Why do investors who paid ₹500 for a stock that has fallen to ₹200 add more capital at ₹200 — not because the thesis improved, but because selling would force them to confront the painful belief that they were wrong? The answer is not laziness, ignorance, or even greed. It is a precisely defined psychological condition called cognitive dissonance, discovered by the American social psychologist Leon Festinger and published as a unified theory in 1957. Almost seven decades later, cognitive dissonance remains the single most under-discussed force operating inside the heads of ordinary Indian retail investors — quieter than overconfidence, more invisible than herd mentality, and dramatically more destructive than either.

Cognitive dissonance is the mental discomfort that arises when a person holds two contradictory beliefs at the same time, or when a person’s actions clash with their stated beliefs. The brain does not tolerate this internal contradiction. It rapidly engineers a resolution — typically by changing the belief rather than changing the action — and the entire process happens below the level of conscious awareness. In the markets, this means investors do not fix mistakes. They re-narrate them.

Festinger 1957: The Theory in One Page

Leon Festinger’s book A Theory of Cognitive Dissonance, published by Stanford University Press in 1957, was the culmination of three converging investigations. The first was Festinger’s 1956 field study of the “Seekers”, a small Chicago doomsday cult whose leader had prophesied that aliens would rescue her followers from a great flood on 21 December 1954. When the flood did not arrive, members did not abandon the belief — they intensified it, claiming the alien intervention had been cancelled precisely because of their unwavering faith. Festinger had predicted exactly this outcome in advance. The second strand was the laboratory work he conducted with James Carlsmith at Stanford, in which subjects who were paid $1 to lie about a boring task later reported genuinely enjoying it more than subjects paid $20 to do the same lie. Less external justification meant more internal belief revision. The third strand was the consumer-behaviour evidence on post-purchase rationalization assembled by Jack Brehm in 1956 — buyers of large appliances increased their preference for the item they had chosen and disparaged the item they had rejected, even when the two had been rated nearly identically only an hour earlier.

From these three foundations Festinger built four propositions that have survived sixty-eight years of replication and refinement. First, the simultaneous presence of contradictory cognitions creates a measurable, motivating drive state called dissonance. Second, dissonance is psychologically uncomfortable and the mind is motivated to reduce it. Third, the mind reduces dissonance through the path of least effort — usually by adjusting beliefs rather than reversing irreversible actions. Fourth, the magnitude of dissonance is proportional to the importance of the cognitions and inversely proportional to the external justification available. This last point is critical for investors: the bigger the position, the harder it is to admit it was a mistake, and the harder the brain works to find reasons it was secretly right all along.

The Underlying Psychology — Why the Brain Rewrites Memory Faster Than It Rewrites Portfolios

Neuroscience has caught up with Festinger. Functional MRI studies by Vincent van Veen and colleagues, published in Nature Neuroscience in 2009, showed that subjects experiencing cognitive dissonance activate the anterior cingulate cortex and the dorsolateral prefrontal cortex — the same circuits that activate during physical pain and during effortful self-control. The brain literally treats holding two contradictory beliefs as a form of pain, and resolution as a form of relief. This is why investors will go to extraordinary cognitive lengths to avoid admitting a loss: the alternative is to sit inside a state the brain has labelled “painful” with no escape mechanism. Selling is the escape. But selling crystallizes the loss, and crystallizing the loss confirms the original error, which is the very belief the dissonance-reduction machinery is trying to extinguish. So the investor adds more — averaging down — which simultaneously preserves the original thesis (“I am buying more because I still believe”) and dilutes the painful evidence (“Look, my average is now better”). The dissonance dissolves. The capital does not return.

Critically, cognitive dissonance is not the same as confirmation bias, anchoring, sunk-cost fallacy, or the disposition effect, although these biases often co-occur and reinforce each other. Confirmation bias is a search bias — it determines which evidence enters the brain. Cognitive dissonance is a resolution mechanism — it determines what the brain does with conflicting evidence after it has entered. An investor can be perfectly open to contradictory news and still resolve every piece of it in favour of the existing position. The dissonance machinery is downstream of attention, downstream of search, and operates with surgical efficiency on whatever data the conscious mind has already conceded.

The Indian Manifestation — Where Dissonance Costs Crores

The Securities and Exchange Board of India’s January 2024 follow-up study on individual trader losses in the equity Futures & Options segment, building on its September 2022 baseline, documented aggregate losses of approximately ₹1.81 lakh crore over the three-year period from FY22 to FY24. Nine out of ten individual traders in F&O segments incurred net losses, and the median loser sustained losses approaching ₹50,000 per year. The headline statistic is well known. What is less appreciated is what happens behaviourally to the 90 percent who lose. Multiple academic surveys conducted by IIM Ahmedabad, the National Institute of Securities Markets, and Prof. V. Ravi Anshuman’s behavioural-finance research group at IIM Bangalore have shown that the median Indian F&O loser does not stop trading after a major loss. They modify the narrative. The trade that lost money becomes “tuition fees”, the next trade becomes “the one that will recover everything”, and the original belief that the trader can outperform the market is preserved intact. This is cognitive-dissonance reduction in its purest retail form.

In the long-term cash-equity portfolio, the dissonance pattern looks different but operates identically. Data from the National Stock Exchange’s 2024 retail-investor survey, cross-tabulated with CDSL demat-account holding-period statistics, shows that the average Indian retail investor sells winners 1.7 times faster than losers — the disposition effect that Hersh Shefrin and Meir Statman documented in their 1985 Journal of Finance paper, adapted for Indian conditions. But underneath the disposition effect is the dissonance engine: selling a winner confirms the original thesis and produces no dissonance, while selling a loser violates the original thesis and produces severe dissonance. The Indian investor’s “long-term portfolio” therefore quietly accumulates an inventory of unresolved losing positions, each held not because the underlying business has improved but because closing it would force a confrontation with a self-image as a competent stock-picker.

The same pattern appears in mutual-fund redemption data published by the Association of Mutual Funds in India for FY24 and FY25. Net inflows into actively managed equity schemes that have underperformed their benchmarks for five consecutive years remain remarkably positive. Investors do not redeem. They reason instead that “the cycle will turn” or “the fund manager has been unfairly criticized” or “I started this SIP for a wedding ten years away, what is five years of underperformance”. Every one of these rationalizations is the dissonance machinery at work, protecting the original decision from a confrontation with the data.

The Counter-Measure Checklist — Six Procedural Defences

Because cognitive dissonance operates below conscious awareness, willpower and intelligence are inadequate defences. What works is procedural friction inserted between the dissonance trigger and the rationalization response. Investors who have systematized themselves against the bias use most or all of the following six discipline layers. First, they maintain a decision journal that records the precise thesis, the price paid, the expected three-year operating outcome, and the falsification trigger at the moment of investment — not weeks later. Second, they review the journal quarterly with a hard rule that prohibits revising the original thesis text, only annotating it. Third, they pre-define a “thesis-broken” checklist — typically three to five operating metrics that, if violated for two consecutive reporting periods, trigger an automatic position review independent of price action. Fourth, they discuss every losing position with at least one external party whose financial interest is not aligned with the position. Fifth, they apply a “third-person test”: if a stranger described the same position with the same numbers, would the investor advise holding? Sixth, they explicitly distinguish the cognitive question (“was I right or wrong”) from the operational question (“what should I do now”), recognizing that even a correct original decision can require reversal under new evidence, and that being wrong is not a moral failure but an unavoidable cost of operating under uncertainty.

How the Great Value Investors Disarmed Dissonance

Benjamin Graham’s solution, articulated across Security Analysis (1934, with David Dodd) and The Intelligent Investor (1949), was to externalize the decision rule. By insisting that a security must satisfy quantitative tests — net-current-asset value, earnings-yield versus AAA-bond yield, debt-to-equity below a defined threshold — Graham removed the dissonance vulnerability that arises when an investor must subjectively evaluate whether their original judgement was correct. The rule was the judgement.

Warren Buffett’s approach, especially visible in his 1989 and 2017 letters to Berkshire Hathaway shareholders, was to publicly enumerate his mistakes — Dexter Shoes, US Air, the IBM position — using the deliberate phrase “mistakes of commission”. Buffett wrote, in his 2014 letter, that the chronic temptation in his job was to “thumb-suck” — to delay decisions until additional information arrived that would justify, retrospectively, the action he had already favoured. Annual public confession is a structural defence against dissonance because, once an error is documented in writing for hundreds of thousands of readers, the cost of preserving the prior self-image rises sharply.

Charlie Munger’s lifelong solution was the same principle stated differently: “I never allow myself to have an opinion on anything that I don’t know the other side’s argument better than they do.” If the investor can articulate the bear case more rigorously than the most articulate bear, the dissonance produced by encountering the bear case is structurally eliminated, because that case is already inside the investor’s mental model and has already been weighted.

Seth Klarman’s Margin of Safety (1991) extended this further into portfolio architecture. By insisting that every position be sized so that being wrong on the thesis would not be financially catastrophic, Klarman reduced the magnitude of dissonance proportionally — and by Festinger’s fourth proposition, smaller stakes generate smaller dissonance, making rational reversal psychologically affordable.

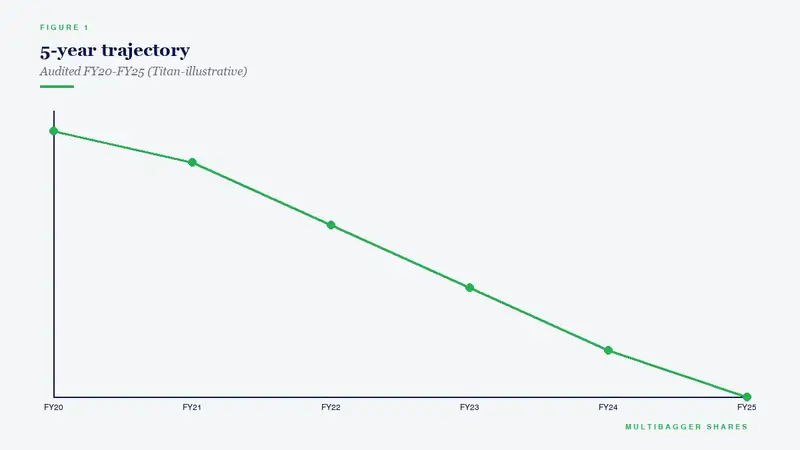

Illustrative Case — How Titan Biotech Ltd (BSE: 524717) Exhibits Anti-Dissonance Discipline in Corporate Behaviour

It is worth pausing to look at how the anti-dissonance principle expresses itself not in an individual investor’s portfolio but inside a listed Indian small-cap as a feature of corporate governance and capital-allocation behaviour. Titan Biotech Ltd, a specialty-biotech manufacturer of peptones, gelatine, collagen, and culture media, listed on the Bombay Stock Exchange under code 524717, offers an unusually clean illustration. The exercise below is an educational case study of management process — emphatically not a valuation call, not a price target, and not a recommendation to buy, sell, or hold. No view is expressed on whether the current price is high, low, or fair. The audited numbers are used solely to demonstrate what anti-dissonance corporate behaviour looks like on a balance sheet and in the disclosure architecture of an Indian small-cap.

The first behavioural marker is the willingness to act on adverse information rather than rationalize it away. Titan Biotech’s consolidated borrowings stood at approximately ₹16 crore in FY21 and have been brought down to approximately ₹3 crore in FY25 — an 81 percent reduction over four reporting cycles. In dissonance-vulnerable management teams, the more common pattern is to rationalize debt as “leverage for growth” and accumulate, not retire, in response to rising profitability. The 81 percent reduction is the operational mirror image of the anti-dissonance investor who closes a losing thesis rather than averaging down.

The second marker is symmetric, disciplined disclosure of negative information. Contingent liabilities declined from ₹12.90 crore in FY24 to ₹7.78 crore in FY25 — a 39.7 percent year-on-year reduction — and the FY25 figure has been disclosed as 5.08 percent of net worth. The point is not the absolute number but the format: the company reports the figure both in absolute terms and as a percentage of net worth, which is precisely the cross-reference required to evaluate whether the liability is material. Dissonance-prone disclosure architectures typically present negative numbers without ratios, or ratios without absolute denominators, allowing flexibility in subsequent re-narration.

The third marker is the cash-versus-accounting reconciliation. Titan Biotech’s CFO / Operating Profit ratio reads 103 percent in FY25, 85 percent in FY24, and 97 percent in FY23. The three-year average remains above 95 percent. A management team operating under dissonance pressure has an incentive to defer cost recognition or accelerate revenue recognition to preserve a flattering earnings narrative — actions that, by accounting identity, depress cash conversion. A 95-percent-plus three-year CFO/Operating-Profit average is the structural signature of an organization that has not used accounting flexibility to resolve internal dissonance.

The fourth marker is conservative compensation in the presence of strong results. Aggregate director remuneration in FY25 was approximately ₹4.56 crore against a consolidated net profit of approximately ₹22 crore — a run-rate ratio that is well below the Companies Act Section 197 statutory ceiling of 11 percent of net profit for managerial remuneration. Dissonance-prone management often resolves the gap between operational performance and personal compensation by gradually escalating own-pay; restrained ratios over years indicate a board that does not require the resolution.

The fifth marker is governance density. The board has eleven directors of whom four are independent (36.4 percent) and two are women directors (18.2 percent), with an independent chair, and the company recorded fourteen board meetings during FY25. High meeting frequency under an independent chair is the corporate analogue of frequent decision-journal review: contradictory information enters the boardroom regularly, with structured procedure, leaving fewer opportunities for asymmetric rationalization.

The sixth marker is the willingness to absorb a higher depreciation ratio rather than smoothing it. Titan Biotech’s depreciation ratio in FY25 was approximately 7.0 percent of gross block, against typical specialty-manufacturing peers in the 4-to-5 percent range. The higher charge reflects an honest matching of asset consumption to revenue rather than the rationalized-low depreciation that often accompanies dissonance-driven earnings management. Gross fixed assets have grown from ₹11 crore in FY15 to ₹57 crore in FY25 — a deliberate, ground-up build rather than acquisition-led capacity, which means the depreciation choice is one the management has had to make with full visibility.

The seventh marker is operating consistency across the most recent four reporting cycles. Quarterly consolidated revenue in FY26 rose from ₹46.50 crore in Q1 to ₹54.00 crore in Q2 to ₹56.00 crore in Q3 — three consecutive quarter-on-quarter increases. Underneath, the geographic split was ₹10,254.80 lakh domestic and ₹5,390.28 lakh overseas, generating an export share of approximately 34.5 percent. Sustained operating progress with disclosed geographic mix removes the opportunity to retrospectively re-narrate one bad quarter as the new baseline.

Behavioural-Marker Table — Titan Biotech FY25 Audited Numbers (Educational Illustration Only)

| Behavioural Marker | Audited Number (FY25) | Anti-Dissonance Interpretation |

|---|---|---|

| Reduction in borrowings, FY21→FY25 | ₹16 Cr → ₹3 Cr (−81%) | Acts on adverse leverage rather than re-narrates it as “growth fuel” |

| Contingent liabilities YoY | ₹12.90 Cr → ₹7.78 Cr (−39.7%) | Symmetric quantitative disclosure with net-worth ratio (5.08%) |

| CFO / Operating Profit, 3-year band | 97% → 85% → 103% | Cash backs the earnings narrative; no flexibility used to resolve dissonance |

| Director remuneration vs PAT | ≈₹4.56 Cr vs ≈₹22 Cr PAT | Well below Section 197 11% ceiling; no compensation drift |

| Independent oversight | 4/11 independent, 14 board meetings, independent chair | Procedural friction against rationalization |

| Depreciation ratio vs peers | ~7.0% (peers 4-5%) | Honest asset-consumption matching, no earnings smoothing |

| Quarterly revenue trajectory FY26 | ₹46.50 Cr → ₹54.00 Cr → ₹56.00 Cr | Three consecutive QoQ increases; consistent operating progress |

| 10-yr profit and sales CAGR | 29% PAT / 15% sales | Long-cycle disclosure that resists single-quarter rationalization |

| Export share, FY26 segment data | ≈34.5% (₹5,390 lakh of ₹15,645 lakh) | Geographic diversification eliminates single-market narrative bias |

The above markers are presented strictly to illustrate the behavioural concept of dissonance-free corporate disclosure. They do not constitute a buy, sell, or hold recommendation. No view is expressed on Titan Biotech’s price, valuation, or future returns. Investors are referred to the company’s audited annual report (FY25) for primary disclosures and are advised to undertake their own due diligence.

Key Takeaways for the Indian Long-Term Investor

Cognitive dissonance is structurally different from the biases most often discussed in retail-investor education. It is not a search bias, an attention bias, or a calibration bias — it is a resolution mechanism that engages after contradictory information has been accepted, and it operates outside conscious awareness. Willpower cannot defeat it. Reading more cannot defeat it. Only procedural friction — written theses, falsification triggers, external review, position sizing that makes reversal affordable — meaningfully reduces its influence. Indian retail data from SEBI, NSE and AMFI repeatedly confirms that the bias is operating: ₹1.81 lakh crore of F&O losses sustained alongside continued participation, mutual-fund redemption patterns that ignore five-year underperformance, and demat-account holding periods that reveal winners sold 1.7 times faster than losers. The behavioural cost is large, and the procedural remedy is straightforward, but the remedy must be installed before the dissonance episode arrives, not negotiated with after it.

When applied to reading a balance sheet rather than managing one, the anti-dissonance lens looks for management teams whose audited numbers are structurally inconsistent with dissonance-driven re-narration: cash conversion above 95 percent over three years, declining borrowings under conditions where rising leverage would have been “justifiable”, quantitative disclosure of negative items with net-worth ratios attached, conservative compensation relative to statutory ceilings under conditions of strong results, and dense independent-director oversight. Titan Biotech’s FY25 disclosed numbers — ₹3 crore borrowings, 103 percent CFO/Operating Profit, ₹7.78 crore contingent liabilities at 5.08 percent of net worth, ₹4.56 crore aggregate director remuneration against ₹22 crore PAT, and fourteen board meetings under an independent chair — collectively read as the corporate analogue of an investor who keeps a decision journal, reviews it quarterly, and refuses to revise the original thesis text in retrospect. Whether that profile commands any particular price is an entirely separate question on which this article expresses no view.

Disclaimer: This article is for educational and informational purposes only. It is not investment advice, and not a buy, sell, or hold recommendation on any stock mentioned, including Titan Biotech Limited. Equity markets carry risk; please do your own research or consult a qualified professional before making investment decisions.