Value Investing — Educational Series

Imagine a sweet shop in your town called Sharma Sweets. For thirty years, people have crossed the whole city for its kaju katli. The shop earns well, the counter is always crowded, and the recipe is a family secret. Then one day, Sharma-ji looks at his growing pile of cash and makes an announcement. He is opening a mobile-repair counter inside the shop. Next month, a travel agency desk. The month after, he buys his cousin’s struggling furniture showroom.

Two years later, what do we usually see? The mobile counter loses money because Sharma-ji knows sweets, not circuit boards. The furniture showroom eats up the cash that the sweet counter earns. And because the owner’s attention is now split four ways, even the kaju katli is not what it used to be. The one great business he had is now paying for three weak ones.

The legendary American fund manager Peter Lynch had a funny name for exactly this mistake when companies do it. He called it diworsification — a play on the word diversification (spreading into many businesses), twisted to show that it usually makes things worse, not safer. He wrote about it in his famous 1989 book One Up on Wall Street, and warned: “Distrust diversifications, which usually turn out to be diworseifications.”

Lynch was worth listening to. From 1977 to 1990 he ran the Fidelity Magellan Fund (a mutual fund — a pool of money from many small investors that a manager invests on their behalf), and he earned about 29 per cent per year for thirteen years. That record made Magellan the best-performing mutual fund in the world at the time. Today’s lesson is one of his simplest and most useful: great companies usually stick to what they do best — and you should be careful when a company starts wandering into businesses it does not understand.

What “diworsification” really means

Diversification, in its original sense, is a sensible idea: do not keep all your eggs in one basket. But Lynch noticed that when companies use this word, it often hides something else. A company that earns a lot of cash from a strong main business gets restless. Instead of giving the extra money back to shareholders (the people who own the company’s shares), or investing it to make the main business even stronger, the managers go shopping. They buy other companies — often in fields they know nothing about — usually at high prices.

Lynch described the pattern bluntly: companies that try to grow this way “acquire other expensive companies, and then invariably, sell or ‘restructure’ by selling these acquisitions at a loss.” In other words, they buy in excitement and sell in regret.

Think of it like a family budget. A household earning well from one steady job suddenly takes the savings and puts them into a friend’s restaurant, a relative’s transport business, and a plot in a town nobody has visited. Each decision is sold to the family with one magic word: “growth”. But growth in a field you do not understand is not growth — it is gambling with extra steps.

Managers often justify these purchases with another magic word: “synergy” (the claim that two businesses joined together will somehow earn more than the two earned separately — the hope that two plus two will equal five). Lynch was deeply suspicious of this word. In real life, two plus two usually equals four, and after paying a fat price for the acquisition, it often equals three.

Why focused companies usually win

Why does wandering hurt so much? The logic is plain, and you already know it from daily life.

First, attention is limited. A great business is like a long cricket innings — it needs the batsman’s full concentration, ball after ball, year after year. A promoter (the main owner-manager of an Indian company) who is running a paint business, an airline, and a real-estate venture at the same time is playing three matches on three grounds at once. Something will be dropped.

Second, skill does not travel as easily as money does. A company that is brilliant at making biscuits has spent decades learning about flour, ovens, distribution vans, and kirana-shop shelves. None of that knowledge helps it run a software company. The cash can move to the new business in one day; the competence cannot. Management thinkers C. K. Prahalad and Gary Hamel called this deep, hard-earned skill a company’s “core competence” — the thing it can do better than almost anyone else. Move away from the core, and the company is an amateur again, competing against focused rivals who have done nothing else for decades.

Third, the strong business quietly pays for the weak one. This is the saddest part. The new venture rarely fails loudly on day one. Instead, year after year, the profits and loans raised on the strength of the good business are poured into the struggling one. It is like a fertile field being drained to water a barren one — at the end, you may be left with two tired fields instead of one rich harvest.

You can even see this logic in the numbers, without any advanced study. A focused quality business usually earns a high return on capital (the profit a company makes for every hundred rupees put into the business — like an FD that pays well, except the company built the FD itself). When that company pushes its money into a weak, unrelated venture, every new rupee starts earning a poor return. The blended result drifts downwards year after year. The company looks bigger — more factories, more press conferences, more headlines — but each rupee inside it is working less hard than before. Bigger is not better; better is better.

For you as an investor, there is one more problem. When you buy shares of a focused company, you know exactly what you own — Lynch’s golden rule. When you buy a company with seven unrelated businesses, you own a thali where you cannot taste any single dish properly, and where one bad dish can spoil the whole plate.

A real example or two

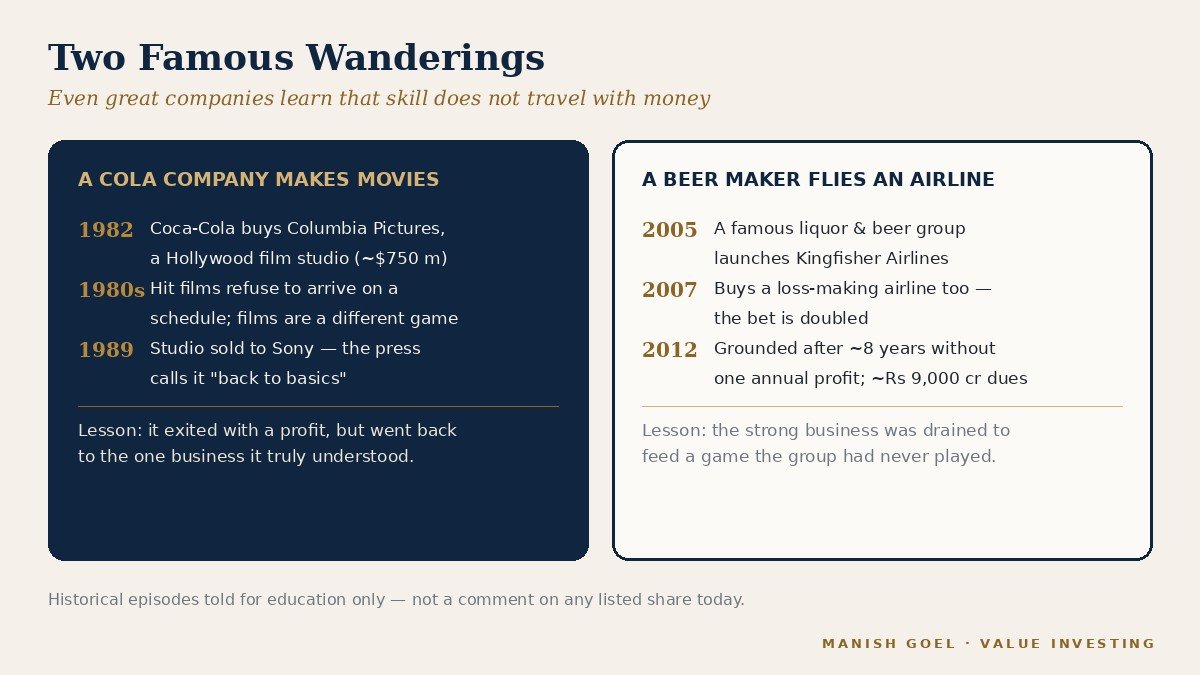

Start with one of the most famous companies on earth. In June 1982, Coca-Cola — the world’s best-known soft-drink maker — bought Columbia Pictures, a Hollywood film studio, for about 750 million dollars. The idea sounded exciting: a great marketing company would now market movies. But making films turned out to be a completely different game from selling a cold drink. Hit films could not be produced on a schedule the way bottles could. After years of mixed results, Coca-Cola stepped back, and in September 1989 the studio was sold to Sony. To Coca-Cola’s credit, it exited with a profit and the newspapers called it a return “back to basics” — but the bigger lesson stuck: even one of the world’s greatest companies found that money travels easily, skill does not. After returning to its core, Coca-Cola went on to create enormous wealth for shareholders by doing the one thing it understood best.

Now an example every Indian reader knows. United Breweries Group was a leader in one business it understood deeply — beer and spirits. In May 2005, its chairman Vijay Mallya launched Kingfisher Airlines. Aviation had glamour, but it was a brutally different business: aircraft bought with heavy loans, fuel prices the company could not control, fares set by cut-throat competition. In its roughly eight years of flying, Kingfisher Airlines never reported an annual profit. In 2007 it bought another loss-making airline, Air Deccan, doubling the bet. By October 2012 the airline was grounded, and banks were chasing dues of roughly nine thousand crore rupees. A famous, profitable group had poured the strength of its good business into a field it did not know — and lost both altitude and money. (This is told purely as a historical story, not as a comment on any listed share today.)

And the quiet opposite? Look at the companies that simply refused to wander. Asian Paints has essentially done one thing since 1942 — paint — and became one of India’s greatest wealth-creating stories by going deeper into that one trade instead of wider into many. Radhakishan Damani built DMart by selling everyday groceries well, and resisted every temptation to become everything else. Boring? Maybe. But in investing, boring focus has a long history of beating exciting wandering.

How you can use this lesson

You do not need any complicated maths to apply Lynch’s warning. Three simple habits are enough.

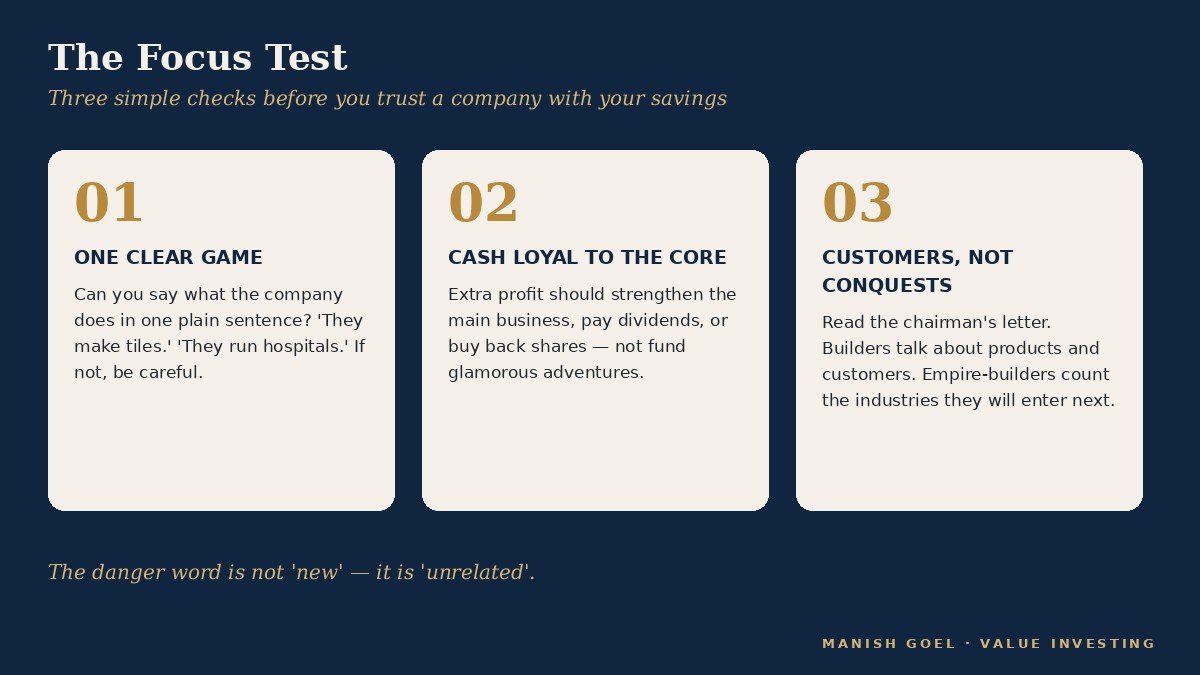

One: when you study a company, first ask — what is its one main game? Open the annual report (the yearly report card every listed company must publish) and look at where the sales and profits actually come from. If you cannot describe the company’s main business in one plain sentence — “they make tiles”, “they run hospitals”, “they sell scooters” — be careful. A company you cannot explain is a company you do not understand.

Two: watch what the company does with its extra cash. A quality business earns more money than it needs. The respectful uses of that money are: making the main business stronger, paying dividends (a share of profit paid to shareholders), or buying back its own shares. The warning sign is when the cash starts flowing into glamorous, unrelated adventures — an airline here, a real-estate arm there, a film studio for excitement. Ask the simple Sharma Sweets question: is this the kaju katli expert opening a mobile-repair counter?

Three: listen to how the promoter talks. Read the chairman’s letter in the annual report or a newspaper interview. Promoters of focused companies talk about customers, products, costs, and quality. Empire-builders talk about how many industries they will enter next. Lynch’s warning even appears in his selling checklist — he flagged “two recent acquisitions of unrelated businesses” as a classic danger sign. One unrelated purchase may be an experiment; a habit of them is a disease.

A gentle word of encouragement here. None of this requires you to be an expert. You judge focus every day without thinking — you trust the dosa stall that makes only dosas over the stall that sells dosas, chowmein, pizza, and momos from the same pan. Carry that same common sense into the stock market. It is one of the few areas where an ordinary investor’s everyday judgement is a real advantage, which is exactly why Lynch wrote his book for ordinary people and not for professionals.

One honest caveat so that we stay fair: not every expansion is diworsification. Moving into a neighbouring business that uses the same skills — a biscuit maker launching rusks, a two-wheeler maker selling spare parts — is often natural and healthy. The danger word is not “new”; it is “unrelated”. The further the new business sits from the company’s core skill, the louder your inner alarm should ring.

Key takeaways

- Diworsification is Peter Lynch’s word for companies that wander into unrelated businesses they do not understand — diversification that makes things worse.

- Money travels in a day, but skill takes decades — a champion in one trade is usually a beginner in the next, like a sweet-shop master repairing mobiles.

- The strong business quietly pays for the weak one, so the damage shows up slowly — in drained cash, rising debt, and a distracted management.

- History keeps teaching the same class: Coca-Cola had to hand films to Sony and go back to basics, while a great Indian liquor group lost thousands of crores flying an airline it never understood.

- Prefer companies with one clear game, cash that stays loyal to the core, and promoters who talk about customers — not conquests.

— Manish Goel

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.