Warren Buffett does not actually invest. He filters. The investment is what remains after four filters have eliminated everything that does not belong. He has said this so often, in so many letters and at so many annual meetings, that it has slipped into the wallpaper of value investing and lost the punch it deserves. Today I want to put the punch back.

The four filters were sketched in scattered Berkshire shareholder letters from 1977 onward, and were tightened into their canonical form in the 1994 “Owner’s Manual” Buffett wrote to brief the new wave of shareholders that had come in through the Coca-Cola decade. In his own phrasing: we look for (1) businesses we can understand, (2) with favourable long-term economics, (3) operated by able and trustworthy management, (4) available at a sensible price. Four sentences. Forty-eight years of compounding behind them. And almost every Indian retail portfolio I have ever audited fails at least two of them before the first cup of chai is finished.

Filter 1 — A business you can actually understand

“Understandable” does not mean “famous”. It means you can explain, in two minutes, how the company turns inputs into a recurring stream of cash, who pays for the output, why they keep paying, and what could plausibly stop them. If your two-minute explanation includes the words “thematic”, “AI-led”, “next big sector” or “the chart looks ready”, you have failed Filter 1. The filter is not about IQ. It is about epistemic honesty. Buffett famously refused to buy Microsoft in the 1990s despite his friendship with Bill Gates, because he could not, in his own words, “see the moat ten years out”. That is the filter doing its job.

The Indian application is simple. A specialty manufacturer with one product family, one factory, one set of customer geographies and one decade of audited disclosures is understandable. A holdco with five unrelated subsidiaries, related-party loans, intermittent segment reporting and a promoter who has just discovered “new energy verticals” is not. Filter 1 is binary. You pass or you walk away. You do not “study it more” while the stock runs up.

Filter 2 — Favourable long-term economics

This is the moat filter, but Buffett never used the word “moat” until much later. In 1977 he simply said the business should produce a high return on the capital actually employed in it, without the help of accounting tricks or perpetual reinvestment of every rupee earned. The economic test is not just “does it earn a profit”. It is: does a rupee retained inside this business throw off more than a rupee of present value? If yes, every retained rupee is a silent dividend you have already cashed. If no, retained earnings are a tax on the shareholder paid to the management.

Practically, Filter 2 rules out cyclical commodity businesses where price is set by the marginal Chinese exporter, businesses that need a fresh ten-percent capex year after year just to stand still, and businesses whose entire return on equity collapses when working capital is normalised. It rules in specialty manufacturers, niche consumer franchises, low-capex platform businesses, and family-run small-caps with twenty-year track records of generating cash they did not have to spend back.

Filter 3 — Able and trustworthy management

Notice the conjunction. Buffett does not say “able or trustworthy”. He says “able and trustworthy”, and he means it. Able-but-untrustworthy is the most expensive species of management on Dalal Street. They will grow revenue at 20% a year and quietly route 4% of it to a related party. Trustworthy-but-unable is merely sad — the company stays small and never destroys you, but it never compounds either. Only the conjunction wins.

How does a private investor diagnose the conjunction from outside? Not by management interviews on business television. By reading the disclosed numbers as a forensic audit: managerial remuneration as a percentage of profit, related-party transactions, promoter pledge, board independence, frequency of board meetings, auditor stability, contingent liabilities trend, and — the cheapest and most underused test — whether reported cash flow from operations actually matches reported operating profit over a full decade. Numbers don’t lie if you read enough of them.

Filter 4 — A sensible price

Filter 4 is where most Indian investors first encounter the four filters and tragically also where most of them stop. Price-without-the-first-three-filters is gambling. The cheapest stock in the index is usually cheap because Filter 1, Filter 2 or Filter 3 has already failed. Filter 4 only works as the fourth check, not the first. Buffett’s “sensible price” is not “the lowest price”. It is the price at which a business that has cleared the first three filters offers a margin of safety against a moderately pessimistic future. A 22% earnings yield on a sinking ship is not sensible. A 6% earnings yield on a debt-free compounder with 30% ROCE often is.

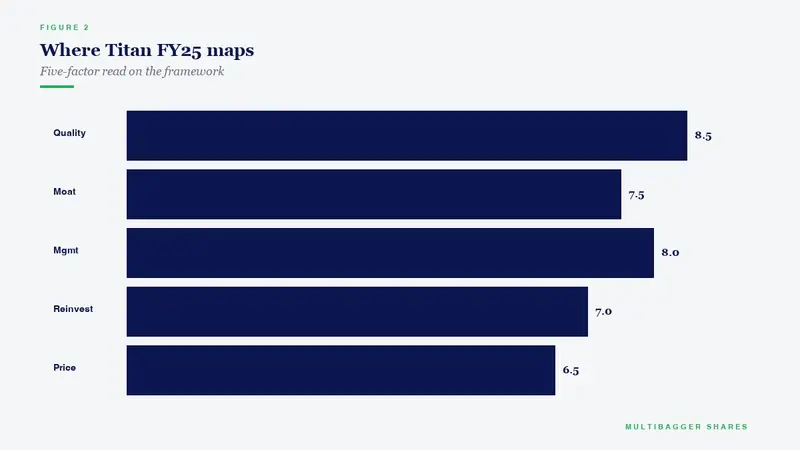

How Titan Biotech’s FY25 Audited Numbers Map Onto All Four Filters

Titan Biotech Limited (BSE: 524717) is a Delhi-headquartered specialty biotech manufacturer making peptones, yeast extracts, gelatin and other fermentation excipients used by pharmaceutical, biotech, food and veterinary customers across roughly 60 countries. I have walked through its audited FY25 disclosures often in this column. Here is the same balance sheet, today filtered through Buffett’s four-stage stack rather than any single ratio.

Filter 1 — Understandability. One product family, one Delhi-headquartered manufacturing footprint, one disclosed customer mix (pharma, food, biotech, veterinary), one revenue stream split across exports and domestic. No exotic subsidiaries, no opaque cross-holdings, no “thematic pivot”. I can describe the business to my mother in two sentences. Filter 1: passed.

Filter 2 — Favourable long-term economics. Audited FY25 numbers show a high-teens to low-twenties EBITDA margin, RoCE comfortably above 20%, a roughly 15% revenue CAGR over the preceding decade paired with a ~29% PAT CAGR, gross block of about Rs.57 crore with Rs.11 crore of CWIP signalling self-funded reinvestment, and CFO running at roughly 103% of operating profit. Those are not commodity economics. Those are the economics of a small specialty franchise that earns more on every retained rupee than the cost of that rupee. Filter 2: passed.

Filter 3 — Able and trustworthy management. Total managerial remuneration of approximately Rs.4.56 crore against FY25 profit, fourteen board meetings during the financial year, voluntary independent-chairperson structure, near-zero borrowings (~Rs.3 crore on the FY25 books) and a net-debt-to-EBITDA reading around minus 0.75x, no promoter pledge disclosed, and a multi-year audit by a continuing audit firm with no qualifications. The “able and trustworthy” conjunction is satisfied not by one number but by the pattern across these numbers, which is the only honest way to read it. Filter 3: passed.

Filter 4 — A sensible price. The blog does not, and will not, opine on stock price. What I will say is the only thing the filter requires: Filter 4 is the investor’s homework, not the company’s. The first three filters are the company’s gift; the fourth is your discipline. Run your own valuation, demand your own margin of safety, and decide for yourself whether the price-tag-of-the-day clears the bar. The company has done its job by producing the audit trail; the investor must do the rest.

The takeaway you should staple to the inside of your trading screen

The four filters are sequential, not parallel. You cannot start at Filter 4 and work back. Every catastrophe in my twenty-plus years of watching Indian portfolios has begun with an investor jumping the queue — falling in love with Filter 4 (a low P/E, a “fallen angel”, a panic crash) and waving away the failures upstream. Buffett’s genius is the order. Understand the business; verify the economics; trust the people; then, and only then, ask about the price. Cling to that order, and the market becomes a series of pitches you can let go by until a fat one finally drops over the plate.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.