Most Indian retail investors look at a quarterly result, see a margin dip or a flat top-line, and immediately ask the wrong question: “Has the business broken?” The right question — the one Tom Russo has been asking for forty years at Gardner Russo & Quoss while compounding capital in Nestlé, Heineken, Pernod Ricard and Berkshire — is: “Is management spending today’s reported earnings to widen tomorrow’s moat?” That single reframing is the heart of a value-investing principle I want every long-term Indian investor to internalise this morning: Capacity to Suffer.

The Principle: Capacity to Suffer, in Plain English

Thomas A. Russo, the partner at Gardner Russo & Quoss whose family-controlled compounders portfolio has run for over four decades, coined the phrase Capacity to Suffer to describe a very specific corporate trait. A company has Capacity to Suffer when its management, controlling shareholders, and board are willing to accept depressed near-term reported earnings — sometimes for years — in order to fund initiatives that will only pay back over a multi-decade horizon.

Russo’s claim is sharper than it first appears. He is not saying that every loss-making investment is a capacity-to-suffer investment. He is saying that the rarest and most valuable corporate trait is the institutional willingness to be misunderstood for five, seven, or even ten years while a brand is built, a distribution network is laid down, a research pipeline is matured, or a new geography is colonised. The capital is being spent on real, durable, hard-to-replicate assets — but the income statement looks worse, not better, during the spending years.

The structural reason most listed companies cannot suffer is brutally simple: their boards report to a public-market shareholder base that punishes quarterly misses. CFOs are graded on near-term EPS. CEOs are compensated on three-year share-price grants. The result is what Charlie Munger called “the most powerful corrosive in capitalism” — managements that under-invest in the very assets that would compound shareholder wealth for decades, simply to protect the next four quarterly reports.

Russo’s portfolio companies — Nestlé in its multi-decade emerging-markets push, Heineken in its Latin-American and African build-out, Pernod Ricard’s premium-brand cultivation in India and China, Brown-Forman’s brand investments before each price increase — all share one feature: each had a long stretch where reported margins were lower than they “should” have been, because management was deliberately spending against the future. The investors who saw past that drag captured decades of compounding. The investors who fled when margins compressed missed it.

Why It’s Almost Always the Owner-Operator

Russo observed something else: Capacity to Suffer is almost always found in owner-operated or family-controlled businesses. A salaried CEO with a five-year mandate cannot tolerate a seven-year payback. A promoter family thinking in generations — children, grandchildren, the family name on the front gate — can. It is no coincidence; it is the structural answer to the agency problem that Berle and Means first identified in 1932.

In the Indian small-cap universe, this is why obsessive long-term investors weight promoter quality, promoter holding stability, and the absence of share pledging so heavily. Those three signals are proxies for the capacity to suffer. A promoter who has not pledged a single share, who has held his stake for two decades without dilution, and whose family is the public face of the business has the structural latitude to accept a soft quarter in exchange for a stronger decade.

How Capacity to Suffer Shows Up on a Balance Sheet

The trait is not abstract. There are four observable signatures on any audited Indian balance sheet that signal a management with the capacity to suffer:

- A live capital-work-in-progress (CWIP) line that is meaningfully positive — meaning capex is being deployed faster than depreciation, with some assets not yet revenue-generating.

- Cash and investments accumulating internally — funded by operating cash flow rather than fresh debt, providing the optionality to keep investing even when the cycle turns.

- R&D, brand-building, or capacity-expansion outflows visible in the cash flow statement at a pace that depresses the current year’s operating margin.

- A multi-year revenue and PAT track record showing that the prior “suffering” cycles eventually translated into compounding growth — i.e. evidence the management has done this before and earned the right to do it again.

None of these are esoteric metrics. Every one of them sits on the audited annual report of every listed Indian company. The reason most retail investors miss the signal is that they read the P&L without reading the cash flow statement, and read the cash flow statement without reading the balance sheet. Russo’s discipline is to read all three together and ask: is this management willing to suffer today for a moat tomorrow?

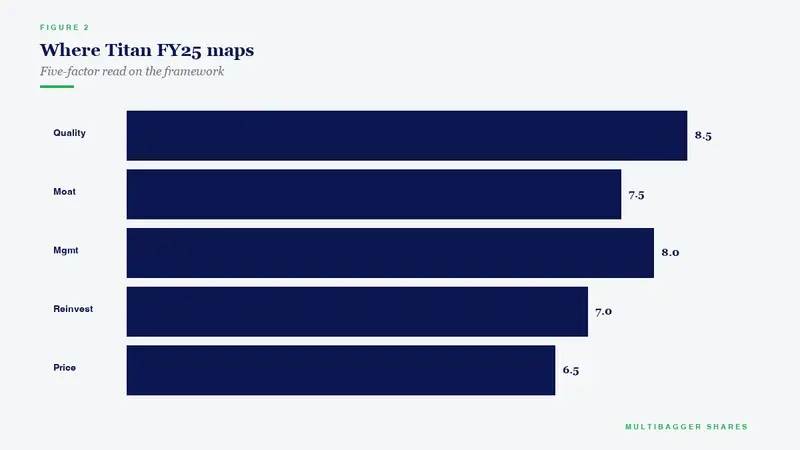

How Titan Biotech’s FY25 Numbers Illustrate This Principle

Titan Biotech Limited (BSE: 524717) — the Bhiwadi-based specialty-biotech manufacturer that exports peptones, amino acids, and biochemicals to more than sixty countries — is a textbook live illustration of the capacity-to-suffer signature on an Indian small-cap balance sheet. The FY25 audited disclosures display every one of the four signatures Russo would screen for, and several more besides.

Reading from the FY25 annual report, here are the audited markers a capacity-to-suffer investor would pull off the page:

- Capital Work-in-Progress of approximately ₹11 crore — sitting on a gross block of approximately ₹57 crore. That is a CWIP-to-gross-block ratio of roughly 19%, signalling an active, internally funded capex pipeline rather than a stagnant asset base.

- FY25 cash flow from operations to operating profit ratio of approximately 103% — operating cash exceeds reported operating profit, meaning earnings are not just accrued but converted to cash before reinvestment.

- Net cash position of approximately ₹35 crore against total borrowings of approximately ₹3 crore — a negative net debt that gives management the latitude to keep investing through any cycle without lender pressure.

- Promoter holding consistently in the 73–74% range with zero share pledging — the structural prerequisite for owner-operator-style long-horizon thinking that Russo demands.

- Approximately ten-year revenue CAGR near 15% paired with a ten-year PAT CAGR near 29% — proof that prior cycles of capex and capacity build-out have translated into earnings compounding, not earnings dilution.

- Export revenue mix of approximately 34.5% across more than sixty countries — geographic diversification that did not exist a decade ago and required years of unglamorous regulatory filings, customer qualification, and distribution build-out.

- Manageable director remuneration of approximately ₹4.56 crore against PAT, well within Section 197 ceilings — a sign that the promoter family is taking the long view of family wealth tied to share price compounding rather than salary extraction.

- RoCE consistently above the Indian 10-year G-sec hurdle rate, meaning incremental capital deployed is genuinely creating value rather than diluting returns.

- EBITDA margin in the 18–22% band — held steady even during years of active capacity expansion, indicating the suffering is being absorbed without breaking the operating model.

What stands out for a Russo-style reader is the combination. Many Indian small-caps have one or two of these markers. Very few simultaneously display an active capex pipeline, net cash on the balance sheet, 103% cash conversion, owner-operator promoter discipline, and a decade-long compounding track record. The combination is the signal.

The Takeaway for the Indian Long-Term Investor

Capacity to Suffer is not a metric you can calculate to two decimal places. It is a posture — the willingness of a promoter family and its board to be temporarily misunderstood by the quarterly-EPS crowd in exchange for a decade of compounding. The investor’s job is to identify managements that have this posture, give them time, and not flinch when a single quarter looks soft because capex is biting margins.

If you are building a long-term equity portfolio in 2026, the question you must learn to ask of every name you hold is not “what did EPS do this quarter?” but “is this management spending today’s earnings to widen tomorrow’s moat — and have they done it before?” When the answer to both halves of that question is yes, you are likely holding a compounder. When the answer is no, you are likely holding a salaried-CEO business that will under-invest its way to mediocrity, no matter how clean the next four quarterly reports look.

Tom Russo’s contribution to the value-investing canon is to give us a name and a framework for what Buffett, Munger and Fisher have all been gesturing towards for sixty years: the rarest, most valuable corporate trait on earth is the institutional willingness to take a temporary hit to reported earnings in order to build something that will still be standing — and still earning — long after the analysts who downgraded the stock have moved on to other names.

That posture is what separates a compounding machine from a quarterly-earnings machine. As an Indian long-term investor, the discipline is simple: identify it, hold it, and stop flinching at the noise.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.