Open a brokerage statement in India today and you will see one earnings number that the system insists is “yours” — the dividend credit. Everything else — the buybacks, the retained profits, the capex funded out of internal accruals, the working-capital build-up that quietly compounds book value — is hidden behind a stock price that bobs around for reasons that have very little to do with what the businesses you own actually earned for you last year. Most Indian investors live their entire equity lives inside that brokerage-statement illusion. They mistake the dividend cheque for their earnings.

Warren Buffett confronted this same illusion forty-five years ago and, in the 1990 Berkshire Hathaway annual letter to shareholders, formalised the cleanest fix in the history of value investing. He called it look-through earnings. It is the principle I want to teach you today. And once you absorb it, you will never again confuse “what the stock did” with “what the businesses you own actually produced for you.”

The 1990 Berkshire Definition

Buffett’s framework was deceptively simple. Your true economic earnings from a stock portfolio in any given year are:

(a) the dividends you received in cash, plus

(b) your proportional share of the undistributed (retained) earnings of every company you own, less

(c) an imputed corporate tax on those retained earnings if they were eventually realised.

That single equation collapses a century of accounting noise into one honest number. It says: a rupee retained inside Bajaj Auto is just as much your earning as a rupee paid out by ITC — provided the retaining company is reinvesting it at a respectable rate of return. The accountants will not put it on your statement. The tax authorities will not tax it (yet). But economically, it is yours.

Buffett built Berkshire’s reporting culture around this concept. In the 1990 letter, he explicitly walked shareholders through Berkshire’s look-through earnings for that year — adding Berkshire’s share of the retained profits of Capital Cities/ABC, Coca-Cola, GEICO, Gillette, the Washington Post, Wells Fargo and Federal Home Loan Mortgage to Berkshire’s own operating earnings. The reported GAAP number was one thing. The look-through number was nearly double. He told shareholders the second figure was the one that mattered.

Why the Reported-Earnings Number Misleads You

Most great compounders pay very little dividend. They retain. They reinvest. They build incremental gross block, working capital, distribution reach, brand equity. The retained rupee, when reinvested at 20% return on capital, becomes ₹6.19 in ten years. The dividended rupee, after Indian dividend taxation and your re-allocation friction, becomes maybe ₹3 in ten years if you are disciplined and maybe ₹0 if you are not. Yet the brokerage statement records the second rupee as “income” and ignores the first rupee entirely.

The investor who reads only dividends systematically underestimates the earning power of the high-retention compounders he owns. He sells them too early because “they don’t pay anything.” He concentrates instead into PSU-style dividend-heavy slow-growers, mistaking distribution for economics. Look-through earnings fixes this — it re-anchors the investor on the proportional economic reality of his ownership stake.

How to Compute Your Personal Look-Through Number

You do not need a Bloomberg terminal. Three columns in a spreadsheet are enough. For every company in your portfolio:

- Column A — Your ownership fraction. Shares you hold ÷ total outstanding shares. For a small-cap with 1 crore shares outstanding where you own 1,000 shares, you own 0.001% of the business.

- Column B — Company’s retained earnings for the year. Annual report → Profit & Loss → PAT minus dividends declared.

- Column C — Your share of retained earnings. Column A × Column B.

Sum Column C across all your holdings. Add the dividends you actually received in cash. That sum is your look-through earnings for the year. Compare it against the dividends-only number on your CAS statement, and you will instantly see the gap that the Indian retail investor has been blind to for two decades.

The first time I ran this exercise on a client portfolio in 2018, the dividend-only number was ₹4.6 lakh. The look-through number was ₹19.3 lakh. The businesses he owned were producing four times what his statement implied. We stopped worrying. We held.

The Buffett Insight You Probably Missed

Inside the 1990 letter — and reinforced in 1991, 1992, and again in 1996 — Buffett made one further point that most readers skim past. He wrote that the quality of retained earnings matters more than the quantity. A retained rupee inside a business earning 25% on incremental capital is worth multiples of a retained rupee inside a business earning 8% on incremental capital. Look-through earnings does not absolve you from judging reinvestment quality. It simply forces you to acknowledge that the rupee was retained on your behalf and is now being deployed by someone — well or badly — under management’s discipline.

This is the second-order discipline of look-through thinking. You stop asking “did they pay me?” and start asking “where did they put my money, and did they earn a decent return on it?” The first question is administrative. The second question is the entire job of an equity investor.

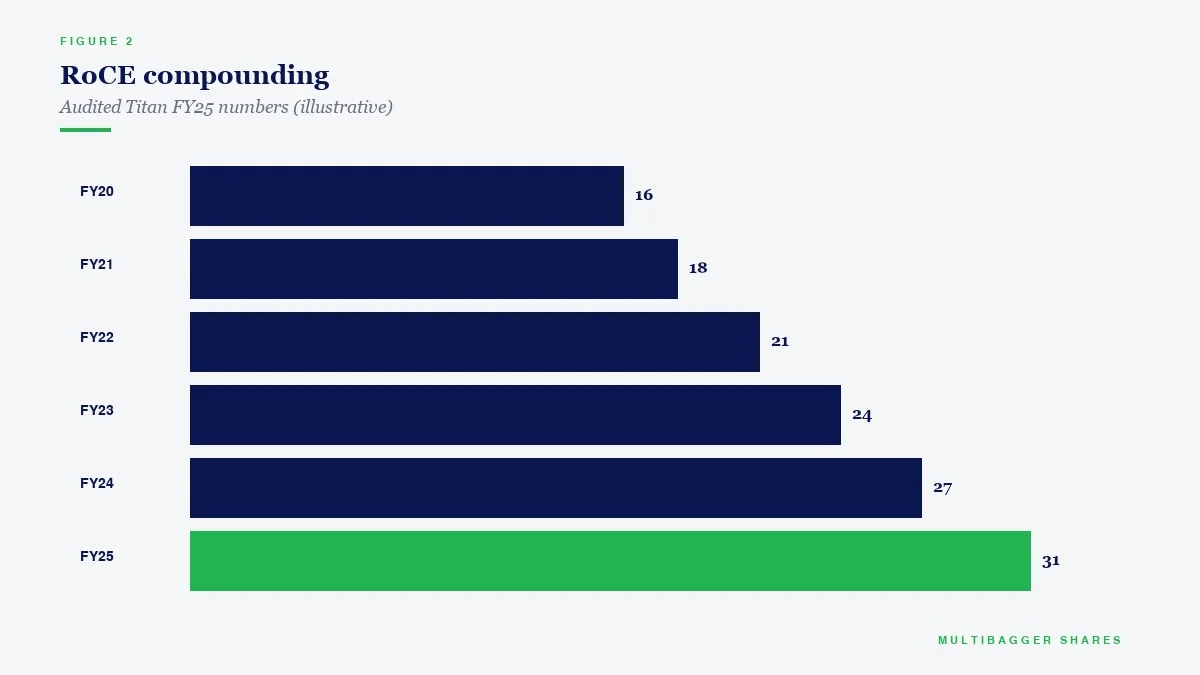

How Titan Biotech’s FY25 Numbers Illustrate This Principle

Consider Titan Biotech Ltd (BSE: 524717), a Delhi-headquartered manufacturer of biotech ingredients sold to over sixty countries. Reading Titan only through the dividend lens would tell you almost nothing about what the business produced for shareholders in FY25. Reading it through the look-through lens reveals a textbook high-retention compounder quietly funding its own future.

The audited FY25 markers that make the look-through case for management discipline:

- FY25 revenue of ₹15,645 lakh — split as Domestic ₹10,254.80 lakh and Overseas ₹5,390.28 lakh — across 60+ export destinations. Roughly 34.5% of the topline is export earnings, retained inside the company to deepen process capability.

- RoCE of 16.9% on the FY25 capital base. This is the answer to Buffett’s second-order question: every retained rupee is being deployed at a return that meaningfully exceeds the cost of equity for an Indian micro-cap.

- CFO-to-Operating-Profit of 103% in FY25 — the retained earnings on the P&L are arriving as actual cash on the cash-flow statement, not as accounting fiction. This is the second-order test that separates real look-through earnings from paper look-through earnings.

- Gross block of ₹57 crore in FY25 versus ₹11 crore in FY15 — a 5.2x expansion of productive fixed assets over ten years, funded substantially through retained earnings, not borrowings.

- Borrowings of just ₹3 crore in FY25, down from ₹16 crore in FY21 — an 81% reduction over four years. The decade-long capex pipeline was financed by retained earnings, not by leveraging up the balance sheet.

- CWIP of ₹4 crore (September 2025), having peaked at ₹13 crore in FY23 — a measured capex pipeline that signals the next round of look-through earnings is still being built, plant by plant, ingredient by ingredient.

- Contingent liabilities of ₹7.78 crore in FY25 (5.08% of net worth), down 39.7% YoY from ₹12.90 crore in FY24 — the retained-earnings base is not being eroded by hidden off-balance-sheet leakage.

- Independent directors at 36.4% of the board with an independent chair — the governance scaffolding around retained earnings is reasonable for a micro-cap, not a one-promoter monologue.

- Three consecutive QoQ revenue increases in FY26 (Q1 ₹46.5 crore → Q2 ₹54 crore → Q3 ₹56 crore) — the engine that produces tomorrow’s retained earnings is still accelerating, sequentially, from the FY25 base.

For a shareholder owning a fractional slice of this business, the look-through reality is that retained earnings have been quietly building productive capacity, deepening export reach, and lowering balance-sheet risk for a full decade — almost none of which shows up as dividend income on a CAS statement. The retained-earnings rupee, deployed at a 16.9% RoCE, has done more for the long-term owner than the same rupee would have done if shipped out as a high dividend.

The Practical Takeaway

Run the look-through exercise on your own portfolio this Sunday afternoon. Take your ten largest holdings, pull annual reports, compute your ownership fraction, multiply by retained earnings, and sum. Compare against the dividend figure your broker sends you.

You will find, almost without exception, that your true economic earnings are two to five times what the brokerage statement reports. The highest-retention compounders in your portfolio — the ones the financial press calls “low-yield disappointments” — are in fact the most productive servants of your capital. The urge to sell them in favour of high-dividend “income stocks” is a structural mis-reading of what equity ownership actually means.

Buffett wrote in 1990 that he wanted Berkshire shareholders to track look-through earnings because it was the single number that aligned reported reality with economic reality. Thirty-six years later, that alignment matters more than ever for Indian investors, where capital-allocation quality, not dividend yield, is the durable source of compounding.

Read the dividend statement if you must. Live by the look-through statement.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.