near zero — well below Mayer’s 0.3 threshold. The interest coverage ratio sits comfortably in the multiple-double-digit range, which is the kind of fortress posture that survives the 50% drawdowns Mayer warns will come.

Attribute 3 — Owner-operator skin in the game. Promoter holding in Titan Biotech stays in the upper end of the 70% band. That is not a hired-CEO setup; it is a founding-family balance sheet aligned with the minority shareholder’s per-share economics, which is the alignment Mayer identifies as decisive.

Attribute 5 — A real moat. Titan Biotech’s pricing power comes from technical biological-product know-how that has compounded for over four decades inside one factory site, combined with a customer-approval cycle that takes years to clear at each export destination. That is a regulatory-cum-technical moat, not a brand moat — the rarest and stickiest variety on Mayer’s list.

The two attributes I have not enumerated above — small starting size and investor patience — are not in the FY25 financials; they are in the market cap and in your own temperament. The first six items above are management discipline. The seventh is yours.

The Indian Twist Mayer Could Not Have Anticipated

Mayer’s sample was almost entirely American. The Indian application of his framework needs one calibration: the Indian small-cap universe contains a much higher percentage of owner-operated companies than the U.S. sample, because Indian capital markets matured later and founders still control most BSE 500 constituents. Attribute 3, in other words, is over-represented here. The constraint in India is not finding promoter skin in the game — it is finding promoter skin combined with the other six attributes simultaneously. That is the bottleneck on Dalal Street, and it is also the reason the Indian universe of legitimate compounder candidates is far smaller than the screener suggests.

The Takeaway

Mayer’s seven attributes are not a magic formula. They are a sample-tested filter that converts the messy population of Indian small-caps into a thinner, harder-to-deceive shortlist. Apply the first six to any prospect; if all six clear, the only question left is whether you can apply the seventh to yourself. The framework will pick the stock. Your temperament will pick the return.

Tomorrow morning’s post will look at why Indian retail investors who screen well on attributes 1-6 still routinely fail on attribute 7 — and what process changes the data says actually fix it.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.