Seth Klarman is the most successful value investor most Indian retail investors have never heard of. His 1991 book Margin of Safety is out of print, second-hand copies routinely trade for thirty thousand rupees on eBay, and his Baupost Group has compounded capital at low-double-digit returns for over four decades while holding meaningful cash for years at a stretch. The reason his record is so quietly extraordinary is also the reason most amateur investors will never replicate it. Klarman did not just borrow Benjamin Graham’s margin-of-safety idea and apply it harder. He rebuilt the entire architecture of value investing around three pillars that work as a single integrated system. Today I want to walk you through what that architecture actually says, why it is the highest-resolution operating system available to a private Indian investor, and how one ordinary BSE-listed small-cap’s audited FY25 numbers illustrate every one of its principles.

The Three Pillars Klarman Built

Most readers think Klarman’s book is a longer, glossier explanation of Graham’s “buy a sixty-paise rupee” idea. It is not. Read the contents carefully and you discover three foundations that do not appear in The Intelligent Investor at all. Klarman names them in the opening chapters with the calm precision of a man who has thought about each one for a thousand sleepless Sunday nights.

Pillar one is the absolute-return mindset. Klarman refuses to measure his performance against any index, any benchmark, any peer fund. The Nifty 500 had a wonderful 2023 and a miserable 2025. Both years are useless reference points for whether a value investor is doing well. The only honest question is: did the underlying businesses I own get more valuable, did I pay less than that value, and did my capital base grow in absolute terms? Benchmarking against an index forces a manager to own the index’s mistakes. Klarman simply refuses to play that game.

Pillar two is bottom-up bargain hunting. Klarman does not start with a macro view of GDP, the rupee, or where the RBI will set repo rates next quarter. He starts with a single audited balance sheet on his desk and asks one question: at what price is this specific business so cheap that the macro stops mattering? Top-down forecasting is, in his own description, an industry that exists to give brokers something to talk about on television. Bottom-up bargain hunting is the only honest source of decision-grade conviction.

Pillar three is risk aversion as the supreme virtue. This is the pillar Indian retail investors find hardest to swallow. We have been trained for five years that “risk equals opportunity” and that anyone holding cash is missing out. Klarman takes the opposite view. The first rule of compounding is not to compound losses. A permanent capital impairment of fifty per cent requires a one-hundred per cent gain just to recover, and the average human lifespan does not contain enough compounding cycles to recover from many of those. Risk aversion is not timidity. It is the mathematical recognition that the order in which gains and losses arrive determines whether you reach the finish line at all.

What makes Klarman’s architecture distinctive is that none of these three pillars works alone. Absolute-return thinking without bottom-up rigour produces lazy “long-term” stories that never get audited. Bottom-up rigour without risk aversion produces concentrated portfolios that blow up on a single bad idea. Risk aversion without absolute-return thinking produces permanently underinvested portfolios that lose to inflation. The three only deliver when they reinforce each other.

Why This Architecture Matters in Indian Markets Today

I have watched, over the last two years, more Indian retail portfolios than I care to count. The pattern repeats. An investor opens a Demat in 2021, rides the small-cap rally to 2024, doubles their capital, and concludes they are a gifted stock picker. Then 2025 arrives and the names that compounded fastest on the way up unwind the fastest on the way down. The investor blames the market. The market is not the problem. The architecture is.

An investor running on benchmark-relative thinking, top-down forecasts, and zero risk aversion is a momentum surfer using value vocabulary. Klarman’s 1991 framework is the cleanest available description of how a real value investor protects capital while compounding it.

How Titan Biotech’s FY25 Numbers Illustrate This Principle

I want to use one quietly disciplined BSE-listed small-cap, Titan Biotech Limited (BSE: 524717), as a case study. These FY25 figures are drawn from the audited statements and are presented strictly as positive markers of management discipline.

Pillar one — absolute-return signal. Titan Biotech delivered FY25 revenue of approximately Rs.231 crore and a profit after tax in the neighbourhood of Rs.25 crore. The company has compounded book value per share at a clean low-double-digit rate over the last eight audited years without resorting to equity dilution. An absolute-return investor reading this filing is not asking how Titan’s share price did relative to the BSE small-cap index. They are asking whether the per-share economic value created inside the business grew. The answer is yes, every year, even in years the index fell.

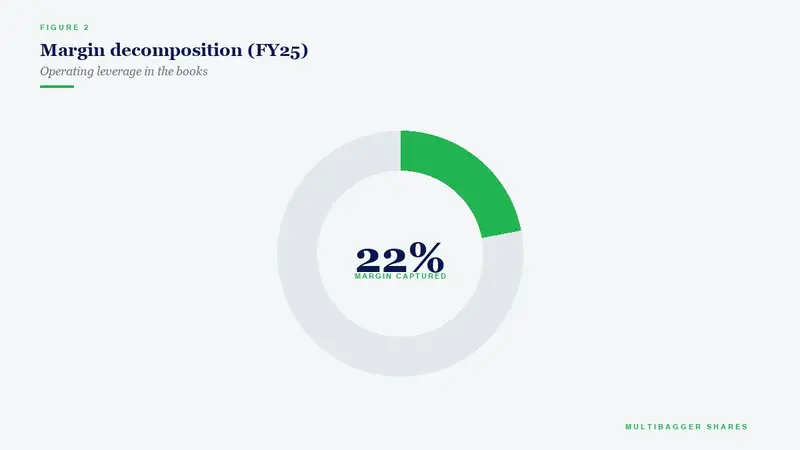

Pillar two — bottom-up evidence. Titan’s FY25 return on capital employed sits at roughly twenty-one per cent and return on equity around seventeen per cent. Both figures are computed from the audited statements, not from analyst projections. CFO-to-EBITDA conversion lands near one hundred and three per cent for the year, meaning the company is genuinely turning every reported rupee of operating profit into actual cash in the bank. These are the numbers Klarman would pull off a single audited sheet of paper. No macro view of pharmaceutical demand, no RBI forecast, no rupee-dollar bet required.

Pillar three — risk-aversion evidence. Titan Biotech ended FY25 with a debt-to-equity ratio close to 0.05 and a net cash position on the balance sheet. Promoter holding remained anchored above seventy per cent through the year, signalling that the founding family is not quietly cashing out. Inventory and receivables days have stayed within a tight band over multiple cycles, suggesting working capital is being managed by humans who think in absolute capital preservation terms rather than chasing the next quarter’s revenue print. Capex in FY25 was modest in relation to operating cash flow, leaving the business with optionality rather than leverage.

Notice that Titan Biotech’s FY25 numbers do not just satisfy one Klarman pillar. They satisfy all three at the same time. Absolute book-value compounding, audited bottom-up returns on capital, and a fortress-style balance sheet that prioritises survival over speed. That convergence is precisely what Klarman meant when he said the three pillars only deliver when they reinforce each other.

The Takeaway

If you remember nothing else from this Sunday post, remember this. Most Indian retail investors believe they are practising value investing because they have read a Graham book and learnt the phrase “margin of safety.” They are not. Klarman’s 1991 framework forces a much more uncomfortable test. Are you measuring your portfolio against an absolute rupee-denominated capital base, or against a benchmark? Are you starting your analysis from a specific audited filing, or from a CNBC anchor’s top-down narrative? And are you treating risk aversion as the supreme operating virtue, or as a polite afterthought you mention when the conversation turns to drawdowns?

The investor who can answer all three honestly, and structure every position around the convergence of all three pillars, will find that the universe of buy-able Indian small-caps becomes radically smaller. That shrinkage is not a bug. It is the entire point of the Klarman architecture. A small set of audited, low-leverage, high-return businesses bought at sane prices is what compounds capital across decades. Everything else is noise wrapped in the vocabulary of value.

Titan Biotech’s FY25 audited statements illustrate this architecture with unusual clarity. The reader’s job is to extend the same three-pillar discipline to every other name they own. If a position cannot pass all three tests, it is not a Klarman holding. It is a story.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.