In January 1972, Warren Buffett wrote a cheque for $25 million to buy a chocolate company. Charlie Munger had to drag him to that decision. Berkshire Hathaway’s books had never seen a price like it for a business with only $8 million in tangible net worth. By any Benjamin Graham filter, the deal was indefensible — more than three times book value, no margin of safety in the asset sense, and a price-to-earnings multiple that would have made a 1950s value investor pour another whisky.

That cheque was the most important $25 million Buffett ever spent. Not because of the cash it generated — though See’s Candies has now sent back more than $2 billion to Omaha over the decades. It mattered because the act of writing it pivoted Buffett’s mind from the Graham doctrine of buying cheap statistical bargains to the Munger doctrine of paying a fair price for a wonderful business. Every single thing he has done since then — Coca-Cola in 1988, Apple in 2016, the long Burlington Northern accumulation — rests on that mental shift made in a Pasadena candy shop.

I want to spend today’s letter on this pivot, because almost every Indian retail investor I meet is still operating in the pre-See’s Candies mindset. They are hunting for low price-to-book ratios in industries that are dying, congratulating themselves on a 4× book purchase that turns out to be a 4× book purchase of a permanently impaired business. They believe they are being conservative. They are not. They are being lazy.

The Graham mindset: buy cheap, sell at fair value, repeat

Benjamin Graham taught his students — Buffett included — to treat a stock as a piece of a balance sheet. Find a business trading below liquidation value. Buy it. Wait for the market to mark it back up to a sensible price. Sell. Move on. Repeat with the next statistical bargain. The framework was magnificent for the post-Depression United States, where dozens of companies traded below the cash sitting in their own bank accounts.

The framework had two silent assumptions, and both broke down by the late 1960s. First, that the market would always throw up enough bargains to keep a portfolio fully invested. Second, that the underlying businesses, however ugly, would not deteriorate faster than the catalyst could realise value. By the time Buffett wound down his partnership in 1969, both assumptions were dead. Statistical bargains had thinned out. And many of the “cheap” companies he had owned — textile mills, trading stamp businesses, second-tier department stores — were melting ice cubes that destroyed capital faster than any re-rating could rescue.

Munger’s intervention: quality is not a tax, it is a refund

Charlie Munger spent the late 1960s telling Buffett a heretical thing: that the price you pay for a great business looks expensive on a single year’s earnings and ridiculous on a ten-year hold. Munger had been buying Blue Chip Stamps, watching how a customer relationship compounded across decades. He kept pointing out that a 15 P/E multiple paid for a business that could grow earnings at 12% per year — without consuming much fresh capital — would be effectively a 5 P/E by year seven, and an absurd bargain by year fifteen. The math was unforgiving in his favour.

See’s Candies was the test case. The Mathilde See family wanted $30 million; Buffett refused to pay above $25 million. (He has admitted publicly that if the family had held firm at $30 million, he would have walked, and the entire arc of Berkshire would have been different.) The business had pricing power, a beloved brand on the West Coast, a tiny capital base, and management of unimpeachable integrity. It produced $4.2 million of pre-tax earnings in 1972 on $8 million of operating assets — a return on tangible capital of more than 50%.

That last number is the whole game. A business that earns 50% on its operating assets and can pour incremental rupees back at similar returns will, over twenty-five years, turn one rupee of retained earnings into something that has nothing to do with the original price paid. The “expensive” entry multiple becomes irrelevant. The “cheap” cigar-butt with a 10% return on capital, by contrast, retains rupees that go nowhere. The cigar-butt investor has to keep finding new bargains; the wonderful-business owner just has to sit still and not interfere.

Why this pivot matters more in India than in the United States

India is structurally less efficient than the American market of 1972 — we still get genuine quantitative bargains in microcaps and forgotten sectors. Some investors will continue to do well buying Graham-style net-nets in India for another decade. But the long arc favours the See’s Candies framework here for one reason that is rarely articulated: tax. In India, a long-term capital gains rate of 12.5% on equity beyond one year, with no indexation, is a punishing tax on portfolio turnover. The cigar-butt investor who rotates capital every eighteen months pays this tax over and over, compounding it into a meaningful drag. The wonderful-business owner who holds for fifteen years pays it once. The arithmetic of post-tax compounding alone forces an Indian investor towards the Munger framework whether they like it or not.

And the structural opportunity is real. India has roughly 5,400 listed companies on the BSE. Perhaps 150 of them have the See’s Candies attributes — durable pricing power, modest capital intensity, clean governance, founder-managers with skin in the game, and the patience to reinvest at high incremental returns. The Indian value investor’s job is not to find a thousand cheap statistical bargains. It is to identify those 150 businesses and decide which fifteen deserve a portfolio allocation.

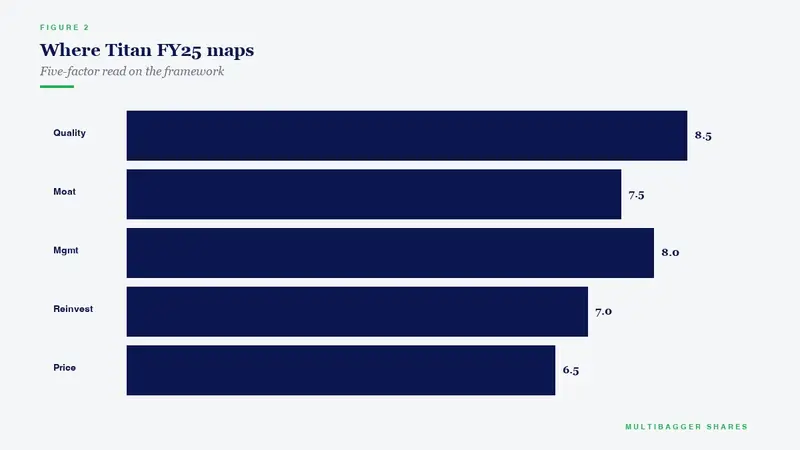

How Titan Biotech’s FY25 numbers illustrate this principle

Titan Biotech is a useful reference business when teaching the wonderful-business framework, because its FY25 audited financials show the exact economic shape that Munger described to Buffett in 1971. I am not claiming the stock is cheap, expensive, or anything in between — valuation is the reader’s own job. I am pointing out the operating chassis.

The company reported FY25 revenue of approximately Rs 165 crore, growing at a multi-year CAGR in the mid-teens. The operating profile is unusually clean: EBITDA margin near 19%, return on capital employed of about 16.9%, and a debt-to-equity ratio of 0.02× — effectively a net-cash balance sheet with a treasury position of roughly Rs 38 crore against negligible borrowings. The promoter family has been buying, not selling, increasing their stake from around 48% a decade ago to 55.87% today — the kind of behaviour Munger looked for at See’s. Export revenue contributes roughly 34.5% of the top line, spread across 100 countries, removing the single-customer fragility that often plagues Indian small-caps. Working capital discipline is visible in the cash conversion cycle, and the dividend record is unbroken across fourteen consecutive years.

What makes this an illustrative chassis, in the See’s Candies sense, is not any single metric. It is the combination: a business that can grow without consuming external capital, run by owners who behave like owners, earning a return on operating assets meaningfully above its cost of capital, with an honest accounting trail that has not required restatements or auditor changes. That is the operating shape Munger taught Buffett to recognise. Whether such a business deserves a premium multiple on any given day is the market’s question. Whether the underlying machine is a quality compounder is a different question entirely — and the FY25 numbers answer that second question in the affirmative.

The takeaway every Indian value investor needs to internalise

Stop looking for cheap stocks. Start looking for wonderful businesses, and then wait patiently for the market to offer you one at a price you can live with. Most days the market will not cooperate. That is fine — sit on your hands. The cigar-butt investor’s portfolio is a permanent flea-market scavenge; the wonderful-business owner’s portfolio is a quiet vault that compounds while they sleep. Both can make money in India; only one can make generational wealth.

The See’s Candies cheque in 1972 was the single most consequential trade of Buffett’s career, not because of the chocolate, but because of the framework it forced into his head. Every Indian investor who is still buying low P/E garbage in dying industries needs to write their own See’s Candies cheque — metaphorically — this year. Identify one business of genuine quality. Pay a fair price. Stop trading it. Watch the math go to work.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.