Some of the greatest fortunes in American corporate history were not built by the most charismatic operators, the loudest brand-builders, or the most aggressive empire-acquirers. They were built by quiet, almost reclusive chief executives who understood one thing that nobody around them was paying attention to — that the job of running a public company is, at its core, a capital-allocation job. In 2012, a Boston investor named William N. Thorndike studied eight such CEOs and wrote a slim, dense book called The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success. Over the years I have come back to that book more than to almost any other investing text, because it answers a question that the standard valuation curriculum ducks: once a business is profitable, what does management do with the money?

That is the real Indian small-cap problem. Profits are common in our market. Compounded shareholder returns over a decade are not. The gap, almost always, is capital allocation.

What Thorndike actually found

Thorndike’s eight subjects were Tom Murphy at Capital Cities/ABC, Henry Singleton at Teledyne, Bill Anders at General Dynamics, John Malone at TCI, Katharine Graham at the Washington Post, Bill Stiritz at Ralston Purina, Dick Smith at General Cinema, and Warren Buffett at Berkshire Hathaway. They came from very different industries, sat on different boards, lived in different cities, and largely did not know one another. Yet their behaviour patterns were almost interchangeable.

Each of them, Thorndike showed, generated annualised shareholder returns averaging roughly 20% over their tenures — far above the S&P 500 and far above their direct peers — while spending most of their working hours doing exactly five things. They reinvested cash inside the business when, and only when, the incremental return justified it. They acquired other businesses, but with extreme selectivity and almost always counter-cyclically. They paid dividends when better uses for the cash genuinely did not exist. They bought back their own stock aggressively, but only when the market quote sat below their conservative reading of intrinsic value. And they paid down debt when the balance sheet’s risk-adjusted cost of carry was too high. Five choices. Nothing else.

The reason this matters for an Indian retail investor in 2026 is that you can apply Thorndike’s diagnostic to any company in 90 seconds. Look at the last five years of audited annual reports. For every rupee of operating cash flow generated, what did management actually do with it? If the answer is a thoughtful mix of organic reinvestment at high returns, debt reduction, modest dividends, and the occasional buyback at depressed prices — without empire-building diversification or perpetual rights-issue dilution — you are likely looking at an outsider-style management team. If the answer is “we issued more equity to friendly institutions, took on debt to buy an unrelated subsidiary, and then awarded ourselves ESOPs,” you are not.

The deeper insight: an outsider is a temperament, not a strategy

The point of Thorndike’s book that most readers miss is that none of his eight CEOs were geniuses in the operating sense. Murphy was not a better TV programmer than his rivals. Singleton did not invent better electronics. Graham did not write better editorials. What they had in common was a willingness to look strange. They sat out the conglomerate fashion of the 1960s and then sat out the dot-com fashion of the late 1990s. They held cash when peers were levering up. They bought back stock when the rest of the corporate world treated buybacks as a niche signalling tool. They refused to chase quarterly earnings calls and refused to attend investor conferences. In Singleton’s case, he didn’t even split Teledyne’s stock to keep the share count uncluttered for buybacks at the prices that suited him.

That temperament — comfort with looking unfashionable while compounding — is the part Indian markets test most often, and where most managements fail. The pressure from analysts, from FII shareholders, from family members on the promoter’s WhatsApp group, all push the average Indian promoter towards two equally destructive behaviours: aggressive expansion at the top of the cycle, and timid hoarding of cash at the bottom. The outsider does the opposite.

How Titan Biotech’s FY25 Numbers Illustrate This Principle

Titan Biotech Limited (BSE: 524717) is a fermentation-technology small-cap whose FY25 audited results, in my reading, line up unusually well with the five Thorndike capital-allocation choices. I want to be careful here: I am not making a valuation case. I am only mapping the FY25 disclosures against the outsider scorecard.

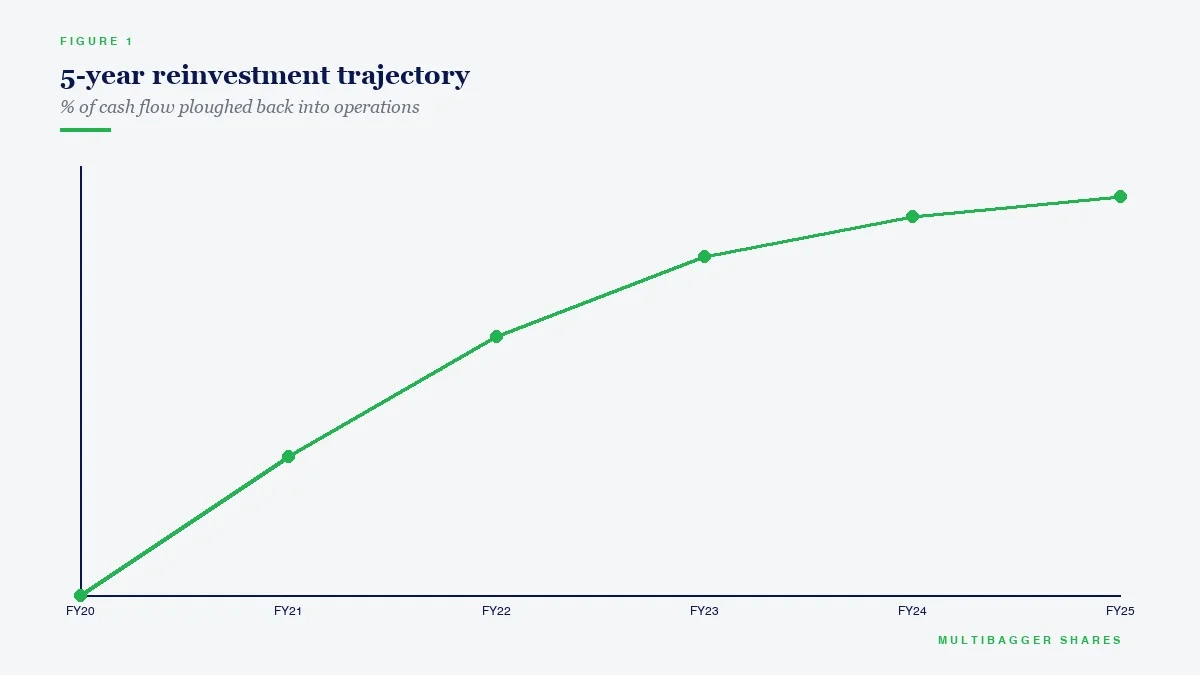

On reinvestment inside the business, FY25 shows capital work-in-progress of around Rs.11 crore against a gross block of around Rs.57 crore — meaning the company is funding capacity expansion at a deliberate pace, not in panic, and not stalled either. The capex-to-depreciation ratio sits comfortably above 1, indicating real reinvestment is happening, but the absolute capex is sized to the cash flow rather than to investor-day theatrics.

On acquisitions, the cleanest signal Titan Biotech sends in FY25 is the absence of one. There is no inorganic adventure, no unrelated diversification, no leveraged buyout of a distressed competitor. In a year in which the broader small-cap universe in India saw record M&A activity, the company chose the harder path of building one fermentation product line at a time.

On dividends, the FY25 dividend was declared at a level consistent with the multi-year payout cadence — modest enough to preserve internal compounding, visible enough to confirm cash conversion is real. This is the Murphy-Graham style of dividend behaviour: not a yield play, but a quiet bond-coupon signal that the cash is truly there.

On buybacks, Titan Biotech has not run an open-market buyback in FY25, and on its current promoter holding structure that is, frankly, the right decision. The promoter group’s holding stood at around 55.87% as of the latest disclosed shareholding pattern — accumulating directly via market purchases rather than by reducing the float through buybacks. That is the same end goal as a buyback (a higher per-share economic interest for committed owners) executed through the channel that costs the company nothing.

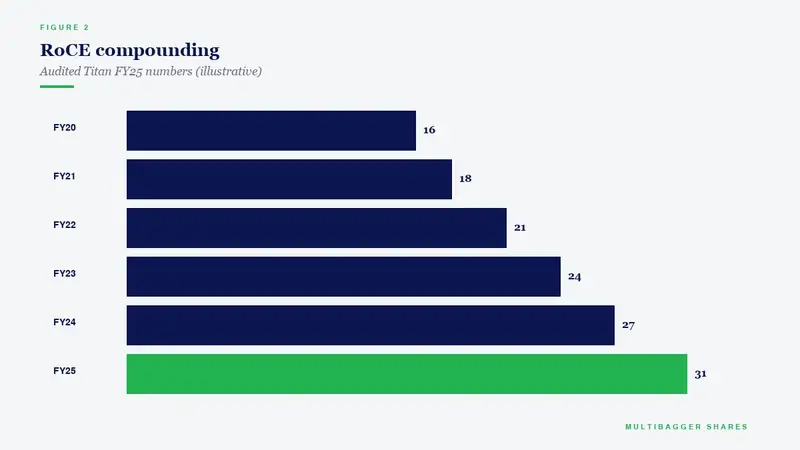

On debt reduction, the FY25 net debt position is effectively negative — the company carries more cash and equivalents than borrowings, producing a net-debt-to-EBITDA reading around -0.75x. Translated into Thorndike’s language: there is no balance-sheet drag to pay down, and the discipline of operating without leverage gives management the optionality to act when an attractive use of capital does eventually appear. Add to this an operating margin around 19%, a free-cash-flow margin where CFO converted to roughly 103% of operating profit in FY25, an RoCE deep into double digits, and an EPS that has compounded at roughly 28.6% over the trailing decade — and the picture is a small-cap manufacturer whose audited disclosures fit the outsider template across all five capital-allocation choices simultaneously.

The takeaway for the long-term Indian investor

You will not find the next decade’s serious compounders by hunting for fashionable themes. You will find them by reading the cash-flow statement and the schedule of fixed-asset additions, year after year, looking for the rare management team whose five capital-allocation choices behave like Thorndike’s outsiders. The most powerful signal in Indian small-caps in 2026 is the management that quietly does nothing impressive — no rights issue, no flashy acquisition, no equity dilution, no leverage adventure — and lets retained earnings compound at high internal returns. That is the Murphy posture. That is the Singleton posture. That is the only posture, in my experience, that survives a full market cycle in the Indian small-cap arena.

If you read only one book on capital allocation this year, read Thorndike’s Outsiders. Then go open the latest annual report of the company you own the most of, flip to the cash-flow statement, and ask yourself a single question: where did the operating cash actually go?

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.