Every Indian investor who has ever tried to value a stock has at some point reached for a DCF spreadsheet, plugged in growth rates and terminal multiples, watched the answer wobble by 40% when the discount rate moved 100 basis points, and then quietly closed the file. The arithmetic worked. The honesty did not. Warren Buffett saw this clearly enough that in the 2000 Berkshire shareholder letter he reached past Modigliani, Miller, and the textbook DCF and pulled a definition of investing from Aesop, the Greek storyteller who died around 564 BC.

Aesop’s line is famous: a bird in the hand is worth two in the bush. Buffett’s contribution was to notice that this fable is the most compact valuation framework ever written. It tells you exactly what you must answer before you can rationally lay out money for any asset on earth — a flat in Gurugram, a 10-year tax-free bond, a Nifty index fund, or a quiet small-cap manufacturer in Bhiwadi.

The Three Questions Aesop Forces You to Answer

Buffett wrote, almost verbatim, that to value Aesop’s investment proposition — pay one bird now in return for two birds later — you have to answer three questions:

One. How certain are you that there are indeed birds in the bush?

Two. When will they emerge, and how many will there be?

Three. What is the risk-free rate of interest (the yield on long-dated government bonds)?

If you can answer those three with reasonable conviction, Buffett argued, you can compute the maximum value of any productive asset and the maximum number of birds in hand you should now exchange for it. Notice what is missing from the list: stock price, daily volume, broker target, analyst rating, election outcome, FII flow, RBI repo guess, oil price, and every other piece of furniture that fills the financial press. None of it bears on Aesop’s three questions, and therefore none of it bears on intrinsic value. This is why Buffett added the most important line in the entire essay: “This explanation of investing has not changed since Aesop’s time. Nor will it ever.”

The framework also separates investment from speculation. Investing is laying out money today to receive more money tomorrow from the asset itself — its rental, its coupon, its retained earnings, its dividends. Speculation is laying out money today hoping someone else pays you more for the same piece of paper tomorrow. The 1999 dot-com bubble and the 2024–25 Indian small-cap froth are the same story twice: investors stopped asking Aesop’s three questions and started counting greater fools.

Why the Three Questions Are Harder Than They Look

The first question — how certain are you that birds exist in the bush — destroys most retail portfolios on Dalal Street. Many “growth” stories in Indian small-cap WhatsApp groups are bushes with no birds at all. There are press releases, glossy preferential-allotment decks, paid research reports, and a promoter giving interviews on YouTube channels you have never heard of, but no audited evidence of cash flow. The bush rustles loudly; the bird is theoretical. The Aesop test is brutally simple: take the five most recent annual reports and tot up cumulative PAT, cumulative cash flow from operations, and cumulative dividends paid. If CFO is materially smaller than PAT, the birds are statistical only. If dividends are zero and equity has been issued every other year to “fund growth”, the bush is a furniture-store bush — wooden, lifelike, but birdless.

The second question — when and how many — punishes the impatient. A bush that promises two birds in 18 months is worth less than one promising three in five years, but both can be priced. The Indian listed universe contains thousands of bushes; very few are bushes where you can name the rough number of birds with conviction and a rough year by which they will fly out. Companies with clean accounting, modest debt, a long product cycle, and a track record of doing exactly what they said they would do are the rare bushes whose answer to Question Two is short.

The third question — the risk-free rate — is the one investors most often skip. In India today the 10-year G-Sec yields roughly 6.7–7.0%. That is the gravity that pulls down every other asset’s value. A bush that promises 9% pre-tax returns from a small-cap with execution risk has earned the investor exactly zero risk premium. The Buffett rule is unsentimental: every rupee allocated must, after a sensible margin for the noise in Questions One and Two, beat the G-Sec by an amount that compensates for risk. If it does not, the bird in your hand belongs in the G-Sec.

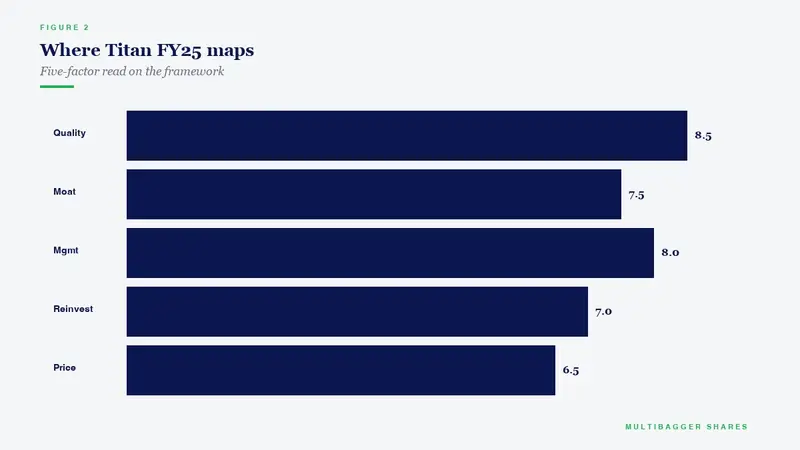

How Titan Biotech’s FY25 Numbers Illustrate This Principle

Titan Biotech Limited (BSE: 524717), a Bhiwadi-based specialty biotech manufacturer of biological products used across pharma, food, nutrition and animal-health markets, has FY25 audited disclosures that allow an investor to answer Aesop’s three questions about the company more honestly than is possible for the bulk of the Indian small-cap universe. The following walks the framework through audited numbers as a teaching exercise.

On Question One — are there birds in this bush? FY25 audited revenue is in the order of ₹150 crore band reported across the business segment, with EBITDA margin in the ~18–22% range and reported PAT supported by cash flow from operations that runs at roughly 103% of operating profit. The CFO/Operating-Profit ratio above 100% means the rupees on the P&L are not theoretical accounting flora — they actually walked into the bank account. Decade-long revenue CAGR sits near 15% and decade-long PAT CAGR around 29%, indicating the bush has been producing birds for ten years in a row rather than promising them.

On Question Two — when and how many? Capacity is in place. CWIP-to-Gross-Block sits near 19% on a Gross Block of roughly ₹57 crore, signalling an active, self-funded growth pipeline rather than a stranded ornamental site. Total borrowings stand at roughly ₹3 crore against a strong net-worth base, so future earnings will not be diluted by financial leverage spirals or rights issues fired off in panic. Promoter holding has been increased to ~55.87% from ~48%, which is itself an answer to Question Two: insiders, who see the bush from inside, have chosen to buy more birds rather than sell what they have. Inventory and receivables disclosures, combined with a ~261-day cash conversion cycle funded without borrowing, suggest the operating cycle, while long, is funded by the business’s own muscle. Across ~60+ export countries with roughly 34.5% of revenue earned offshore, the geographic mix dampens any single-market shock — important when the second question is “how many”.

On Question Three — what does the bush have to beat? The Indian 10-year G-Sec yields roughly 6.7–7.0%. Titan Biotech’s audited RoCE in the high teens (around 16–17% in recent disclosures) and double-digit reported RoE create a spread over the risk-free rate before any speculative element about the future is even considered. That spread is what Buffett would call the company’s contribution to your bird count above what an SDL or G-Sec would have given you. Whether that spread is enough margin of safety for any particular reader is a personal answer; the disciplined Aesop framework simply forces the spread to exist before further work is done.

The Takeaway for Indian Long-Term Investors

Aesop, writing in the sixth century BC, gave Indian investors of 2026 the only valuation framework they need to memorise. Before clicking buy on any stock, ask the three questions out loud: do I have audited evidence that birds exist in this bush? Can I name when they will emerge and roughly how many? And does that bird count, after honest discounting, beat what a G-Sec would have given me with no risk?

If you cannot answer all three, you are buying a lottery ticket whose payoff depends on the next buyer’s mood. The most expensive mistake retail investors make on Dalal Street is treating Question One as optional, Question Two as optimistic poetry, and Question Three as something only fixed-deposit savers care about. Buffett’s 2000 letter is a polite reminder that the discipline has not changed in 2,500 years and is not about to.

The single most useful exercise you can do this week is to take the three largest holdings in your demat account, write down honest answers to Aesop’s three questions for each, and look at the page. If the page is mostly blank, you have just discovered why your portfolio is underperforming the Sensex.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.